- Colombia: April manufacturing and retail indicators suppressed by COVID-19 lockdowns, but suspension of protests bodes well for the future

- Mexico: S&P affirms the country’s long-term sovereign rating, but maintains negative outlook

COLOMBIA: APRIL MANUFACTURING AND RETAIL INDICATORS SUPPRESSED BY COVID-19 LOCKDOWNS, BUT SUSPENSION OF PROTESTS BODES WELL FOR THE FUTURE

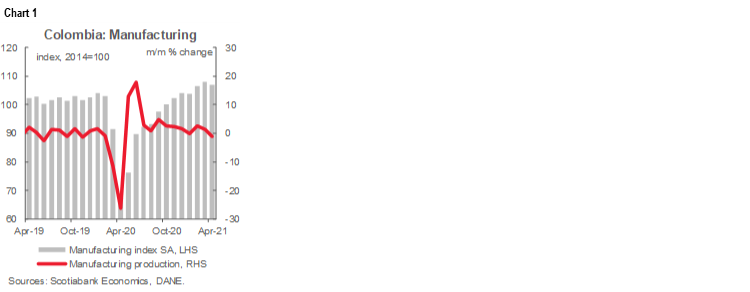

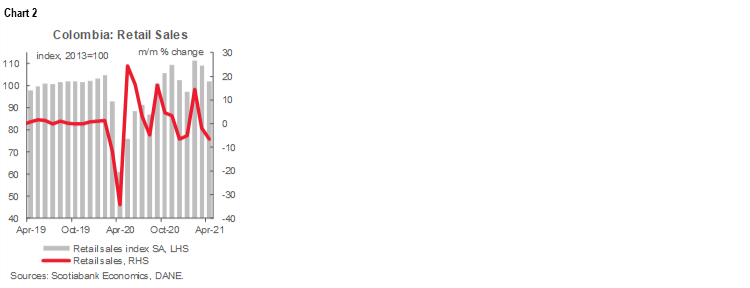

Manufacturing production and retail sales data for April published by the Colombian National Statistical Department, DANE, June 15 were suppressed by lockdowns in major cities but showed substantial y/y gains compared to April 2020, when lockdowns were more stringent.

Manufacturing production fell -1.0% m/m sa in April (chart 1) as lockdowns to slow the third wave of COVID-19 were implemented in Bogota, Antioquia, the north coast, and other regions. Fuel oil, steel and iron, and coffee production were hardest hit.

On a year-over-year basis, April manufacturing data showed an expansion of 63.7% y/y, above the Bloomberg market consensus of 61.5% y/y and Scotiabank’s 59.4% y/y estimate. Base effects account for this rise, as the economy was under a more severe lockdown in April 2020. In contrast, manufacturing expanded by only 5.2% compared with the pre-pandemic (April 2019) level.

Base effects account for the fact that output in all sectors expanded in April on a year-over-year basis, with construction-related mining products (808%), clothing (745%), beverages (170%); and oil refining (68%) posting the highest increases. Together these four sectors jointly accounted for about half of the overall yearly gain.

Antioquia, Cundinamarca, and Bogota led these gains and contributed 90% of Colombia’s year-on-year growth in manufacturing. However, Bogota contracted (-4.1%) compared to April 2019.

Total retail sales, ex-vehicles, fell by -6.5% m/m sa in April (chart 2), owing to lockdowns implemented in some of Colombia’s major cities, as all retail sales groups fell. In fact, it was the worst monthly contraction since the pandemic began.

On a year-over-year basis, retail activity increased by 75% y/y in April, posting a mild negative surprise as compared to the Bloomberg survey consensus (77.5% y/y), and below our expected 77% y/y. Base effects also affected this figure, as retail sales were flat (-0.1%) compared with pre-pandemic levels (April 2019).

Large increases were registered vehicles for household use (2,012% y/y), spare parts for cars (575% y/y) and fuel sales (105% y/y). Compared to April 2019, the best performing lines were vehicles (10.5%), computers for domestic use (33%), and cleaning products (34%). On the negative side, the most significant declines relative to pre-pandemic (April 2019) levels were concentrated in clothing (-3% y/y) and vehicles (-4.3% y/y), reflecting the lasting effects of the pandemic.

By region, Bogota led the gains with a 78% y/y increase in retail activity, but also registered the largest contraction compared to pre-pandemic 2019 levels (-6.1%).

Looking ahead, May data for manufacturing activity could be significantly weaker as some industries have experienced disruptions to their operations resulting from social unrest. According to DANE estimates from its electricity demand indicator, manufacturing activity in May could fall by almost 23% from pre-COVID-19 levels. May retail sales could also contract as the nationwide strike disrupts supply chains, increasing the inflation in some key items.

Activity should pick up in June, however, as protests dissipate and production is restored. In this respect, on June 15 protest leaders announced they will suspend demonstrations, providing an impulse to economic activity. While the labour market remains a concern, since employment remains around 4% below pre-pandemic levels in manufacturing and 3.5% below in retail sales, employment should rise as economic reopening consolidates. Therefore, although economic activity in Q2-2021 will be weaker because of social unrest, we continue to expect 6% y/y GDP growth in 2021.

On this basis, we reaffirm our view that the central bank (BanRep) will begin moving toward hikes in September or October.

—Sergio Olarte & Jackeline Piraján

MEXICO: S&P AFFIRMS THE COUNTRY’S LONG-TERM SOVEREIGN RATING, BUT MAINTAINS NEGATIVE OUTLOOK

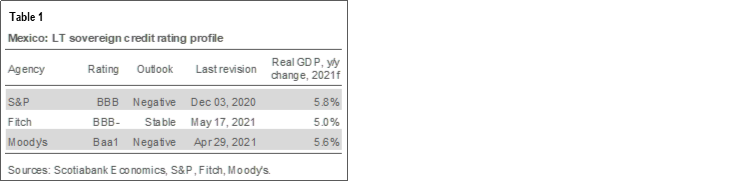

On Tuesday, June 15, S&P affirmed Mexico’s long-term sovereign rating in foreign currency at BBB, one notch above non-investment grade (table 1), but maintained its’ negative outlook.

S&P cited a strong external profile, including a flexible exchange rate and inflation targeting regime that supports the credibility and flexibility of its sound monetary policy. Net government debt is expected to remain stable at around 48% of GDP over the next two years, consistent with the BBB group.

S&P expects that the conservative fiscal stance that has characterized the current administration will continue in the second part of its term, supporting macroeconomic and financial stability. Economic growth is expected to rebound to 5.8% y/y in 2021 (which is a little more optimistic than our 5.3% y/y expectation) driven by robust US demand, record remittances from workers abroad, which support consumption in the lower income segment, and a broad recovery in tourism, as vaccines become more widely available. S&P anticipates growth to slow over 2022–2024 to below 3.0% y/y owing to low public and private sector investment, the relatively low quality of education, and high levels of crime and judicial uncertainty. S&P’s announcement also highlighted the recent mid-term elections, noting that with greater counterweights in the Chamber of Deputies the results are unlikely to lead to a material shift in macroeconomic policies.

Our take is that rating agencies will maintain Mexico’s current ratings until the broad outlines of fiscal reforms scheduled for the second half of this year are clear. In our view, the need for fiscal reform is becoming increasingly urgent as a result of the rise in the public debt-to-GDP ratio caused by the economic crisis of 2020. Our estimates and projections suggest that, to anchor the trajectory of public debt, a fiscal adjustment equivalent to around three percentage points of GDP would be needed, of which one point would be necessary to capitalize Pemex. This adjustment could be achieved through cuts to spending that expand the primary surplus, and through an increase in public revenue from greater collection efficiency, a broadening of the tax base, the introduction of new taxes, or hikes in some existing taxes.

—Paulina Villanueva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.