- Peru: Election update and recent political events

- Chile: If not for the increase in gasoline prices, inflation would have been 0% m/m in June

- Mexico: Auto industry recovering in June, still below pre-pandemic levels

PERU: ELECTION UPDATE AND RECENT POLITICAL EVENTS

Peru’s electoral authorities have continued their review of contested ballots of the presidential election that took place on June 6. We might see movement soon, as July 8 (today) has been deemed by authorities as the tentative date to conclude said review, paving the way to officially pronounce a winner by July 15.

The contested election result will take place amidst a very volatile political environment, which includes a recently launched corruption investigation against Pedro Castillo’s (the leading presidential candidate) political party, and new tensions between the current (outgoing) congress and the judiciary.

Perú Libre leadership under investigation

Perú Libre (PL), the party of leading presidential candidate, Pedro Castillo, is under investigation amidst claims of wrongdoing involving campaign funds. The scandal involves the party leader, Vladimir Cerrón, and other prominent party leaders.

Pedro Castillo has not been named in the accusations; therefore, he is likely to distance himself from the controversy and those involved. If deemed the presidential winner, however, Mr. Castillo would need to navigate the politics carefully to avoid alienating the party base. The PL will, after all, hold the largest share of congressional seats (37/130) in the new legislature that is due to be sworn in at the end of this month (no later than July 27). In a way, Cerron losing influence could allow Mr. Castillo greater maneuvering room, particularly on key appointments.

Tensions between congress and the Constitutional Tribunal

In a surprising development, on July 6 the Superior Court of Lima ordered Congress to halt procedures for the election of six members of the Constitutional Court (Tribunal Constitucional, TC), arguing that procedures lacked transparency.

Members of Congress defied the order, proceeding with the vote and alleging interference. The vote was nonetheless unsuccessful as neither of the two proposed candidates obtained the 87 required votes.

This is yet one more development in a long string of quarrels between congress and the other branches of government. The majority of members of the Constitutional Court (6/7) have been eligible for replacement for some time, but at this stage it appears unlikely that the current congress will succeed in making new appointments, given the limited time left before the new legislature is sworn in.

—Guillermo Arbe

CHILE: JUNE CPI INCREASED 0.1% M/M (3.8% Y/Y), CALMING INFLATIONARY ANXIETIES

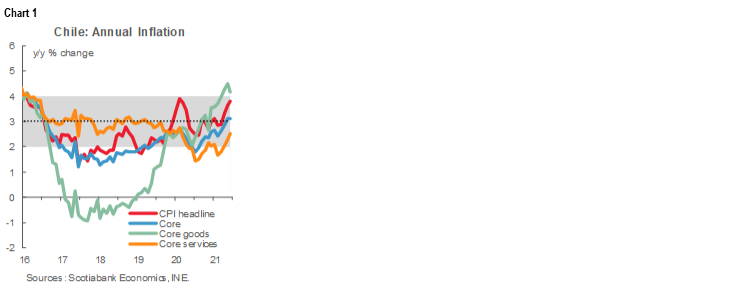

I. If not for the increase in gasoline prices, inflation would have been 0% m/m in June

Data released July 8th showing June inflation of 0.1% m/m (3.8% y/y) is in line with our forecast but came in well below the consensus (0.34%) (chart 1). The outcome surprised those who projected that the recent rise in inflation would continue. We did not share that view given the persistent weakness of the labor market, the transitory nature of recent inflationary shocks and disruptions to distribution channels, and demand fundamentals that remain very weak.

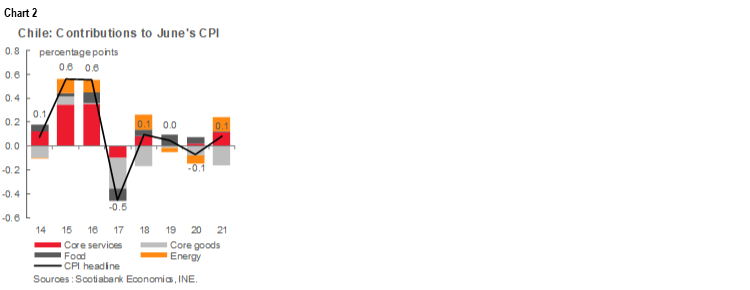

June inflation is explained by the increases in fuel prices (gasoline and diesel), without which inflation for the month would have been 0% m/m (chart 2). Inflation ex- food and energy items was -0.1% m/m (3.1% y/y).

For July, we project inflation between 0.2% and 0.3% m/m (4% y/y). Key drivers are likely to be transportation costs, highlighting the increase in fuel prices, as well as seasonal increases in inter-city transportation fares, which could be reinforced by the relaxation of mobility restrictions announced this month. Likewise, we expect limited increases in prices of the food and non-alcoholic beverages, and modest increases in the prices of fruits, vegetables and meats.

Disinflationary risks from the political arena remain. Legislation that would temporarily reduce the specific tax on gasoline and diesel by 50% (with a potential direct negative impact of -0.5 percentage points m/m) continues to move forward in the Congress. There are at least two other initiatives that also seek to reduce the specific tax. Likewise, a draft bill to reduce VAT for certain essential products remains under review. All in all, we maintain our projection of year-end 2021 annual inflation at 3.5%.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

MEXICO: AUTO INDUSTRY RECOVERING IN JUNE, STILL BELOW PRE-PANDEMIC LEVELS

According to the INEGI release of auto industry data for June, the sector continues to recover at a moderate pace. Microprocessor supply chain disruptions continue to keep the sector’s production below capacity, with some estimates suggesting microchip shortages could continue beyond year-end. Auto production and sales advanced 9.3% m/m and 1.7% m/m, at 264.0 thousand and 87.1 thousand units, respectively, while exports fell 3.2% m/m to 234.4 thousand units (chart 3). On a year-over-basis, the auto industry reported significant upsurges owing to base effects. Production advanced 5.5% y/y, exports rose 18.3% y/y, and domestic sales grew 38.5% y/y. Cumulative data from January to June show auto production increased 31.8% YTD, exports grew 33.5% YTD and domestic sales advanced 18.1% YTD. However, production, exports and domestic sales remain -20.5%, -19.5%, and -20.5% below January–June 2019 levels, respectively. Cumulative data thus suggest a slow, yet firm recovery, although the industry has still not recovered pre-pandemic levels.

Despite upward revisions in the last months in GDP forecasts for Mexico and US, semiconductor shortage that result in supply bottlenecks and shortages of critical components could still hamper the industry, generating uncertainty with respect to the outlook for the industry.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.