- Chile: GDP "again" recovers pre-Covid levels; Labour market loses strength in May

- Colombia: Employment edges up despite nationwide strike; Banrep minutes reveal the board remains vigilant on inflation, fiscal and international financial conditions; Fitch cuts Colombia's sovereign rating to BB+ as prospects for debt reduction in the medium term are judged low

- Peru: inflation rose in June, exceeds upper limit target range

CHILE: GDP "AGAIN" RECOVERS PRE-COVID LEVELS; LABOUR MARKET LOSES STRENGTH IN MAY

I. Economic activity up 18.1% y/y in May (2.6% m/m), with all non-mining sectors expanding on seasonally adjusted basis and fiscal support fueling growth

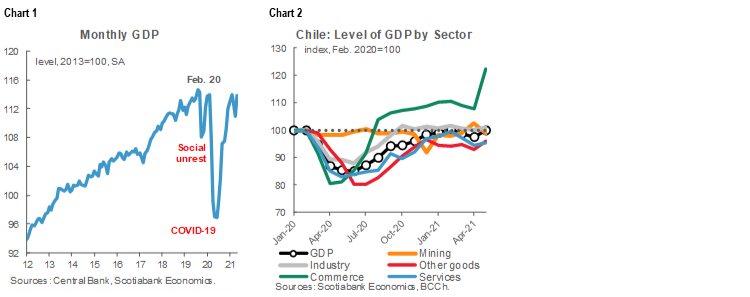

IMACE economic activity indicators for May showing an increase of 18.1 % y/y (2.6% m/m) suggest the economy has adjusted to mobility restrictions. This accommodation effect supports our early view of GDP expansion of not less than 7.5% in 2021 (chart 1). We maintain our forecast of a GDP growth range between 7.5% and 8.5%. However, the loss of salaried employment raises concerns regarding the resiliency of the labor market in the medium term, and complicates political narratives in which the recovery of GDP to pre-Covid levels (chart 2) is tempered by a significant employment gap (1 million jobs to recover).

IMACEC showed an economic activity expansion of 18.1%, in line with consensus (Bloomberg: 17.5%) and somewhat above from our projection (16.5%). Non-mining GDP expanded 3.5% m/m, slightly above what we anticipated (2.8%), but in the context of greater labour market mobility compared with previous month. All non-mining sectors recorded significant m/m growth, highlighting the effects of an additional business day in May and liquidity injections of households from pension fund withdrawals (chart 2).

Public Spending grew by an 59.1% y/y in real terms in May, with "Subsidies and Donations" expanding by an incredible 125% y/y. This has been the trend of fiscal spending thus far in 2021, which is strongly supporting economic growth and accounts for a real increase of 24.8% y/y as of May, with strong growth in capital spending (8.3% y/y). In the first months of the year, budgetary execution of public spending continues to advance faster than in previous years, with an execution rate of 48.7% as of May, which compares very favorably with the 38.4% rate as of May 2020.

For June, we forecast a monthly GDP expansion of between 17–18% y/y, which still reflects the base effect of low level in 2020, with a monthly recovery of no more than 1% m/m. Mobility restrictions were again tightened in June, imparting some uncertainty with respect to the outlook.

II. Labour market loses strength in May

WIDESPREAD JOB DESTRUCTION ACROSS ECONOMIC SECTORS

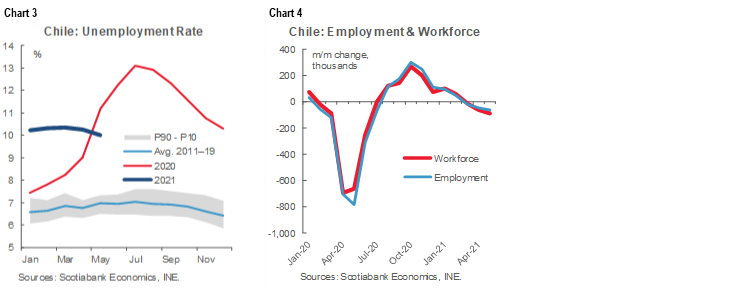

Data released June 30 show the unemployment rate at 10.0% in the three months that ended in May (chart 3), 0.2 percentage points below the rate recorded in April and better than expected by the market (Bloomberg: 10.4%). The decrease in the unemployment rate is explained by a more pronounced fall in the workforce (-1.0%) compared to total employment (-0.8%) (chart 4).

In that context, the decline in the unemployment could give a misleading impression of the health of the labour market. However, several factors could be suppressing formal hiring and informal employability, since during May the economy had higher levels of mobility (restrictions were re-imposed during June). Among these factors is the high degree of household liquidity, thanks to fiscal aid and withdrawals of part of pension funds, as well as fears of exposure to Covid-19, all of which would be preventing people from go out and look for work.

During the quarter that ended in May, about 63 thousand jobs were destroyed, representing three consecutive months of declines in total employment, which increased the gap with respect to the pre-pandemic level (February 2020) to about 1 million fewer jobs.

By sector, the heterogeneity in the recovery of employment continues, with services still lagging the most behind. There is also a greater weakness in the margin in sectors such as commerce and manufacturing. Informal jobs again showed a slight drop in the quarter that ended in May (-1.2%).

—Jorge Selaive, Anibal Alarcón, Carlos Muñoz & Waldo Riveras

COLOMBIA: EMPLOYMENT EDGES UP DESPITE NATIONWIDE STRIKE; BANREP MINUTES REVEAL THE BOARD REMAINS VIGILANT ON INFLATION, FISCAL AND INTERNATIONAL FINANCIAL CONDITIONS; FITCH CUTS COLOMBIA'S SOVEREIGN RATING TO BB+ AS PROSPECTS FOR DEBT REDUCTION IN THE MEDIUM TERM ARE JUDGED LOW

I. Employment edges up despite the nationwide strike

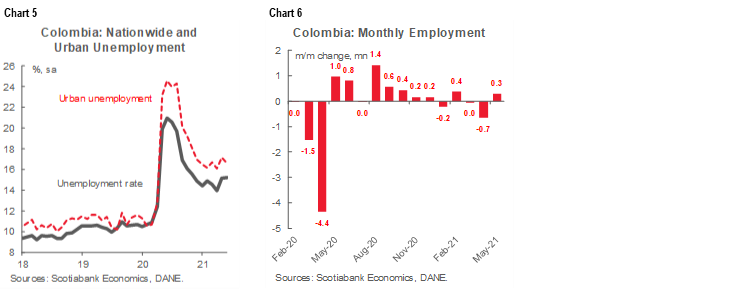

On Wednesday, June 30, the Colombian statistical agency DANE reported May's unemployment rate was 15.6% (not seasonally adjusted) (chart 5). This outcome is below the May 2020 level of 21.4%, but still well above the pre-pandemic (May 2019) level of 10.5%. The urban unemployment rate for 13 major cities was 16.6%, lower than the 18.2% rate expected by Bloomberg’s survey market consensus). On a seasonally adjusted basis, the national unemployment rate was broadly unchanged at 15.2% in May versus 15.1% in April 2021, while the urban unemployment rate surprisingly fell from 17.1% in April 2021 to 16.5% in May (chart 6). Employment results surprised on the upside, since active jobs increased despite disruptions resulting from the nationwide strike.

Despite widespread protests, the labor market improved in May reflecting a relaxation of enforcement of pandemic restrictions in major cities and the recovery of some services related and informal jobs. April saw the worst monthly contraction of active jobs as major cities implemented significant restrictions to combat the third wave of COVID-19. And while the country was under a nationwide strike in May that disrupted the operation of some industries owing to road blockades and frequent demonstrations, the protests also limited the authorities’ ability to enforce lockdown measures.

Total active jobs rebounded by 281 thousand m/m in May (chart 6), but were still down by 1.60 million (-7.2%) relative to May 2019. Inactive workers remained high, with the inactive labor force 10.4% above the pre-pandemic level (16 million in May 2021 versus 14.4 million in May 2019). Despite higher employment in the major cities in May, job losses remained concentrated in urban areas, which accounted for around of 60% of total job losses.

From a sectoral perspective, 78% of employment losses as of May 2021 versus pre-pandemic levels remained concentrated in four sectors: public administration, education, and health group (397 thousand), agriculture (387 thousand), manufacturing sector (-320 thousand), and restaurants and hotels (213 thousand).

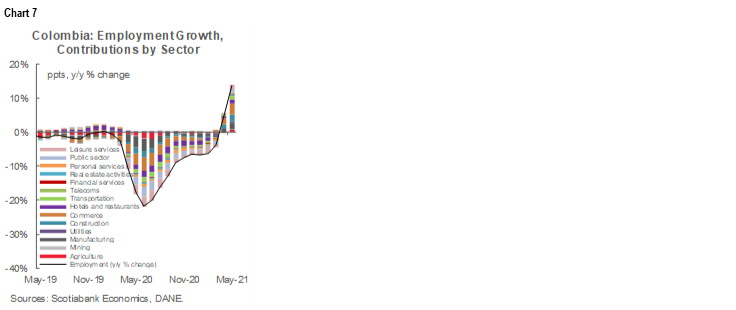

Employment gains came from utilities (81 thousand), financial activities (75 thousand), and transport (25 thousand). It is worth noting that employment in the construction sector has led to the recovery since the pandemic started (chart 7), strongly related to government programs to impulse the housing construction sector.

Key metrics of labour market resiliency and performance include: a wide gap between female unemployment rate (19.4%) and male rate (13%), though it has narrowed recently; concerns with respect to the evolving quality of jobs, with around 47% of employment recovery attributable to higher self-employment (chart 8), and about 26% of hiring related to big companies, while informal employment increased from 46.8% of total jobs in May 2020 to 48.3% in May 2021; high youth unemployment, which DANE data revealed stood at 23.1% in the latest three months to May, with 44.6% of young workers in the informal sector. The fact that 26.8% of the youth population has neither studied nor worked poses a serious challenge to policymakers.

Summing up, despite May’s positive surprise in terms of jobs gains, key characteristics of the labour market remain a concern. We expect the labor market to continue gradually recovering, with a sizeable monthly rebound in June reflecting the relaxation of lockdown measures in major cities since the first week of June. Looking further ahead, the national government is working to speed up its vaccine roll-out and in July private companies will start to vaccinate employees, which will support better economic and employment recovery in the 2H-2021

II. BANREP MINUTES REVEALED THE BOARD REMAINS VIGILANT ON INFLATION, FISCAL AND INTERNATIONAL FINANCIAL CONDITIONS

On Wednesday, June 30, the central bank released the minutes of its most recent monetary policy meeting on Monday, June 28, in which director’s unanimously decided to maintain the benchmark rate at 1.75%. From the minutes, we would highlight that:

- Directors examined inflation developments and said they expect inflation to remain above the 3% percent target until Q1 2022. Current supply shocks that put upward pressure on prices would persist until local and international logistics and production conditions normalize. The board noted that, although inflation expectations remain anchored, expectations would be affected by previous shocks and that it would continue to closely monitor inflation developments.

- One board member said that core inflation would rise if increases in international commodities and logistic prices persist; another member said that persistence in supply shocks would challenge the ability of monetary policy to prevent stagflation.

- The board also discussed the risk of an early start in Federal Reserve rate normalization, highlighting that this scenario reduces monetary policy's capacity to maintain its current expansionist stance. The board highlighted that recent exchange rate depreciation largely reflects idiosyncratic issues, such as sovereign credit rating downgrade and social unrest. That said, the board underscored the importance of approving a fiscal reform.

- Regarding the transmission of simulative monetary policy, one member said that currently available financing sources to the private sector are low, observing that there is probably a crowding-out effect from the public sector.

All in all, despite the unanimous vote to hold rates steady, the minutes were tilted to a more hawkish side. The board will closely monitor inflation and inflation expectation developments versus target. Additionally, international financing conditions and developments regarding Colombia’s fiscal reform would condition Banrep’s counter-cyclical monetary policy. Although we expect inflation to remain within the upper half of the target range (2%–4%), we think the board will find enough macroeconomic arguments to consider starting a hiking cycle begining in September/October 2021. By this time, we expect economic activity to consolidate around stronger growth, inflation developments to provide a clearer picture, and discussions on fiscal reforms. For now, we re-affirm our expectation of a 25 bps hike by September, followed by two more rate increases to close the year with the key policy rate at 2.50%.

III. Fitch cuts Colombia's sovereign rating to BB+ as prospects for debt reduction in the medium term are judged low

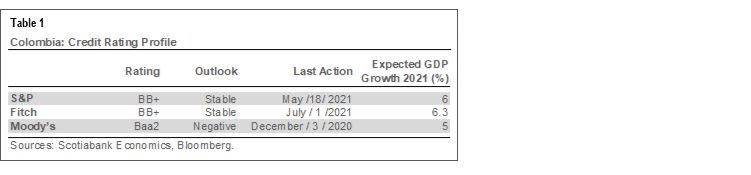

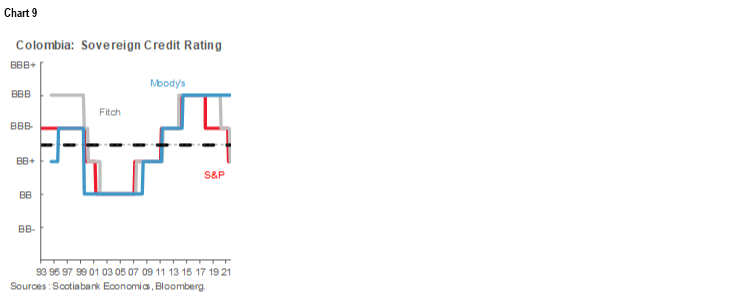

Fitch downgraded Colombia's Long-Term Foreign-Currency and Local-Currency sovereign rating to BB+ from BBB, with a “stable” Outlook (table 1). Fitch projects debt will increase through 2022 with little chance of a reduction over the medium-term, which means that Colombia would maintain a debt-to-GDP ratio above 60%. This ratio is double the 30% of GDP level when Fitch upgraded Colombia to the BBB group in 2011. However, Fitch revised up its 2021 GDP growth forecast from 4.9% to 6.3% and assesses risks to the upside, although uncertainty remains high. The current account deficit is expected to widen to 4.1% of GDP in 2021, with significant financing from the FDI.

Fitch cited several factors behind the downgrade, including the president's low approval rating, which could hinder the reform agenda, dependence on tax administration efforts and disinvestments for fiscal consolidation, and the risk that fiscal reforms to be presented in July could be watered down by the Congress. That said, Fitch projects Colombia's debt –to-GDP ratio to stabilize around 64% of GDP by 2024, though further fiscal reforms are needed before debt can be reduced. This is a significant source of uncertainty, since Fitch also noted that the current social and political situation reduces the possibility to pass any reform to achieve fiscal sustainability ahead of elections in the medium term.

What would trigger further cuts?

- A significant deterioration in debt to GDP metrics versus the BB group

- Lower economic growth prospects, with higher unemployment and poverty levels.

- A sharp increase in external debt relative to GDP.

What would lead to an upgrade?

- Achieving a sustained primary balance leading to a consistent decline in the debt-to-GDP ratio.

- Higher sustained economic growth in the medium term above 3.5%.

- Greater governance and social cohesion that strengthens reform momentum.

Our take:

Fitch's announcement was earlier than expected since they previously said they would wait until mid-July to announce a ratings decision, probably to assess the fiscal reform proposal. Regardless, Fitch's negative take on the Medium-Term Fiscal Framework reflects the projected increase in the debt-to-GDP ratio through 2024 and the fact that a reduction in the debt level is contingent on a new fiscal reform.

Although the FX market had been pricing in the possibility of downgrade, we think volatility will continue in the short term; we will revise our USD COP forecast by the end of the year to the upside, although it would still be lower than current levels. As Fitch also downgraded local currency FI debt, the COLTES market could suffer. However, in the medium term, as new investor groups are likely to enter and equilibrate somewhat the market. That said, we expect the financing conditions on the fiscal side to remain solid.

Minister Restrepo highlighted that Colombia should continue working to achieve higher economic growth and to persevere with fiscal reforms to guarantee medium-term fiscal sustainability and preserve critical social programs. On the political side, the 2022 elections will be critical, as they will define the likelihood of success of key reform.

The last time Colombia lost its investment-grade level was in 1999, and it took until 2011 to reach the investment-grade level again (chart 9). However, we think the current situation is better since Colombia is more open to international markets and local institutions remain sound and stable, improving prospects to reach investment grade again.

—Sergio Olarte & Jackeline Piraján

PERU: INFLATION ROSE IN JUNE, EXCEEDS UPPER LIMIT TARGET RANGE

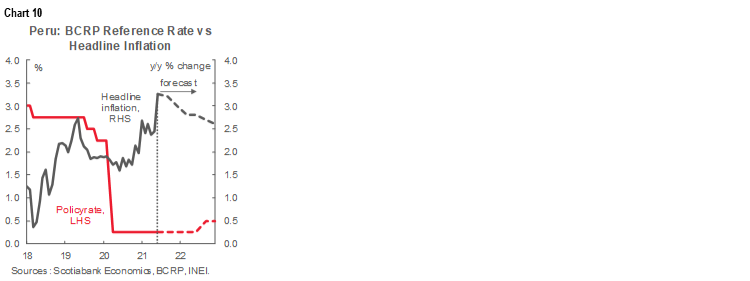

Inflation jumped in June, exceeding the upper limit of the 3.0% target range (chart 10). Inflation printed at 0.52% m/m in June, up from + 0.27% m/m in April, and materially above the Bloomberg consensus of 0.20% m/m and our own forecast of 0.30% m/m. Headline inflation rose from 2.45% y/y in May to 3.25% y/y in June, above the upper limit of the target range (between 1% and 3%) for the first time in August 2017 and reaching the highest pace since April 2017. This rate also exceeds the BCRP's year-end forecast, which had recently been revised from 2.0% y/y to 3.0% y/y. Core inflation rose slightly, from 1.76% y/y in May to 1.89% y/y in June, but remains comfortably below the 2% y/y target for headline inflation.

We see the increase in inflation as linked to rising costs rather than demand. These cost factors include the rise in raw materials and oil, which should be transitory, but have persisted longer than expected, as well as, possibly, more structural issues in global supply chains. These sources of pressures on headline inflation may be are likely to persist for the remainder of the year. In addition, the moderately strong FX depreciation this year should continue to have a lagged effect on inflation. Based on these factors, and considering that inflation during the 2021-1H is already at 2.2%, we are revising our full-year 2021 inflation forecast to 3.5%.

The PEN has depreciated 6.9% against the USD during the 2021-1H, most of it (6.0%) since the first round of voting on April 11. The carry-over effects so far have been moderate but could be more visible in the coming months if pressures on the PEN persist.

Core inflation continues low, however, at 1.9%, just under the midpoint of the target range (2%). As long as this is the case, we do not foresee changes in monetary policy decisions. In the short term, it will be useful to see the behavior of inflationary expectations and the new composition of the BCRP's board, to assess the possibility of any change in the BCRP's reference rate before those expected (mid-2022).

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.