Chile: BCCh held at 0.50%, enlarged FCIC, and broadened collateral to support Fogape 2.0; rise in commercial credit ahead

Colombia: Monetary policy meeting preview—BanRep expected to hold at 1.75% in a split decision

Peru: New partial lockdown measures interrupt recovery; pension reform bill still at early stage

CHILE: BCCh HELD AT 0.50%, ENLARGED FCIC, AND BROADENED COLLATERAL TO SUPPORT FOGAPE 2.0; RISE IN COMMERCIAL CREDIT AHEAD

At its Wednesday, January 27, meeting, the central bank’s Board maintained its monetary policy rate at 0.5%, where it has been since end-March 2020 (chart 1), and kept its dovish bias. It also announced a third stage of its FCIC program (la Facilidad de Financiamiento Condicional al Incremento de las Colocaciones, or the Facility for Financing Conditional on Increases in Lending). This new tranche would have an envelope of USD 10 bn with a term of six months; it would complement the recently approved Fogape-Reactiva program (also called Fogape 2.0), which allows the adaptation of credit lines to the current needs of financial institutions, including through higher interest rates and the possibility of refinancing previous Fogape loans, among other measures. In addition, the BCCh agreed to expand the range of eligible collateral for this new stage of the FCIC program, adding the A5 and A6 commercial portfolio categories with carry state-guarantees. These portfolios (within the normal category) have a higher probability of loss (still less than 10%) than existing approved categories of collateral, although they are considered less risky than the substandard category (which carries a probability of default greater than 13%). This move significantly expands the range of collateral that banks can present in order to access new liquidity under the FCIC and support more loans under Fogape 2.0.

The effectiveness of this latest tranche of the FCIC will depend critically on the rate of lending growth that is required to access the Facility. We expect this threshold to be specified in the coming days, and we anticipate that it will be set somewhat lower than the growth rate tied to the previous two tranches of the FCIC.

These new measures reveal increased concern at the central bank about the recent slowdown in loan growth, especially in the consumer and commercial segments. Figures for the second week of January still do not show any structural changes in lending, which underscores the low demand for investment funds and working capital by companies in the recent Bank Credit Survey.

The analysis of the January meeting statement reveals that the Board is not concerned about possible medium-term inflationary pressures. Its focus is rather on the wide output gaps that still persist in the economy and that are closing at only very gradual rates. We agree with this diagnosis, although we anticipate some temporary spikes in month-on-month inflation in January and February, influenced by recent depreciation in the peso that is pushing up fuel prices; increases in the prices of certain volatile items; and price pressures stemming from boosts to consumer demand driven by withdrawals from the pension funds in the midst of tight supply conditions. The greatest concern for inflation, which the central bank seems to share, relates to the second quarter, when the replenishment of inventories should have concluded and consumer demand ought to begin reflecting the weakness of the labour market—which should lead to a deceleration in month-on-month sequential measures of inflation. All of this should arrive in a context where a third withdrawal of funds pension assets is unlikely, although we do expect delivery of a medium-sized fiscal package financed with existing resources in the Treasury’s cash reserves and/or by a revision of the structural parameters of the cyclically adjusted balance, facilitated by adjustments to copper price assumptions. Inflation should remain well-anchored as level effects will keep year-on-year measures around the BCCh’s 3% y/y target (see our forecasts in the January 25 Latam Weekly).

In the statement, the Board also made a positive assessment of the external environment, highlighting an increase in capital flows to emerging economies, general improvements in stock markets, and improvements in the prices of raw materials, noting the strong recovery of oil prices and the rise of copper prices to around USD 3.60/lb. The Board also observed that the beginning of the global vaccination process has been a positive development, but warned of the wide range in the speeds by which vaccinations are being rolled out across major economies.

On the domestic front, the good performance of the stock market in the last month was called out, together with the appreciation of the peso in late-2020 and the sustained rise in the price of copper. The Board also acknowledged strong sectoral heterogeneity in the economic recovery so far: on the one hand, industries such as commerce and mining have returned to levels of activity similar to the pre-pandemic period, while services continue to lag in an environment where labour-market gaps remain large.

Looking at possible market impacts, we could see some decline in nominal swap rates owing to the Board’s decision to maintain existing stimulus while also introducing new facilities to re-accelerate credit growth. This stance could also precipitate some depreciation of the peso given that the BCCh began to buy USD-spot on Monday, January 18. We continue to expect a first hike from the BCCh in Q2-2022 (chart 1, again).

—Jorge Selaive & Carlos Muñoz

COLOMBIA: MONETARY POLICY MEETING PREVIEW—BANREP EXPECTED TO HOLD AT 1.75% IN A SPLIT DECISION

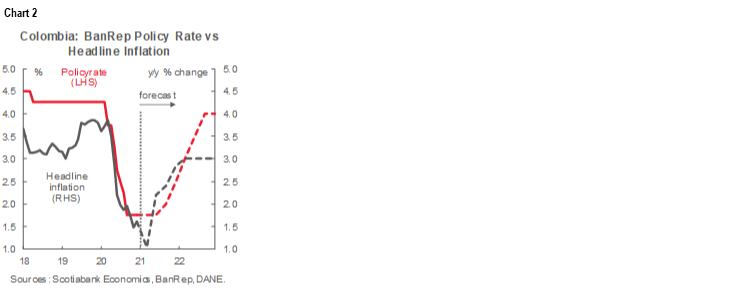

This Friday, January 29, BanRep shall hold its first monetary policy meeting of 2021 and we expect the Board to keep the policy rate at 1.75% in what is likely to be a split decision. At its December meeting, the Board kept the policy rate at 1.75%, where it has been since September 2020, although unanimity broke and two out of the seven members voted for an additional cut of -25 bps. The dissenters argued that inflation is below the target range and that the recovery in economic activity is proving more gradual than anticipated. We expect, along with the market consensus, BanRep to keep the policy rate at 1.75% on Friday (chart 2); however, it is highly probable that the Board will remain split due to the great uncertainty hovering over the growth outlook and inflation normalization.

This meeting is somewhat special for several reasons:

i) It is the first meeting with Leonardo Villar as Governor of BanRep. In our opinion, this supports the idea of policy rate stability for this Friday, since we do not believe that Villar will begin his mandate by surprising the market;

ii) It is probably the last meeting for two Board members—Galindo, who resigned in December owing to family matters, and another member who has not yet been identified. The law allows the President to appoint two Board members once he has been in office for at least two years. These forthcoming changes are neutral for Friday’s decision: we do not think that the spectre of these shifts in Board membership will affect views at this meeting;

iii) Earlier in January, the BanRep staff ran its models and adjusted key projections and forecasts, but we don’t have visibility on how the Bank’s macro views have been altered. This is the most significant source of uncertainty since we haven’t had any hints on how the staff’s GDP growth expectations, inflation forecasts, and neutral rate calculations have evolved. The only clue that we have heard came from Ana Fernanda Maiguashca, who indicated that the neutral rate estimate has likely been reduced due to lower international rates; and

iv) Unanimity has already been broken, which, in regular times, normally foreshadows a change of stance. This would typically point to a cut this Friday, but we think that BanRep will wait a bit longer to see more data on the impact of the new lockdowns and how January inflation reacts to them. January is normally a month when inflation accelerates and Q1 tends to account for about 50% of Colombia’s annual price increases due to indexation.

Additionally, it’s important to remember that, since the December Board meeting, inflation expectations and economic activity projections have not changed significantly. These aspects of the consensus outlook have remained steady despite the imposition of new lockdowns on weekends in Colombia’s most important cities and an upside surprise in the December inflation reading.

The public debate in Colombia is currently dominated by fiscal consolidation. The discussion is focused principally on the possibility of delivering to Congress a new tax reform package during Q1-2021. Policy changes would be designed to fight tax evasion and to increase tax collections without hurting the country’s gradual economic recovery.

All in all, anticipating BanRep’s January meeting is far from being easy given that the year started full of uncertainty around the economic recovery—which opens the door to further cuts in the policy rate. Additionally, fiscal consolidation and reform could put some pressure on the BanRep to deliver further cuts. Having noted all of this, we believe the Board will still decide to keep the policy rate at 1.75% on Friday as it waits for a bit more data on the economic recovery. To this point, we have official data only up to November, most of which was better than expected. But the second wave of COVID-19 and new lockdown measures began in January; as a result, their impact isn’t yet reflected in the numbers.

We maintain our call (see the January 25 Latam Weekly) that the BanRep Board will stay on the sidelines this Friday with a hold at 1.75%, but will leave a door open to further cuts in case economic activity deteriorates. We currently expect a first hike in Q3-2021 (chart 2, again).

—Sergio Olarte & Jackeline Piraján

PERU: NEW PARTIAL LOCKDOWN MEASURES INTERRUPT RECOVERY; PENSION REFORM BILL STILL AT EARLY STAGE

I. New partial lockdown measures interrupt recovery

The government has brought forward a new, partial lockdown in large parts of the country, including the key city of Lima. A host of new measures has been announced that will, for the most part, be in effect from January 31 to February 14. These moves will have an impact on growth and the government’s fiscal accounts.

To compensate for the economic effects of the new measures, the Minister of Finance also indicated, on Wednesday, January 27, a one-month postponement on the payment of income, sales, and other taxes for households and businesses located in those regions affected by the “Extreme Alert”. Furthermore, the government will provide an additional PEN 600 transfer to over four million families.

The main partial quarantine or lockdown measures, published on January 27 in the official gazette as a Supreme Decree, include:

- The current State of Emergency is extended until February 28. Note, however, that the lockdown measures stretch until only February 14;

- Ten regions have been placed under Extreme Alert for the period ending February 14. The economically more important of these regions include: Lima, Callao, Ancash (mining), Junín (mining and agriculture), and Ica (mining and agriculture);

- The use of private vehicles is prohibited in Extreme Alert regions, including Lima;

- Activities that cannot operate in Extreme Alert regions include casinos, restaurants (except for deliveries), sports clubs, educational facilities, hair salons, and travel to and from other regions, all of which are mentioned specifically. The status of other sectors and businesses that that were not considered essential in the past was not specified; and

- Other economically important regions, such as Arequipa, La Libertad, and Piura, will face mild restrictions that would mostly affect mobility, client capacity, and hospitality businesses.

The measures are clear in terms of their implications for mobility standards, but are much less clear on which, if any, major production activities would be locked down. At this point, it is our understanding that major sectors, including mining, agroindustry, construction, public investment, as well as other businesses considered essential, would be allowed to continue operating even under Extreme Alert conditions.

Prior to these measures, most analysts had been upgrading their GDP forecasts for Peru based mainly on two factors: high metal prices going into 2021 and a stronger-than-expected recovery trend since Q4-2020. The lockdown puts a significant damper on the second factor.

Our own forecast of 8.7% y/y GDP growth for 2021 (see the Latam Weekly from January 25) was up for the revision we normally undertake at this time of year, but recent developments will keep our forecast unchanged. We held off on revisions earlier this month as the second COVID-19 wave surged since we believed that this was likely to spawn a government response similar to the one we’ve just seen. This week’s events eliminate the upside risk to our forecast and make it less likely that growth in 2021 will surpass our current 8.7% y/y GDP growth projection. Note that our forecast is lower than consensus (n.b., the Latinfocus consensus forecast stands at 9.5% y/y) and also lower than the BCRP’s forecast of 11.5% y/y, which was released before the risk of the current lockdown had emerged.

The fiscal repercussions of the new contagion control measures should become clearer once the government announces the complete set of new economic safety-net measures for households and support measures for business. It is not yet obvious whether there will be additional actions beyond the already-announced PEN 600 transfer and the postponement of tax payments. One possibility could be additional liquidity and/or funding for businesses.

II. Pension reform bill still at early stage

A Congressional committee has drawn up a new pension reform bill that is likely to be debated in February. The bill does not enter into too much detail and is likely to be discussed on the main floor of Congress floor and modified sometime next month. The bill’s titular reference to an “Integrated Universal Pension System” underscores the intentions of the Committee’s members to eliminate the autonomous nature of the private pension system and to unify it with the state pension system under the authority of a public institution.

The bill has not yet been put on the agenda of the full Congress, but debate is likely to be scheduled for the coming weeks in February. We would expect Congress to invite testimony from experts and authorities on pension funds at the Ministry of Finance, the office of the Superintendent of Banks, and the private pension funds. The resulting discussion could well lead to modifications of certain aspects of the draft bill and add precision to its details. There is also a good chance that the bill will be sent back to the drafting committee for further elaboration.

Eventually, a final draft will be produced for enactment as law. The question is whether the ultimate draft will maintain the significant modifications that the current draft would introduce to the pension system.

Some of the more significant aspects and omissions of the current draft bill include:

- Unification of the public pension system (ONP) and the private system (AFP);

- Creation of an autonomous Authority for the Integrated Pension System. This would likely require a constitutional reform. The new entity would be constituted under the office of the President of the Cabinet (PCM). There are no details yet on how this new authority would work or how its presiding members would be appointed;

- Participation in the new system would be automatic, with personal pension accounts opened for each citizen;

- Private (AFP) managers would not be eliminated, but their role would be limited to managing assets for individual (non-shared) funds;

- Another shared fund is envisioned to be managed by the new Authority;

- Contributors to the private system (the AFPs) would be integrated into the new system and would keep their individual accounts; the full amount of their accumulated funds would be retained. They would, however, be obligated to pay a “solidarity” fee which would be used to augment third-party pensions that fall below a certain threshold;

- Contributors to the public system (ONP) would be integrated into the new system supported by underwriting via a “Recognition Bond” that would be financed through additional sovereign borrowing;

- The draft does not provide a mechanism for commissions, market benchmark determinations, or contribution amounts. These would have to be established by the government; and

- The draft does not determine the way in which the two funds would be operated, such as their investment limits or criteria, and so forth. However, the bill does suggest a role for both the BCRP and the Superintendent of Banks in these areas.

Looking at what comes next, Congress will have to debate and approve a new law on pensions, which may be similar to, but also could be quite different from, the current draft bill. The shape of this process will depend on whether the bill includes some critical elements: the integration of the private and public pension systems; the end of the private system’s autonomy and its subordination to a public institution; and details on the investment policies and strategies under which pension funds would be managed. If these important aspects of the bill are maintained, as they very well could be, then either the government or the private AFPs may challenge the ensuing law at the Constitutional Court on the grounds that the new system would interfere with contracts between private parties.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.