Argentina: Inflation accelerated in December

Chile: A new fiscal package sooner rather than later

Peru: As expected, the BCRP holds at 0.25%

ARGENTINA: INFLATION ACCELERATED IN DECEMBER

In data released from INDEC later in the day on Thursday, January 14, inflation picked up from 3.2% m/m sa in November to 4.0% m/m sa, which was dead on a very late update to the Bloomberg consensus. We had long forecast a 3.6% m/m rise in the month, with upside risk owing to the BCRA’s monetization of fiscal deficits through October; the rapid expansion of the monetary base; and pass-through effects from ARS depreciation. Core inflation’s 4.9% m/m sa print reflected these underlying pressures (chart 1).

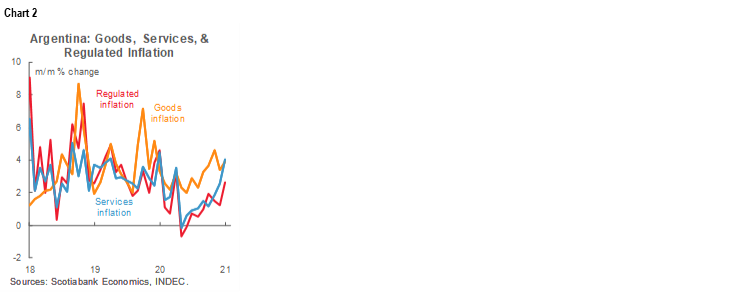

Argentine inflation would be even higher were it not for price controls. While goods prices were up 3.9% m/m sa and services prices rose 4.0% m/m sa, regulated prices rose by only 2.6% m/m (chart 2).

The print brought year-on-year inflation up from 35.8% y/y in November to 36.1% y/y in December, just above our forecast of 35.9% y/y. Core inflation rose from November’s 37.8% y/y to 39.4% y/y in December (chart 3).

The decline in headline inflation from 53.83% y/y in December 2019 to 36.10% y/y at end-2020 is an artefact of level effects and price controls that mask the acceleration in sequential monthly inflation during the latter half of 2020. While monthly inflation averaged 2.15% m/m sa in H1-2020, it accelerated to a mean of 3.07% m/m sa in H2-2020. The rise in inflation would have been even greater were it not for the decline in administered price inflation from

16.9% y/y in December 2019 to 14.8% y/y at end-2020.

—Brett House

CHILE: A NEW FISCAL PACKAGE SOONER RATHER THAN LATER

New COVID-19 cases have increased significantly and we expect the government to bring forward additional containment measures with accompanying fiscal support. Although the authorities have not yet called it a second wave, substantial signs of stress are clearly observable in the health system. Restrictions on mobility have intensified in recent weeks. In this context, a new fiscal package to support families is likely to be announced in March.

The government has at least two ways to finance this spending that is likely to amount to about USD 2 bn (0.8% of GDP).

- On the one hand, the government could call on the committee of experts to review the long-term copper price (LTCP) benchmark for the fiscal rule. The last revision of the LTCP occurred in August 2020, when the spot price of copper was around USD 2.8/lb. At that time, the committee determined an LTCP of USD 2.88/lb. The price of copper has increased significantly—and surprisingly—since that date, reaching USD 3.6/lb most recently. Consequently, knowing the strong co-movement between the spot price and the LTCP determined by the committee of experts, it is very likely that we should see an increase in the LTCP. If the LTCP were to be lifted to, say, USD 3.2/lb, it would open space for an additional USD 1.6 bn of government spending.

- Alternatively, the government has about USD 5 bn available in liquid treasury assets with an important part of them in USD. These resources could be used in a completely discretionary way. If the government chooses this alternative to finance a new fiscal package, it would certainly exert some minor, but significant, appreciative pressure on the peso.

—Jorge Selaive

PERU: AS EXPECTED, THE BCRP HOLDS AT 0.25%

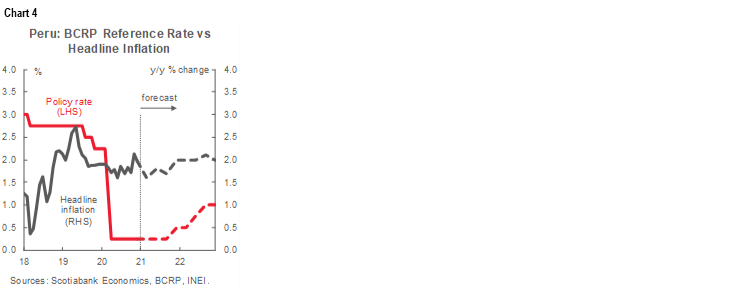

In line with market expectations, the BCRP kept its reference rate unchanged at 0.25% for a ninth consecutive time at its monetary-policy meeting on Thursday, January 14 (chart 4). However, it signalled that it is looking to reduce long-term rates. It reinforced its strongly expansionary stance by activating interest-rate swaps for long-term loans in an effort to bring about lower yields, particularly for mortgage loans.

In its policy statement, the BCRP noted that inflation should stay within its target band over the next two years despite the past year’s massive growth in the monetary base (chart 5). Inflation is expected to remain close to the 2% y/y midpoint of the target range during the early months of 2021, but it could fall toward 1.5% y/y in the lower part of the range at year-end due to an expectation that economic activity would remain below potential. In contrast, full-year 2021 inflation expectations are at 1.9% y/y, similar to our forecast of 2% y/y (chart 4, again).

In the short term, the BCRP warned that business expectations had moderated in December after some rebound during previous months. For 2021, the BCRP expects an economic recovery of 11.5% y/y higher than the 11.0% y/y projected in September, and more optimistic than our 8.7% y/y forecast.

Regarding the FX market, the BCRP sold USD 177 mn in the spot market and its derivatives offers outstanding were expanded to USD 65 mn in January, highlighting the longer-term tenors in the exchange swaps, i.e., from 3 months to 6 months, due to the limited appeal of short-term hedging. The PEN has appreciated by 0.2% YTD. The FX market is still marked by a record deficit of

USD 3.4 bn in the cash position of the banking system. This keeps the exchange rate under pressure and prevents it from reflecting fundamentals.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.