Argentina: November industrial capacity utilization hits two-year high

Chile: New central-bank program to increase international reserves; CLP could rise above USDCLP 750 in the very short run

Mexico: December formal jobs report confirms record cumulative employment losses

Peru: Government unveils new, mostly underwhelming, COVID-19 restrictions

ARGENTINA: NOVEMBER INDUSTRIAL CAPACITY UTILIZATION HITS TWO-YEAR HIGH

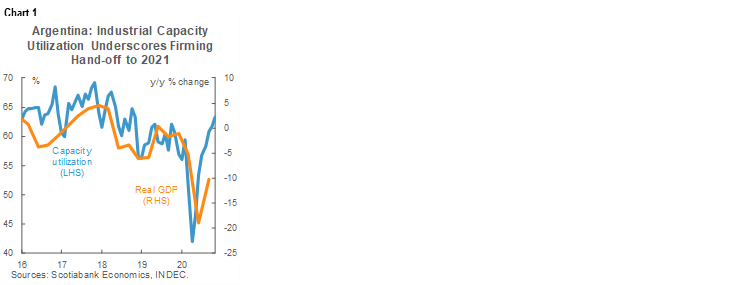

Argentina’s industrial capacity-utilization rate rose from 61.8% in October to 63.3% in November, its highest level since November 2018 (chart 1). This rate is marked by substantial seasonality in non-pandemic times and has fluctuated in recent years between December’s holiday-induced lows around 56% to highs in the mid-60s. Amidst April’s most comprehensive lockdowns, the rate fell to 42%, but has been on an uninterrupted rise since then. The revisiting of levels of capacity employment last seen two years ago coincides with November’s return to positive year-on-year growth in industrial production for the first time since the pandemic took hold in March, which we detailed in the January 12 Latam Daily. The ongoing rise in industrial capacity utilization adds to year-end evidence of strengthening domestic demand and a firming hand-off to 2020, but this is set to be undermined by rising new COVID-19 case numbers.

—Brett House

CHILE: NEW CENTRAL-BANK PROGRAM TO INCREASE INTERNATIONAL RESERVES; CLP COULD RISE ABOVE USDCLP 750 IN THE VERY SHORT RUN

I. Central bank announces a program to increase international reserves by USD 12 bn

On Wednesday January 13, the Central Bank of Chile decided to initiate a gradual program of replenishment and expansion of its FX reserves to strengthen the country’s international liquidity position in preparation for the end in 2022 of Chile’s existing arrangement under the IMF’s Flexible Credit Line (FCL). The goal of this initiative is to increase the level of international reserves to around 18% of GDP, which implies that the BCCh will buy around USD 12 bn (chart 2).

In 2020, the Board of the BCCh considered it necessary to strengthen its international liquidity position in order to mitigate the effects of the potential materialization of financial risks for the country. Therefore, the Bank obtained in May of last year an arrangement under the FCL for almost USD 24 bn, with availability for 24 months.

Considering that the FCL is a precautionary and temporary arrangement, which expires in May 2022, and that the prevailing international financial conditions are appropriate, the Board has considered it is prudent to start now a process that will allow the BCCh to fulfill the insurance function of the FCL through the gradual accumulation of international reserves.

Starting on Monday, January 18, the central bank will implement a gradual foreign exchange purchase program for a total of USD 12 bn. Of these, USD 2.55 bn corresponds to the replacement of reserves used in the intervention plan that was executed between December 2019 and January 2020 following the October 2019 social outbreak; the remaining USD 9.45 bn balance represents the amount necessary to increase reserves to the equivalent of around 18% of GDP. This program will be executed over a period of 15 months in order to be completed by the time of the expiry of the FC arrangement through regular purchases of foreign currency to the tune of USD 40 mn per day through competitive auctions.

II. Our economic view

Our estimates indicate that for each USD 1 bn the central-bank purchases, the exchange rate depreciates by an increment of between USDCLP 2 and 3, all other things being equal. Therefore, the peso could weaken on a transitory basis to USDCLP 750 with much of this depreciation happening a few days after the announcement. We don’t rule out weaker levels for the CLP if there are global changes in risk sentiment or changes in carry trade positions by foreign investors, which we discuss below.

With this, the central bank will intervene in the FX market whenever the real exchange rate is at 97 (index 1986=100), around 3% higher than its historical average (chart 3), which in our view is an appreciated level given that the Chilean economy is going through a severe adjustment process and there are still wide output gaps stemming from the crisis caused by the pandemic. A couple of months ago the central bank noted that the equilibrium real exchange rate had depreciated as a result of the latest crisis.

This announcement implies that the central bank is not worried about medium-term inflation. On the contrary, the BCCh doesn’t consider recent inflationary pressures set off by the two rounds of withdrawals of almost USD 30 bn in pension assets as permanent. The FX purchase program could even point to some disinflationary concerns stemming from the recent appreciation of the peso in a context where the labour market remains weak and economic, sanitary, and political uncertainty is still high.

The central bank has also announced that it will not completely sterilize its FX interventions through the sale of bonds. The exact extent of planned sterilization is unknown, but the BCCh has indicated that the financial conditions needed to completely sterilize its international currency purchases have not been realized. Moreover, the BCCh Board has expressed a dovish bias in recent minutes. Therefore, the impact on prevailing policy rates should be limited.

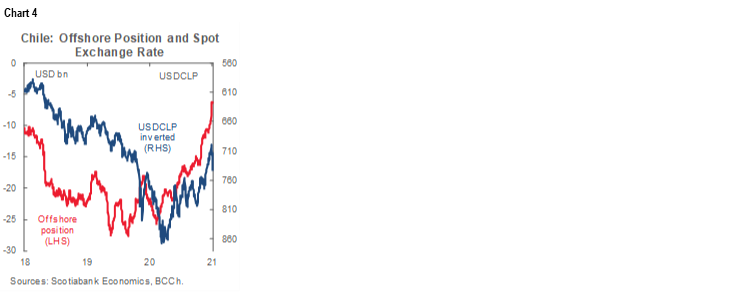

At the same time, off-shore positions have increased their exposure to the CLP in recent months, which has intensified risks of depreciation if these positions are unwound. We will have to wait and see if this announcement will cause a sell-off of non-residents’ positions and further depreciate the CLP. In fact, the non-resident position on derivates/forwards reached USD -6.2 bn on Tuesday, January 12, after reaching USD -16 bn in early-November. Therefore, foreign investors bet in favour of the CLP by USD 10 bn in just a couple of months (chart 4).

It is worth mentioning that the BCCh’s planned accumulation of reserves worth USD 12 bn comes at the same time as the Treasury’s plan to liquidate USD 3 bn of the sovereign funds and USD 6 bn of foreign bonds issued abroad in foreign currency in order to finance government expenditure under the 2021 budget. It may be that the announcement of USD liquidation by the Treasury has already been priced into the CLP, although we doubt this is the case since the market was not entirely aware of the scale of the existing USD 6 bn in external bond issuance.

—Jorge Selaive, Carlos Muñoz, & Waldo Riveras

MEXICO: DECEMBER FORMAL JOBS REPORT CONFIRMS RECORD CUMULATIVE EMPLOYMENT LOSSES

Data from the IMSS (Mexican Social Security Institute) released on the afternoon of Tuesday, January 12, showed that Mexico’s formal jobs numbers declined by -277,820 positions from November, the smallest sequential drop for any December since 2014 (-1.4% m/m), a month in which employment numbers typically fall. With the December data, the cumulative loss in formal positions in 2020 amounted to -647,710 (-3.2% y/y), the biggest single-year decline since 1995 (chart 5).

Country-wide formal jobs summed up to 19.774 bn at end-2020, of which 86% were permanent jobs and the remaining 14% were part-time jobs with social-security benefits. The number of employers registered with the social-security system fell by -2,847, equivalent to an annual change of -0.1%.

Growth in nominal salaries moderated slightly from 7.94% y/y in November to 7.90% y/y in December, but this was still a record pace for any December in recent years. In real terms, the average pace of salary growth rose from 4.5% y/y in November to 4.6% y/y in December, boosted by low inflation at the end of 2020.

The weak performance of the labour market during 2020 reflects still fragile economic conditions that could delay the forecast recovery in 2021. Labour-market weakness is compounded by limited fiscal support from the national government to help businesses and households get through the pandemic, the lack of confidence amongst private-sector actors in some of the policies adopted by the authorities, and new restrictions implemented to mitigate the spread of COVID-19.

—Miguel Saldaña

PERU: GOVERNMENT UNVEILS NEW, MOSTLY UNDERWHELMING, COVID-19 RESTRICTIONS

During a press conference on Tuesday, January 12, President Sagasti announced a new strategy to confront COVID-19. According to Mr Sagasti, the government views Peru as being in the early days of a second wave of COVID-19 (chart 6). As a result, the government has designed a differential response by region according to the degree of local virulence as given by the R ratio (i.e., the effective reproduction number). Each of Peru’s 24 regions will fall into one of three categories: moderate, high, or very high alert. Half of the regions and Lima have already been placed on high alert.

The restrictions for each category are rather mild and not significantly different from those already in place. For high alert regions, such as Lima, the existing curfew will begin earlier, at 9pm instead of 11pm, and continue to last until 4am. Capacity levels at businesses that cater to the public will be pegged at between 30% and 50% of full-capacity, depending on the establishment. This is only mildly lower than current capacity limits. Finally, private vehicles will still not be allowed to circulate on Sundays. None of these measures will have a significant marginal impact on the economy. Restrictions are somewhat harsher for the six very high alert regions. Although some of these regions are important in terms of mining and agroindustry, the restrictions should not interfere greatly with any of these businesses. Pres. Sagasti also stated that the restrictions will be in place until January 31, after which they can be either expanded or reduced.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.