Mexico: Outlook improves in Banxico survey; remittances hit new record

Peru: Raising our inflation forecast for 2021; early positive signs on December 2020 growth

MEXICO: OUTLOOK IMPROVES IN BANXICO SURVEY; REMITTANCES HIT NEW RECORD

I. Banxico Survey expects slightly better recovery for 2021

In Banxico’s Survey of Economists for the first month of 2021, released on Tuesday, February 2, the outlook for GDP growth became slightly more positive. Respondents anticipated further GDP expansion to average a 3.74% y/y rebound in 2021, up from an average of 3.54% y/y in the December survey. The improvement in the forecast appears to reflect stronger recovery in external demand, particularly from the US, rather than a recovery in the domestic market where the growth impulse remains weak.

In other major features of the survey, we noted that:

- The expected economic recovery in 2022 improved slightly from 2.59% y/y to 2.61% y/y;

- Headline inflation expectations increased marginally for the end of 2021 and 2022 to 3.65% y/y and 3.55% y/y, respectively, but remain within the monetary-policy target range of 2–4% y/y;

- Forecasts for the exchange rate at the end of both 2021 and 2022 appreciated with respect to the December survey and the Mexican currency is now expected to close 2021 at USDMXN 20.18 and 2022 at USDMXN 20.59;

- As for monetary policy, the results showed that from Q1-2021 and throughout the forecast horizon, most specialists anticipate an interbank funding rate lower than the current target rate of 4.25%: the median and mode for end-2021 are both 3.75%. Analysts expect the benchmark policy rate to rise thereafter to 4.25% by end-2022. The next monetary-policy meeting is scheduled for February 11;

- The outlook for the labour market also improved; analysts now anticipate a recovery of 382k formal jobs by the end of 2021 and the creation of 390k jobs during 2022. Although an increase in formal jobs is positive for the economy, the number of new jobs expected for this year would not be enough to compensate for the -647k positions lost during 2020. In addition, the extension of public-health-related restrictions to more states could negatively affect the recovery of the economy’s dynamism and employment growth;

- Regarding the forecasts for the public deficit as a percentage of GDP, the average deficit projected for end-2021 narrowed from 3.85% in December to 3.41% in January; for 2022, it is projected to reach 3.25%; and

- The main factors expected to hinder Mexican economic growth in 2021 were domestic economic conditions (44%), governance (31%); and public finances (12%).

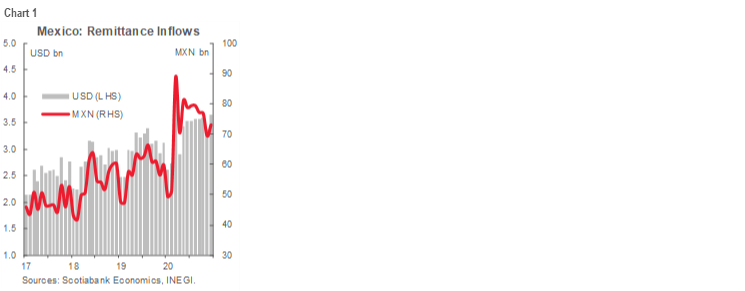

II. Another record for remittances in December

According to data released by INEGI on February 2, remittances totaled USD 3.7 bn in December and USD 40.6 bn for the whole of 2020 (chart 1)—record flows for both periods. Compared with the year before, December’s remittance inflows were up 17.4% y/y, which put 2020’s number up 11.4% y/y compared with 2019. The number of transfers in December, at 10.8 mn, was also a record, which pushed growth in the number of transactions up from 9.2% y/y in November to 13.2% y/y in December. The average value of each transfer, at USD 339, represented a moderation in annual growth from 5.8% y/y in November to 3.7% y/y in December. Remittances were not hit by recent hiccups in the US labour market.

Looking ahead, further economic recovery in the US, supported by a new fiscal stimulus package, should continue to drive strong remittance flows into Mexico during 2021.

—Miguel Saldaña

PERU: RAISING OUR INFLATION FORECAST FOR 2021; EARLY POSITIVE SIGNS ON DECEMBER 2020 GROWTH

I. We’re raising our inflation forecast for 2021 to 2.6% y/y from 2.0% y/y

In the Latam Daily for Tuesday, February 2, we reported that 12-month inflation to January reached 2.7% y/y for Lima, which is usually taken as the benchmark official figure. After further review of the underlying data, we are now raising our forecast (see the January 25 Latam Weekly) for 2021 inflation from 2.0% y/y to 2.6% y/y (chart 2).

Inflation has consistently surprised to the upside over the past few months. For a long time during 2020, we, market consensus, and the BCRP had been forecasting low inflation based on the argument that COVID-19 and the consequent lockdown would hurt demand. The BCRP had even forecast at one point that 2020 inflation would be nil. In the end, it came in at 2.0% y/y.

The main driver for inflation seems to be import prices owing to pass-through effects from the weak PEN. Fuel and soft commodity prices (particularly maize and soybean-based animal feed) have risen in USD terms and the weakness of the PEN has exacerbated these price pressures in local-currency terms. The full extent of the eventual impact of these price increases has probably not yet been felt, particularly since commodity prices have continued to rise in 2021 and are set to increase further. Moreover, there is likely to be a lag in the full price pressures they induce across the economy as they filter up the value chain. Health-product prices have also contributed to inflation and this is also likely to continue going forward given the ongoing second wave of COVID-19.

The BCRP is also adapting its outlook on inflation. In its December Inflation Report, the BCRP raised its forecast for 2021 from 1.0% y/y to 1.5% y/y. This was before the January print, although the central bank’s relatively modest inflation outlook may also reflect the fact that only the headline inflation rate is rising, while core inflation has remained at 1.8% y/y.

Our new inflation forecast of 2.6% y/y is still within the BCRP target range of 1% y/y to 3% y/y. For this reason, and more broadly because the main concern of the BCRP today continues to be the provision of stimulus to support the recovery of the economy, we do not see the BCRP raising its reference rate in 2021; we maintain our forecast that a rate hike will not be forthcoming before mid-2022 given that we still foresee inflation settling to around 2% y/y in 2022. However, we are not quite as confident in our view as we were previously as we see more uncertainty in the inflation trend than before.

II. Early growth indicators for December 2020 more positive than negative

The following early growth figures and indicators for December were released on February 2 by the National Statistics Institute and skewed more positive than negative.

- Fishing soared 108.5% y/y in December. The month was the height of the fishing season, although activity in January should also have been strong. This alone would add nearly one full percentage point to GDP growth in December.

- Mining fell -2.5% y/y. This was unsurprising.

- Oil & gas fell -10.9% y/y, although the sector does not carry a large weight in overall GDP. Oil production in particular has been declining for some time.

- Domestic cement consumption was up 21.5% y/y in the month. At the same time, public investment rose 26.7% y/y. The combination implies that construction GDP growth in December could have been close to 20% y/y.

All in all, these figures imply that December GDP growth likely fell somewhere between -0.5% y/y and -1.0% y/y, which would compare nicely with -2.8% y/y in November.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.