- Colombia: Q3-2021 balance of payments—deficit keeps widening, while FDI reaches the best level since the pandemic began

- Peru: Inflation pauses, but rate hikes to continue; another political scandal erupts

COLOMBIA: Q3-2021 BALANCE OF PAYMENTS—DEFICIT KEEPS WIDENING, WHILE FDI REACHES THE BEST LEVEL SINCE THE PANDEMIC BEGAN

On Wednesday, December 1, the central bank (BanRep) released Q3-2021 current account data, showing a quarterly deficit of USD 5.12 bn, equivalent to 6.4% of GDP (chart 1), the largest deficit since 2016. This result reflects a higher trade deficit and higher income account outflows, both of which are fueled by the economic recovery. The trade deficit includes vaccine imports, which should moderate over time. The public sector was the main source of financing, though we expect FDI to contribute more in 2022.

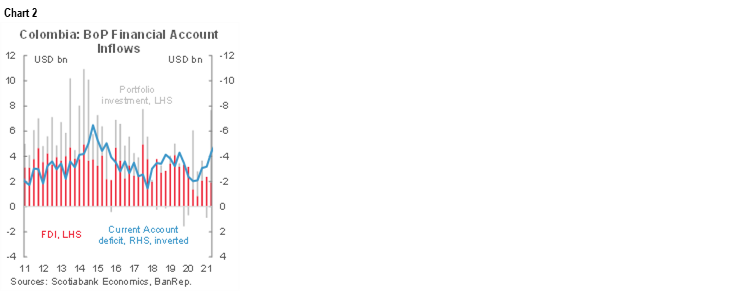

Portfolio investment featured net outflows of USD 556 mn (chart 2). A moderation of capital inflows (USD 982 mn) reflecting reduced appetite from offshore agents for COLTES was completely offset by portfolio investment outflows (USD 1.6 bn). Net FDI reached the highest level since the pandemic began (USD 2.6 bn), pointing to a strong recovery after the uncertainty generated by the social unrest in May/June. Remittances remained high but broadly unchanged versus the previous quarter.

The public sector was the main source of financing, reflecting the use of proceeds from the sale of ISA to Ecopetrol and dollar purchases by BanRep deposited into government accounts.

The balance of payments in Q3-2021 reflected the ongoing recovery, as imports of raw materials and capital goods increased, as well as higher import prices. While financing has thus far been available to support the higher current account deficit, for long-run current account sustainability and to ensure the continued recovery of domestic demand, FDI must return to pre-pandemic levels so that it is the main source of finance for imports. Our end-2021 forecast for the current account deficit sits at 5.2% of GDP, though risks are tilted to a wider deficit. Ahead of 2022, we think imports should decrease somewhat, especially those related to vaccines, mirroring lower government financing needs amid better economic activity and higher tax collections.

Additional information by lines in the current account:

- The overall trade deficit stood at USD 5.5 bn, mainly owing to a higher deficit in the trade of goods (USD 3.8 bn), while the services deficit widened by USD 105 mn to USD 1.8 bn. The total combined goods and services trade deficit in Q3 was the largest in recent history. Exports were closer to pre-pandemic levels (USD 12.9 bn), while imports (USD 18.5 bn) are 13% above pre-pandemic;

- Goods exports expanded by 15% q/q and 38% y/y to USD 10.9 bn. Mining product exports led overall export growth, with higher international prices driving export values, as volumes have, in fact, continued to fall;

- Goods imports increased by 12% q/q and 45.9% y/y, consistent with the recovery in domestic demand and higher international prices in raw materials and capital imports;

- In the services balance the Q3 trend continued, with higher growth in tourist package deals, and IT services exports, such as call centers the best performer, increasing by 31% y/y in the YTD up to September-2021;

- Income account outflows increased and reached the highest levels since the pandemic began, showing improved export dynamics which boosted profits across Colombia’s main economic sectors, especially those sectors with high FDI, such as oil and mining and financial services; and

- Remittances inflows stabilized in a historical high (USD 2.1 bn) in Q3-2021.

On the financing side, FDI increased in the third quarter, though the public sector remains as the main source of financing through assets sales and monetization of credits and cash in foreign currency.

Portfolio investment stood at USD 556 mn, increasing 72% y/y, but falling 109% q/q, reflecting decreased interest from offshore investors in the COLTES market and higher outflows from residents.

FDI inflows stood at USD 2.8 bn, increasing 47% q/q, but still below pre-pandemic levels by 20%. In the YTD FDI inflows were concentrated in financial services (25%), transport and communication (20%) the manufacturing sector (16%), and the oil and mining sector (12%). Q3’s FDI inflows showed and strong recovery after the significant impact of the nationwide strike in May which brought uncertainty. We expect FDI to recover gradually due to the consolidation of domestic demand recovery, however the presidential election can post a challenge in H1-2022.

—Sergio Olarte & Jackeline Piraján

PERU: INFLATION PAUSES, BUT RATE HIKES TO CONTINUE; ANOTHER POLITICAL SCANDAL ERUPTS

I. Inflation takes a breath, but we still expect a new rate increase next week

Peru’s inflation increased 0.36% m/m in November, higher than the Bloomberg consensus of 0.30% m/m, but below our forecast of 0.50% m/m. Headline annual inflation slipped from 5.8% y/y in October to 5.7% y/y in November (chart 3), taking a breather in its upward trend. This marks the sixth consecutive month in which inflation exceeded the upper limit of the central bank’s target range (between 1% and 3 %); and at levels not seen since the beginning of 2009. Inflation remains well above of the BCRP’s inflation forecast of 4.9% for this year. All this adds to the pressure for further increases in the reference rate.

November’s inflation is in line with our inflation forecast of 6.5% for the full year in 2021, as December should see a moderate uptick. We maintain our forecast of 4.5% inflation for 2022.

Core inflation continued to pick up, going from 2.8% y/y in October to 2.9% y/y in November, approaching the upper limit of the target range (3%). Wholesale inflation, linked to production costs, remained high, close to 14% y/y, the highest rate in 27 years. We see cost pressures likely to continue to persist over the next year. The PEN depreciation accelerated slightly, from 12% y/y in October to 13% y/y in November, in a context of persistent political uncertainty. The carry-over effects of the FX on inflation could also persist in the coming months, adding to the growing concerns at the BCRP.

Over the last four months, the central bank raised its benchmark rate by 175 basis points to 2.00% and increased reserve requirements twice, signaling that it would continue to withdraw the monetary stimulus. The BCRP has been acting reactively. The pause in the pace of inflation and the recent appointment of a more technical BCRP’s Board could allow it to take a more preventive stance, so we believe that further increases in the policy rate will be necessary for inflationary expectations to return to the target range. We expect a 50 bps increase at the next BCRP meeting next week, on December 9.

—Mario Guerrero

II. Peru’s scandal of the week

Over the weekend the media reported on clandestine meetings that President Castillo had been holding in a private house (which he called his home “mi domicilio”) in Lima. The issue has escalated quickly, as it became known that people who entered the place during President Castillo’s time there included individuals who were soon afterwards awarded tenders for government investment projects. Castillo, on Monday, gave a very brief three-minute conference on the topic, but stated only that the meetings were private, or “personal”, and that nothing untoward occurred. This has not placated the press and opposition politicians. Decrying an inconsistency in claiming private meetings with businesspeople who later were awarded tenders, they have made calls for the Attorney General’s office to get involved. These ongoing events are occurring only days before the December 7 date in which Congress is expected to vote on beginning impeachment procedures for President Castillo. Political analysts widely believe that the 87 votes needed for an impeachment would not be forthcoming, but that it has become, at the same time, more likely that the 52 vote threshold needed to initiate the impeachment procedures will be met, which would allow Congress to grill President Castillo.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.