- Chile: Presidential race takes shape as nine candidates vie for November first-round

- Peru: Q2 results point to strong private investment at the same time as short-term capital outflows; Congress awaits the new cabinet

CHILE: PRESIDENTIAL RACE TAKES SHAPE AS NINE CANDIDATES VIE FOR NOVEMBER FIRST-ROUND

On Monday, August 23, the presidential candidate registrations officially closed and the main political forces registered nine candidates for the November 21 election. As we discussed in yesterday’s Latam Daily, the centre-left bloc chose Yasna Provoste as its candidate for the November election, who will seek Chile’s presidency alongside the representative of Social Convergence (left), Gabriel Boric, and the independent (centre right) Sebastian Sichel. Also, the Electoral Service (Servel) confirmed the candidacy of José Antonio Kast (far-right), Marco Enríquez-Ominami (Progressive Party), Franco Parisi (People’s Party), Diego Ancalao (The People’s List), Eduardo Artés (far-left) and Gino Lorenzini (independent). The Servel will now proceed to vet the nominations before considering candidates as officially registered by September 2.

—Anibal Alarcón

PERU: Q2 RESULTS POINT TO STRONG PRIVATE INVESTMENT AT THE SAME TIME AS SHORT-TERM CAPITAL OUTFLOWS; CONGRESS AWAITS THE NEW CABINET

I. Q2 results point to strong private investment

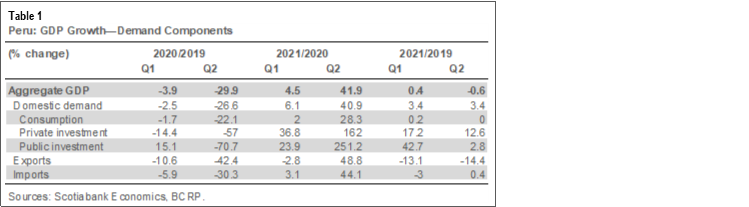

Peru’s central bank (BCRP) released the official GDP and domestic demand growth figures for Q2-2021 on August 20. As for GDP growth, the strength of private investment was the greatest surprise, especially considering signs of domestic outflow of short-term capital (more below).

GDP growth of 41.9% y/y in Q2 (table 1) was not all that surprising, as monthly results had already been released and given the low base of Q2-2020—a time of COVID-19 lockdowns. What is particularly encouraging, in comparing with 2019, is that, exports aside, all demand components of GDP were up. Domestic demand was 3.4% greater than in pre-COVID-19 Q2-2019.

As mentioned above, private investment was the greatest surprise: a huge 12.6% increase over the same quarter in 2019. Even though 2019 was not a great year for private investment, such a large increase amidst the current political turbulence is surprising. Especially considering that investment in mining was 9.8% lower than in 2019, and, thus, the underlying driver was non-mining investment, which was up 16%.

Consumption has also been holding up well, up a mild 0% to 0.2% in the first half of 2021 over 2019. This belies a weakish labour market, and reflects the tremendous amount of resources that have reached households through public transfers and withdrawals from pension and labour funds.

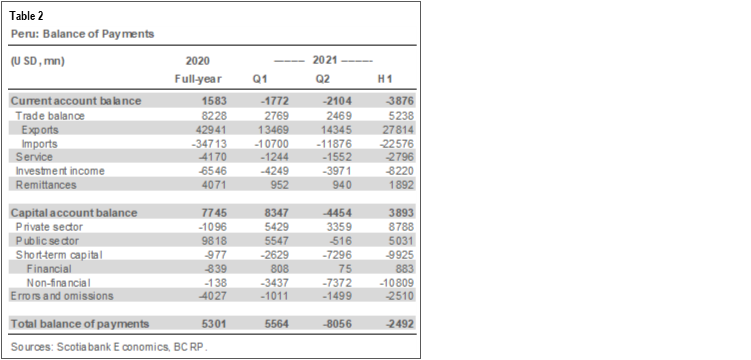

II. External accounts weakened in Q2, on short-term capital outflows

The BCRP also released balance of payments results for Q2. Perhaps the most notable data had to do with the reported outflow of short-term capital from non-financial institutions (that is, businesses and households, and excluding banks and offshore funds) of USD 7.4 bn for Q2, and USD 10.8 bn for the first half of 2021 (table 2). These are huge amounts. The previous record for a net outflow from businesses and households dwarfs in comparison, at USD 3.0 bn, and this was for the full year 2018. Data shows that the outflow of short-term capital was mostly from domestic sources. In comparison, outflows attributed to offshore funds disinvesting out of local PEN instruments—mostly sovereign bonds—was tame, only USD 987 mn for Q2 and USD 1.9 bn for the first semester. Together, the two sources of outflow amount to USD 11.8 bn, which goes a long way in explaining the strong depreciation of the PEN in this period.

Other balance of payments accounts were much more favourable. The trade balance is on its way to meet our forecast of USD 12 bn for the year, and a new record, thanks to metal prices. High metal prices are also behind the increase in investment income, which accounts for earnings of offshore companies, especially mining. This factor, plus higher service costs, led by a sharp increase in freight costs, caused the current account deficit to slide into a deficit so far this year.

III. Defining political events ahead as Congress awaits the new cabinet

This is a week of definitions. Maybe. In principle, three things should occur in the next seven days until the end of August, although only one is actually scheduled. First, this coming Thursday, August 26, the cabinet is scheduled to formally present itself before Congress, outline its government plan, and request a vote of confidence. Second, by August 31, the Ministry of Finance should submit the 2022 fiscal budget to Congress. Third, the designation of the BCRP’s Board of directors is still pending.

1. The vote of confidence: Guido Bellido, the Head of the Cabinet, is not seen favourably by much of Congress, therefore a vote of confidence is not a given. A lot may depend on how moderate he is in his speech and proposals. Bellido has been sending mixed messages of late, but overall appears to have softened his tone. There is a good chance that he will seek to appease Congress, rather than confront it, but this cannot be assured until the actual delivery is made.

The government did, however, take one important step towards appeasing Congress last week when it replaced the Minister of Foreign Affairs, Héctor Béjar, with Oscar Maúrtua de Romaña. Béjar was a far-left figure which seemed intent on reneging on Peru’s recent history of regional alignments, and realigning the country with more leftist countries, such as Cuba and Venezuela. Replacing him with Maúrtua, a long-term diplomat who had held the position of Minister of Foreign Affairs in 2005–2006, is a strong statement on several levels: the government is replacing someone who is inexperienced in foreign affairs, and identified with the far left, with someone well experienced and is a moderate centrist; the switch also reduces the presence of people closely allied with Vladimir Cerrón and Peru Libre’s leadership, inside the cabinet, thereby modifying the balance of power. Furthermore, the appointment of Maúrtua de Romaña, a technocrat, brings into question what his designation means with regard to putting governability above the party’s ideology and preferences.

However this may be, the move should, at least, help mollify Congress, and increases the likelihood that the Bellido Cabinet will receive a vote of confidence.

2. The 2022 budget: The budget will shed light on how the government intends to stimulate the economy and implement social programs, while maintaining the goal, already stated by Finance Minister Francke, to bring the fiscal deficit down to 3.7% of GDP. We shall also learn how the government intends to finance its spending programs, and the deficit. This is becoming a bit more of an issue, as conditions to issue debt have deteriorated.

Finally, the budget may tell us if the government is contemplating new taxes, or raising current levies, especially on mining. For any tax change to be in force in 2022, it must be established by law in 2021.

3. The BCRP Board of Directors: Expectations remain high that the current President, Julio Velarde, will be ratified. However, the government’s decision-making process is still uncertain and this is not entirely assured. Given the state of investor confidence, rising inflation and PEN volatility, one would assume that time is of the essence in deciding on this issue, yet it is not perceived as an immediate priority for the administration. In the past, the BCRP Board designations were typically made in August, but this is not set in stone. In 2011 Velarde was not reappointed until October 3.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.