Chile: Best monthly growth for any February since 2010 leads us to reaffirm our forecast of 7.5% y/y real GDP gains in 2021

CHILE: BEST MONTHLY GROWTH FOR ANY FEBRUARY SINCE 2010 LEADS US TO REAFFIRM OUR FORECAST OF 7.5% Y/Y REAL GDP GAINS IN 2021

Chile’s IMACEC monthly real GDP proxy, in its latest release on Thursday, April 1, showed the best sequential growth for any month of February since 2010 at 0.9% m/m sa. This was well above the 0.0% m/m sa expected in the Bloomberg consensus, but represented a slowing from 1.3% m/m sa in January.

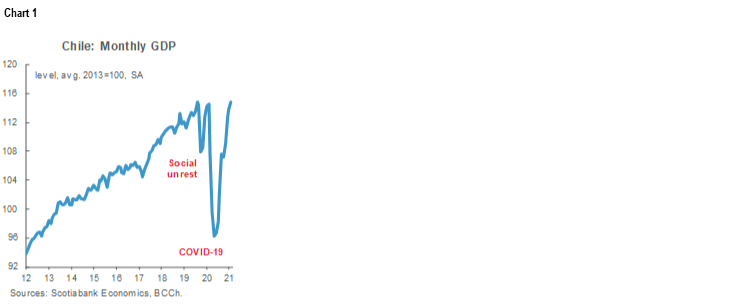

The monthly print resulted in February’s annual growth rate coming in at -2.2% y/y, which was well below expectations owing to level effects stemming from 2020’s leap year. This was the second month in a row in which seasonal/calendar effects had an important influence on the IMACEC activity numbers. We had expected a print of -0.5% y/y, while the BCCh’s own survey (i.e., the Encuesta de Expectativas Económicas, EEE) foresaw 1.5% y/y, and the Bloomberg consensus anticipated 1.6% y/y. Nevertheless, high monthly rates of growth have returned economic activity to levels comparable to a year ago (chart 1), making Chile one of the world’s first countries to attain pre-COVID-19 levels of monthly GDP.

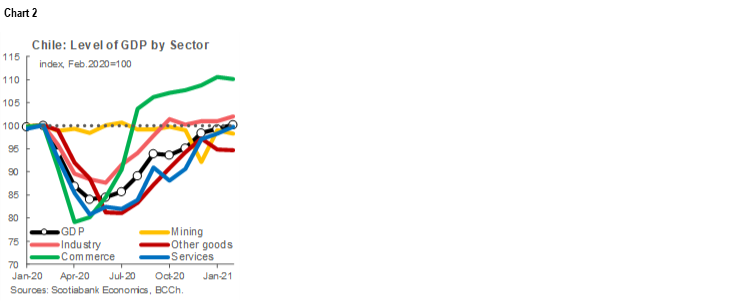

The non-mining component of GDP grew sequentially even faster in February, hitting a rate of 1.1% m/m sa. The recovery of services, with growth of 1.5% m/m sa, stood out as it is one of the drivers of Chile’s rebound: the print highlighted further re-opening of the economy and rising numbers of people who travelled domestically for their summer vacations. February’s real level of services activity was on par with a year ago in February 2020. Commerce (i.e., retail) also continued to show solid dynamism in February owing to the availability of monies from the second round of pension withdrawals at the end of December 2020 (chart 2).

Recent quarantine measures are likely, however, to lead to new setbacks to GDP in March. We would not rule out the possibility that these effects could continue into April if restrictive measures remain in place beyond the middle of this month.

This note of caution is focused at the sectoral level on mining, which saw a significant annual decline in February (-4.9% y/y). This resulted from a fall in the volume of copper extracted and processed as average mineral grades came down. Additionally, the leap-year effect, where February 2020 had one more day than its 2021 counterpart, had a more pronounced impact in mining than in other major productive sectors.

The seasonal factor surprised us negatively: it was markedly smaller than that observed for any February in recent years (chart 3). We believe that this was due to more pronounced seasonal effects related to last year’s extra day in February than we had anticipated in our models. Still, the strong month-on-month gains in February provided a good hand-off to the rest of the year.

February marked the fourth consecutive month in which there has been positive sequential growth in non-mining GDP (chart 4). In fact, aside from October 2020, non-mining GDP has seen month-on-month gains since June last year. It appears that the economy has adapted to the “new normal” of greater social distancing and mobility restrictions.

Our baseline forecast of a 7.5% y/y expansion of Chile’s real GDP in all of 2021 remains solid. It takes account of an estimated -3% m/m sa sequential contraction in March owing to new public-health measures, which would still leave activity up 4% y/y in the month. Even if we see another seasonally-adjusted, month-on-month pullback in April, it would still be consistent with our 7.5% y/y projection for 2021 as a whole.

Jorge Selaive, Carlos Muñoz, & Waldo Riveras

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.