- Peru: BCRP institutes interest-rate cap; Castillo and Fujimori challenge each other to debate as gap between them narrows

PERU: BCRP INSTITUTES INTEREST-RATE CAP; CASTILLO AND FUJIMORI CHALLENGE EACH OTHER TO DEBATE AS GAP BETWEEN THEM NARROWS

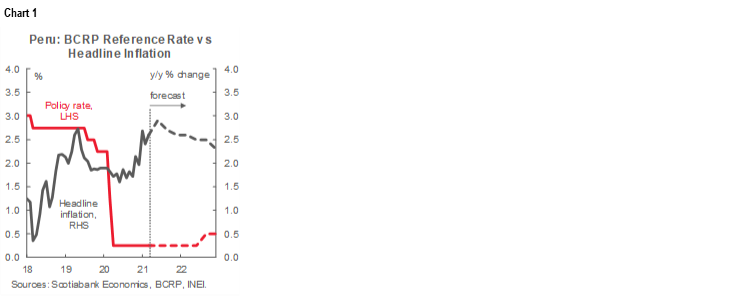

I. Central bank establishes 83.4% interest-rate cap

On Wednesday, April 28, the BCRP (i.e., the central bank) established 83.4% per annum as the ceiling for interest rates on consumer and small-business loans—well above current policy rates (chart 1). The BCRP also provided the methodology it will follow for determining future rate ceilings. The basic rule is that the rate ceiling is to be adjusted every six months to be equal to twice the average rate for consumer loans over the previous two to seven months. In this initial setting, the average rate from October 2020 to March 2021 was 41.7%. Despite the publication of the methodology, it’s not clear how the ceiling will evolve over time since the interest-rate cap itself lowers the average rate for consumer loans. The ceiling will apply from May 10.

The BCRP established this ceiling in keeping with a recent law on the matter developed and passed by Congress. The central bank expressed its concern that the interest-rate cap could leave higher-risk clients without access to credit. The BCRP, in establishing the ceiling, apparently sought to have as little impact on the financial system as possible, while at the same time avoiding an impression that it was following the law only in name. Concurrent with the central bank’s move, public attorneys (i.e., the Procuraduría) for the Ministry of Finance submitted to the Constitutional Court a petition that the law that imposed an interest rate ceiling be declared unconstitutional.

II. Presidential candidates challenge each other to debate as gap between them narrows

The local pollster Datum released today, Friday, April 30, a poll showing Keiko Fujimori narrowing the gap with Pedro Castillo by a third. The poll, undertaken between Tuesday, April 27, and Friday, April 30, showed Castillo adding three points to his share of voter intentions, up from 41% in a previous Datum poll to 44%. Fujimori, however, increased her share more substantially from 26% to 34%, which narrowed the gap with Castillo from 15 percentage points to 10. The share of undecided voters fell from 18% to 11% and the slice of “blank” voters from 15% to 11%.

Our read: this was a sizeable reduction in the gap between the two over only one week. However, Castillo’s lead is still comfortable and, perhaps more importantly, he is not losing votes: he continues to have a fairly high share. As expected, Fujimori is gaining, perhaps even faster than anticipated; but, with Castillo’s support still firm, there is no assurance that she can catch up completely. Unless Castillo starts losing votes, Fujimori will need to garner the support of most of the currently undecided voters and also some of the blank voters to overtake her rival. Even though there is likely to be some hidden support for Fujimori not currently captured in the polls, the run-off remains an uphill battle for her.

Pedro Castillo was taken to a hospital on Thursday, due to breathing problems. This may be due to the stress of the campaign given that Castillo recovered from COVID-19 only in March, although some believe he may be trying to avoid debating Keiko Fujimori on Saturday, May 1. Castillo and Fujimori each challenged each other to a debate in a battle of words over recent days. Castillo dared Fujimori to debate in Chota, a place in Cajamarca that for Castillo would be equivalent to playing on home court. Fujimori accepted immediately and proposed that the debate take place this Sunday, May 2. Castillo countered with a proposal for Saturday, May 1. One wonders how this debate will be organized. Typically, the National Elections Board (Jurado Nacional de Elecciones in Spanish) establishes debate dates, invites the candidates to participate, and undertakes the organization of the event.

Meanwhile, Keiko Fujimori announced the names of part of her “technical team”. Fujimori may have wished to make the point that she actually has a team, in part to underscore the fact that Castillo does not. Castillo has been under great pressure to release names of a viable team, something which he has not been able to do. However, the names released by Fujimori were underwhelming and included controversial figures such as Jorge Baca in charge of economic policy. Baca is suspected of having links to Vladimiro Montesinos, a key advisor to ex-President Alberto Fujimori (1990–2000) and the centre of a range of corruption scandals that eventually brought down Fujimori’s administration. Perhaps as a result of the backlash to the announcements, Keiko Fujimori indicated that Luis Carranza was joining her team. Carranza is a prestigious economist who was Finance Minister during the second Alan García Government (2006–11).

For his part, Castillo has come under fire for saying that he would deactivate Peru’s Defensoría del Pueblo, an institution that has a mandate to defend fundamental rights and ensure that State institutions perform their responsibilities. Put on the defensive on the issue, Castillo backtracked, as has become his wont: he indicated that he would not abolish the Defensoría, but, rather, would “reinforce it to the benefit of the most vulnerable [people].”

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.