Chile: Intense political discussions on a possible third round of pension-fund withdrawals

Colombia: S&P affirmed Colombia’s credit rating at BBB- owing to commitment to fiscal sustainability, but kept outlook negative

Mexico: Headline inflation spiked above consensus in the first half of April

Peru: Government gives green light to withdrawals from worker funds

CHILE: INTENSE POLITICAL DISCUSSIONS ON A POSSIBLE THIRD ROUND OF PENSION-FUND WITHDRAWALS

Chile is experiencing some intense political discussions on a possible third round of pension-fund withdrawals—discussions that will continue in the weeks ahead and could potentially have important implications in the near term for the country’s economic performance and financial markets. First, the bill to allow the withdrawals has been discussed in the Senate, where it was meant to be approved on Thursday April 22: a two-thirds majority had expressed their intention to vote in favour of the bill. However, since the Senate made some modifications to the bill, Congress will have to go into a joint committee session with members of both the Chamber of Deputies and the Senate acting together to enact the measure. This joint committee is expected to begin discussing the bill on the afternoon of Friday, April 23 (today).

In parallel, the government sent on Tuesday, April 20, a petition to the Constitutional Court to declare the bill unconstitutional. The request is grounded on the argument that the legal authority to make modifications to public expenditure plans lies exclusively with the President under the existing constitution.

In response to the petition, some parts of the Opposition (i.e., the Communist Party and members of the Frente Amplio coalition) announced that they will prepare a request for a constitutional censure of Pres. Piñera. This proposal has already received backing from some additional members of the left-wing coalition.

On top of this hectic political terrain, Senator Bianchi, a member of the Opposition, is preparing a motion to impeach Justice María Luisa Brahm, President of the Constitutional Court. The motivation for this petition lies in Brahm’s ties to President Piñera: she was the head of advisers in his first government (2011–14) and she voted to declare unconstitutional the previous withdrawals of pension-fund assets.

All in all, even if Congress approves in the coming days the bill to allow a third withdrawal of pension-fund assets, the final resolution enabling these transfers would take at least a couple weeks to be released. The government and members of the Opposition are preparing the arguments that they plan to present to the Constitutional Court. Once the petition is registered, the Constitutional Court would take up to 10 days to examine its admissibility and then five more days are provided for the parties involved to make their arguments. Hence, it is expected that the Constitutional Court will release its verdict just days before the elections of May 15–16.

It has been estimated by the pension-funds regulator that a third round of withdrawals would lead to divestitures of USD 19 bn. Such moves would have noticeable implications for the exchange rate, interest rates, and private consumption.

—Jorge Selaive & Carlos Muñoz

COLOMBIA: S&P AFFIRMED COLOMBIA’S CREDIT RATING AT BBB- OWING TO COMMITMENT TO FISCAL SUSTAINABILITY, BUT KEPT OUTLOOK NEGATIVE

On Thursday, April 22, the international rating agency S&P decided to keep its ratings and outlook on Colombian debt at BBB-/A-3 (negative outlook), one notch above the investment grade threshold. The move came as a surprise since we did not expect any agency to publish a view on Colombia so early in the year. As a result, S&P’s move should be taken as positive news for markets, where expectations were tilted to the downside owing to the possibility of a watered-down tax reform package that wouldn’t be enough to ensure long-run fiscal sustainability.

S&P highlighted Colombia’s renewed commitment to fiscal sustainability, as demonstrated by the government’s presentation of its tax-reform proposals to Congress. However, S&P’s maintenance of its negative outlook reflected the ongoing risk of further deterioration in Colombia’s fiscal accounts. A negative scenario that could trigger a downgrade would feature lower growth, a further weakening in public finances, and an increase in public-debt burdens. On the other hand, S&P’s outlook could be revised to stable if the government were to stabilize the economy and rebuild fiscal buffers, improve its debt profile, and reduce external risks.

As in previous ratings decisions, S&P’s report underscored Colombia’s traditions of stable democracy and strong public institutions, predictable economic policies, and orthodox macroeconomic management, as particularly reflected in the flexible exchange-rate regime and independent central bank. These assets will remain key considerations in any future ratings-agency assessment.

For additional context, recent communications from Fitch (which also pegs Colombia at BBB- with a negative outlook) indicated that it would wait until after the pandemic passes before updating its view on any countries with a negative outlook. At the outset of the COVID-19 crisis, S&P cut Colombia’s outlook from stable to negative, while Fitch downgraded Colombia to BBB- and kept its outlook at negative (table 1).

Colombia should retain its investment-grade status for now, with any future credit-ratings action contingent on the success of the fiscal reforms currently under discussion in Congress and the country’s ongoing economic recovery. We expect real GDP growth to meet or exceed the credit-rating agencies’ expectations, which should add support to Colombia’s investment-grade status.

—Sergio Olarte & Jackeline Piraján

MEXICO: HEADLINE INFLATION SPIKED ABOVE CONSENSUS IN THE FIRST HALF OF APRIL

According to data released by INEGI on Thursday, April 22, headline inflation in the first half of April came in above market consensus at 6.05% y/y (versus 5.22% y/y in late-March and the 5.9% y/y consensus), well above the 4% y/y upper bound of Banxico’s target range (chart 1). Sequential inflation came in at 0.06% 2w/2w compared with the -0.13% 2w/2w average expected in the Citibanamex Survey. Since 2010, inflation for this fortnight has tended to be negative, but upward price pressures in its major subcomponents caused this fortnight to be an outlier.

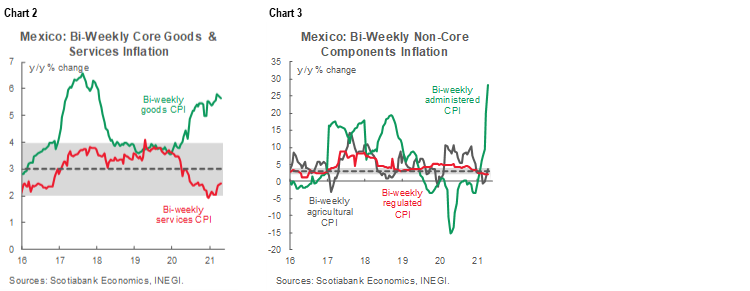

Looking further into the details, core prices advanced 0.18% 2w/2w, above the 0.16% 2w/2w average expected, but below the 0.20% 2w/2w previously registered in late-March. Core inflation continues to show distinct rates of advance amongst its major subcomponents. Merchandise prices accelerated 0.29% 2w/2w from late-March’s 0.18% 2w/2w, while growth in the prices of services moderated from 0.23% 2w/2w to 0.06% 2w/2w following the end of the holiday period.

On the other hand, the non-core component fell -0.28% 2w/2w from 0.51% 2w/2w in late-March, which compares with a variation of -5.78% 2w/2w in the same fortnight in 2020. The energy-prices subcomponent went from 0.61% 2w/2w in late-March to -2.31% 2w/2w, driven by lower domestic gas prices; on the food side, prices advanced in the fortnight from 0.61% 2w/2w to 1.60% 2w/2w.

The 6.05% y/y variation in headline inflation was the highest since the second half of December 2017 (6.85% y/y). We are concerned that this spike could be more stubborn than previously expected given that combined core and non-core foodstuffs have a roughly 25% weight in total CPI, and ongoing droughts pose an additional risk of upward price pressures. Even with analysts expecting a rise in prices during this fortnight, the annual change was materially above the 5.9% y/y expected by consensus. Banxico will have to be cautious to avoid second-order effects.

By components, core inflation advanced 4.13% y/y in early-April (chart 1, again). Merchandise prices rose 5.66% y/y from a previous rate of 5.78% y/y (chart 2). Merchandise prices have been cooling for two consecutive fortnights, but are still growing at higher rates than observed prior to the pandemic. Services prices accelerated for a third consecutive fortnight, from 2.39% y/y to 2.47% y/y. Finally, the non-core component jumped from 8.52% y/y to 12.21% y/y (chart 1, again), its highest rate since the second half of December 2017 (13.04% y/y), driven mainly by the 28.22% y/y rise registered in the administered energy prices (chart 3).

Overall, this latest inflation print poses yet another risk to our call for a final -25 bps cut to Banxico’s policy rate during Q3-2021.

—Miguel Saldaña

PERU: GOVERNMENT GIVES GREEN LIGHT TO WITHDRAWALS FROM WORKER FUNDS

The Head of the Cabinet (i.e., Prime Minister), Violeta Bermúdez, announced on Wednesday, April 21, that the government would not veto the law issued by Congress allowing for complete withdrawal of worker compensation funds (Compensación por Tiempo de Servicios, CTS). CTS funds consist of accounts that are made available to formal workers who lose their jobs. The setup has been created in lieu of government unemployment cheques or insurance. Currently, CTS funds amount to PEN 21.7 bn (USD 5.9 bn) or 2.9% of GDP. Since assets in these accounts generally accrue interest at a rate that is higher than that applied to other personal savings accounts, it is not clear how much of these funds will actually be withdrawn, especially considering that account holders are, by definition, people who have formal jobs. At the same time, however, family needs, and perhaps the political situation, may motivate workers to pull out some of the monies in these accounts. Withdrawals will be permitted once the government provides guidelines (there is a 10-day deadline) and will be allowed until December 31. Bermúdez conceded that allowing such withdrawals carried the risk of leaving workers unprotected if they lose their jobs, but she argued that the current emergency warrants special measures. Bermúdez also indicated that the government had yet to make a decision on the Congressional initiative that would allow for a third withdrawal from private pension funds. The CTS withdrawals would add to the 2.5% of GDP worth of fund payouts and government benefits awarded in 2021 that have been helping to bolster consumption. The government could conceivably make the same argument that an emergency merits allowing Peruvians to draw again on their pension funds, but there is more at stake with the CTS draw-downs as the private pension fund system itself is the subject of political debate.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.