Central banks & macro data: September lull in risk events

Argentina: Still in the woods

Colombia: BanRep delivered a -25 bps cut in a split decision; IMF increased the flexible credit line by 60%

Mexico: July IGAE rose 5.7% m/m, but remained down -9.8% y/y

Peru: More unlocking in Peru; business loans continued surging in August

CENTRAL BANKS & MACRO DATA: SEPTEMBER LULL IN RISK EVENTS

The week ahead is expected to be relatively quiet for the Latam-6’s central banks, with the 14:00 ET release today by Colombia’s BanRep of the minutes from its Friday, September 25, monetary policy meeting the only major event scheduled for the week. We will look to the minutes for additional colour on the views of the three Board members that voted to keep the monetary policy rate on hold at 2.00% rather than opt for the -25 bps cut to 1.75% favoured by the Board’s four-member majority. It’s not clear whether the minority wished to see an end to the easing cycle or additional cuts at a more gradual pace.

There are also only a few major tier-1 macro data prints this week:

- Argentina. The July monthly GDP proxy comes out today, the last of the Latam-6’s economic activity prints for July. Consensus expects a mild improvement from -12.3% y/y in June to -11.5% y/y in July. We are a tad more optimistic with a -9.7% y/y forecast.

- Brazil. August’s primary budget deficit, due to be released on Wednesday, is expected by consensus to widen from BRL -81 bn in July to BRL -97.7 bn.

- Chile. Thursday should see the release of the August economic activity index, and consensus expects an improvement from -10.7% y/y in July to -8.4% y/y. Our own forecast is for an -8.0% y/y reading.

- Mexico. PMIs for September are set to arrive on Thursday, with the leading indicator indices on Friday.

- Peru. Lima leads the Latam-6 in the release of September price data with headline inflation numbers out on Thursday. Consensus expects Lima CPI to hold at 1.7% y/y from August (chart 1), but our team forecasts a slowing to 1.5% y/y on the back of a -0.2% m/m pullback. We still expect inflation to end the year at 1.1% y/y, however—well above the 0.8% y/y anticipated by the BCRP.

—Brett House

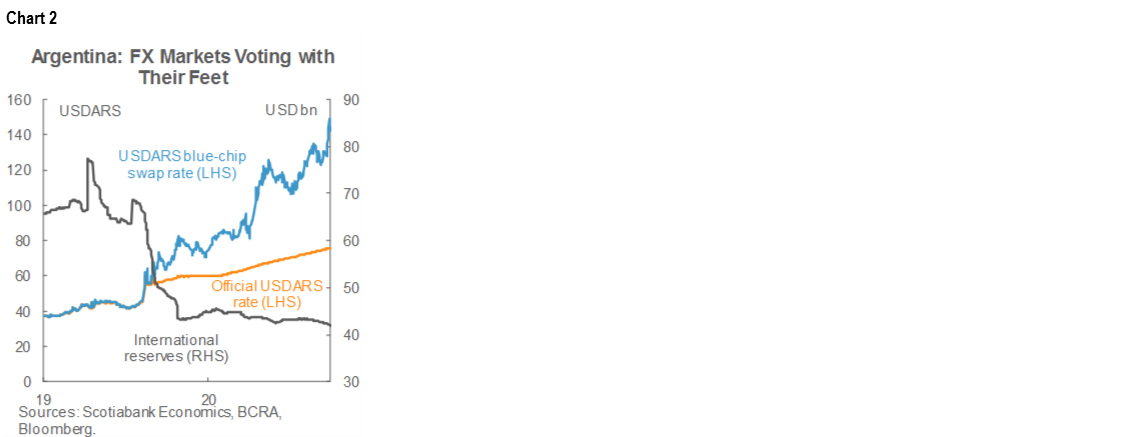

ARGENTINA: STILL IN THE WOODS

The halo generated by the recent restructuring of USD 65 bn in foreign-law bonds that were in default is fading quickly and Argentina’s balance of payments remains under pressure. FX reserves continue to edge down, with an estimated 90% of the existing USD 42 bn holdings (chart 2) thought to be committed to pre-existing obligations. Last week, the blue-chip swap rate surged at one point to a record USDARS 149.31 after the authorities tightened FX controls and USD deposits continued to drain out of the financial system. Near-term hopes are pinned on a rapid agreement to roll over Argentina’s outstanding debt to the IMF, which would extend the grace period on its obligations by over three years. But an understanding on a new lending program will almost certainly feature some combination of a gradual liberalization of FX controls, ARS devaluation, and higher interest rates.

—Brett House

COLOMBIA: BANREP DELIVERS A -25 BPS CUT IN A SPLIT DECISION; IMF INCREASED THE FLEXIBLE CREDIT LINE BY 60%

On Friday, September 25, BanRep cut the monetary policy rate (MPR) by -25 bps to 1.75% (chart 3) in a divided decision: four members voted for the cut, while three voted for a hold. The communiqué emphasized that both inflation and inflation expectations are at low levels, while the economy remains weak. The Board observed that the labour market remains a concern and that household disposable incomes have fallen significantly, which probably was the main reason that the Board voted to continue the easing cycle.

The central bank also announced that the FX NDF program will be renewed in October. The size of the outstanding program is about USD 328 mn and three expiration dates remain: October 5, 9, and 13.

Additionally, the BanRep noted that the IMF had approved a request from the Colombian authorities to increase the country’s Flexible Credit Line (FCL) from USD 10.8 bn to USD 17.2 bn, a 60% increase. The BanRep statement explained that the government is considering using USD 5.7 bn of the FCL for pandemic-related budget support that, in principle, would replace other possible (and more expensive) external financing sources, in line with the current fiscal deficit target of -8.2% of GDP for 2020.

Regarding monetary policy, Governor Echavarria said that the central bank is running out of space to continue cutting the MPR and that the easing cycle is almost done. Although the BanRep remains data dependent, this is a clear signal that the probability of a pause is high at the next meeting.

All in all, Friday’s split decision marked a clear shift from the BanRep that points to a hold at the October meeting. We maintain our baseline forecast of stability in the MPR at 1.75% for the rest of 2020, with a first hike in H2-2021. The authorities’ plan to monetize further indebtedness should prompt new USD inflows.

—Sergio Olarte & Jackeline Piraján

MEXICO: JULY IGAE ROSE 5.7% M/M, BUT REMAINED DOWN -9.8% Y/Y

According to figures released by INEGI on Friday, September 25, growth in the Global Indicator of Economic Activity (IGAE in Spanish) slowed from 8.95% m/m in June to 5.69% m/m in July even after further progress in Mexico’s gradual re-opening. In annual terms, the decline in real GDP softened from -13.18% y/y in June to -9.84% in July, almost in line with market expectations of -10.10% y/y. This marked a seventh straight month in which the monthly GDP proxy has been down from a year earlier. Declines in industry and services dominated the comparisons with a year ago. For the first seven months of the year, the IGAE was down an average of -9.9% y/y, the worst decline for the January–July period in recent history (chart 4).

Despite July’s month-on-month gains, we expect Mexican real economic activity to remain below levels from a year ago through the end of 2020, as noted in the most recent Latam Weekly from September 20. We forecast a contraction in real GDP of -10.6% y/y in Q3-2020 and -5.6% y/y in Q4-2020. Overall, 2020 remains on track to record a decline of -9.1% y/y, followed by a mild rebound of 3.0% y/y in 2021.

—Paulina Villanueva

PERU: MORE UNLOCKING IN PERU; BUSINESS LOANS CONTINUED SURGING IN AUGUST

President Vizcarra announced more re-opening measures during a press confidence on Friday, September 25. Pres. Vizcarra stated that Phase 4 of the re-opening would begin in October, but was expected to be implemented gradually. This was largely expected, and there was little that was surprising in the details of the announcement:

- The focused lockdown in Cusco, Puno, Moquegua, and Tacna was lifted.

- International flights would begin on October 5, although to a limited number of destinations. Tourism and everything having to do with flights and tourism will be able to resume operations.

- Artistic activities, non-contact sports, and most family entertainment can re-open at 50% capacity.

- Restaurant and mall capacity have been raised from 40% to 50% and 60%, respectively.

- Bars, dance halls, cinemas, and schools are to remain closed.

Note that Phase 4 only represents 5% to 6% of the economy.

Total bank loans were up 15.0%, y/y in August, according to data released by Asbanc, on par with growth in July (chart 5). The strong performance largely reflected the BCRP’s liquidity programs, especially the PEN 60 bn REACTIVA program, which is channeled through banks to businesses. As a result, total business loans were up 23.7% y/y, led by small business loans, which rose an impressive 49.5% y/y. These programs have been key in maintaining payment chains during the lockdown and its aftermath. Meanwhile, household loans were basically flat, with 0.2% y/y growth (chart 5, again). Unlike business loans, household loans are more in line with the decline in demand and employment. The one hopeful sign on the household front is that mortgage loans outstanding rose m/m in August for the first time since March.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.