Latam Economic Update

Argentina: Extended lockdowns slowing the recovery

Brazil: IPCA pushed up by food prices and rebounding activity, but BCB has signaled it’s likely to look through it

Colombia: Re-opening announcements and recovery indicators

Mexico: Recovery in commercial activity cooled in July

Peru: Home sales in August surpassed pre-COVID-19 levels for a second month

ARGENTINA: EXTENDED LOCKDOWNS SLOWING THE RECOVERY

Retail sales for July, released by INDEC later on Wednesday, September 23, continued to paint a picture of two distinct sub-sectors. While supermarket sales were more or less flat, turning from a -1.5% y/y decline in June to 1.0% y/y growth in July, shopping centres, which largely remain closed, still saw sales off -83.3% y/y, basically unchanged from June’s -88.6% y/y (chart 1). With quarantine measures extended in greater BsAs through mid-October, the retail sales data underscore that further recovery in economic activity is going to be a slow grind from here.

In a stale print on Wednesday, September 23, Argentina’s Q2 unemployment rate came in at 13.1%, up from 10.4% in Q1 (chart 2). Although no consensus forecast was available for this data point, the last unemployment release for Q2 amongst the Latam-6, the outturn was just above our forecast of 12.1% and within the margin of error on Argentina’s official statistics. Every country saw a spike in unemployment rates in Q2, so the rise in Argentina is broadly in line with expectations. What is different in Argentina’s case is that the spike continues a trend of increasing unemployment rates through three years of recession that will likely prove more difficult to roll back post-pandemic than in other countries. Still, there was one bright spot in the numbers: the rate of underemployment came down from 11.7% in Q1 to 9.6% in Q2.

—Brett House

BRAZIL: IPCA PUSHED UP BY FOOD PRICES AND REBOUNDING ACTIVITY, BUT BCB HAS SIGNALED IT’S LIKELY TO LOOK THROUGH IT

The IBGE released on Wednesday, September 23, IPCA inflation data for the first half of September, which printed at 2.65% y/y, close to consensus of 2.60% y/y, but above our house call for 2.50% y/y (chart 3). We underestimated the pressures on food prices (which surged to 9.93% y/y), but we don’t see this print as a “view changer” or even particularly meaningful: the spike was already flagged by the BCB in the statement that followed its September 16 Selic decision and in the minutes from that meeting that were released on Tuesday, September 22. The Copom signalled that it anticipated this rise in inflation and saw it as temporary; in fact, the BCB introduced further stimulus through forward guidance in the minutes despite having foreseen the food price spike in the IPCA data.

In addition, on Wednesday, September 23, we received Brazil’s August current account data, which surprisingly showed an increase in the monthly surplus from USD 1.6 bn to USD 3.7 bn (versus consensus of USD 2.3 bn). We had anticipated that the surplus would begin narrowing on the back of the relatively strong recovery in Brazilian demand compared with other large EMs and trade partners.

—Eduardo Suárez

COLOMBIA: RE-OPENING ANNOUNCEMENTS AND RECOVERY INDICATORS

Since September 1, Colombia has been operating under a new approach to the pandemic, having abandoned a mandatory general quarantine in favour of a selective isolation policy. With this move, the Colombian government now allows around 95% of the economy to operate as usual; having said this, in the capital city, Bogota, some additional restrictions remain in place which are dampening the speed of the expected economic rebound.

On Monday, September 21, however, Bogota's Mayor, Claudia Lopez, eased some restrictions. A scheme under which some businesses and activities were restricted to specific days was withdrawn. Additionally, citizens can now access different services without limitation; previously, these activities were limited by individual ID numbers, a scheme called “pico y cédula”. Businesses are still required to follow biosecurity protocols and social distancing, but gyms and churches have been allowed to resume their activities. The only activities that continue to face comprehensive restrictions are night clubs, concerts, and large indoor events.

The Bogota mayor’s announcement represents the biggest liberalization in the city since the re-opening started. The decision to reduce restrictions was taken after occupied capacity in hospital ICUs fell to 55% and contagion numbers began to show some improvement. Bogotá accounts for 26% of Colombia's GDP and 16% of the industrial sector. Thus, any easing of restrictions in the capital region has massive implications for the entire Colombian economy.

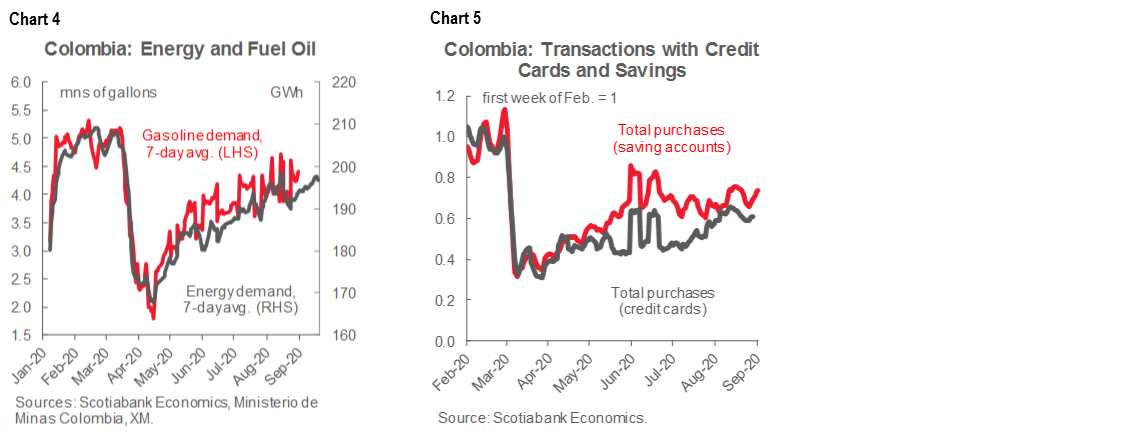

As some early economic indicators have implied, the economic recovery in July and probably also in August stagnated as Colombia’s main cities restricted activities more than in other regions. However, leading indicators such as energy demand (chart 4) are pointing upward again. Still, the real challenge remains household demand since employment remains down by -20% and sentiment remains soft. According to Scotiabank Colpatria data, clients' transactions with credit and debit cards started September with moderate increases, but remain below pre-pandemic levels: debit card transactions are still down -20% from pre-COVID-19 numbers, while credit-card flows are off -40% (chart 5).

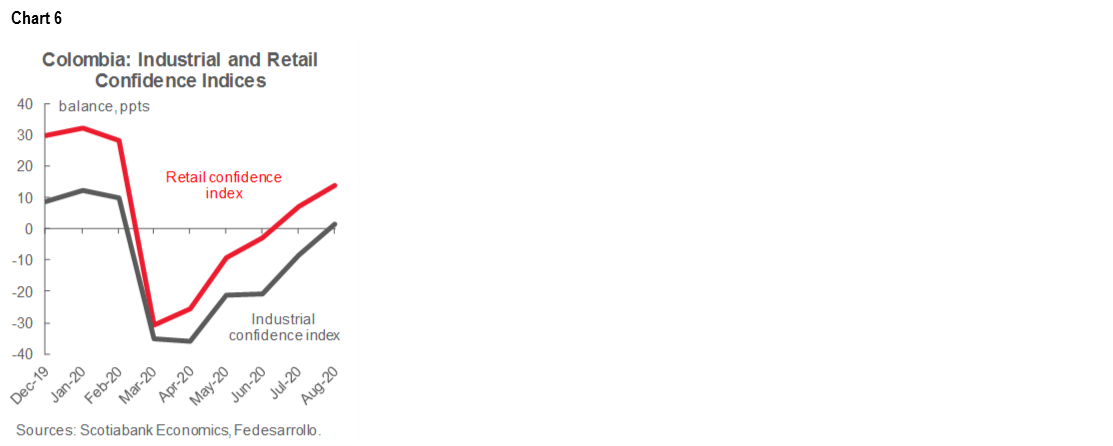

Green shoots are, nevertheless, appearing in businesses confidence surveys: according to Fedesarrollo's August readings, out on Wednesday, September 23, indices of both retail and industrial sentiment improved and are now in positive territory. The gains were driven by better expectations about the economic situation and rosier assessments of the current situation (chart 6). Complementing these developments, employment will likely continue to recovery gradually as better business perspectives consolidate.

For now, we are not changing our GDP forecast from -7.5% y/y for 2020 and 5.0% y/y in 2021, as noted in our September 20 Latam Weekly. We think the current re-opening stage should come together and lead to better numbers in the coming months. Still, ahead of the Friday, September 25 BanRep monetary policy meeting, we continue to anticipate a further (and probably the last) -25 bps rate cut in the headline rate to 1.75%.

—Sergio Olarte & Jackeline Piraján

MEXICO: RECOVERY IN COMMERCIAL ACTIVITY COOLED IN JULY

Retail and wholesale activity continued to improve in July, but at a modest pace, according to data released on Wednesday, September 23 (chart 7). Both sets of numbers improved slightly, but remained well below pre-pandemic levels.

In sequential monthly terms, retail sales growth moderated from 7.8% m/m in June to 5.5% m/m in July, and wholesale sales also softened from 11.1% m/m to 4.5% m/m.

In real annual terms, retail and wholesale sales in the second month of re-opened businesses improved, but remained well below last year’s numbers. Retail sales were down -16.6% y/y in June and improved to -12.5% y/y in July, below market consensus of -12.0% y/y. Simultaneously, wholesale sales came up from -12.8% y/y in June to -10.7% y/y in July.

July’s moderation in the commercial rebound was somewhat anticipated by other previously released indicators for the same period. However, considering the depth of the unprecedented drop in April and May, a broader recovery was always expected to take time, especially because we maintain a weak outlook for the labour market and for domestic consumption through the rest of the year.

—Miguel Saldaña

PERU: HOME SALES IN AUGUST SURPASSED PRE-COVID-19 LEVELS FOR A SECOND MONTH

According to data released Wednesday, September 23, by the private-sector’s Association of Real Estate Companies (Asociación de Empresas Inmobiliarias—ASEI), home sales in Lima were up a rather astonishing 10% y/y in August (chart 8). These results came after an even stronger month in July. The ASEI data are not reviewed by official sources, but they are reliable indicators of trends for the sector. Note, however, that although the V-shape recovery in home sales is real, the strength of the rebound likely also reflects demand that was pent up from the March–May lockdown period. This would explain why sales were lower in August than in July, and would suggest that year-on-year home sales growth could continue moderating in the coming months.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.