Latam Economic Update

Argentina: FX controls tighten from today

Brazil: Preview of today’s BCB Copom decision

Peru: July GDP and August employment continued improving slowly, politics remain unsettled

ARGENTINA: FX CONTROLS TIGHTEN FROM TODAY

In a move that dashes some hopes of a shift to more orthodox policy-making following the conclusion of the external debt restructuring and the initiation of talks with the IMF, BCRA President Miguel Pesce indicated on the evening of Tuesday, September 15, that from today, Wednesday, September 16, new FX controls would be imposed. These include the following efforts to encourage use of the ARS:

- The so-called “solidarity tax” on retail USD purchases would be raised from 30% to 35%, with the limit on USD purchases maintained at USD 200 each month;

- The tax on USD credit card purchases would also be set at 35% on balances from September 15;

- Elimination of the holding period on FX-denominated assets if they are settled in local currency, while at the same time raising the holding period for FX assets not settled in ARS to 15 days; and

- Companies with over USD 1 mn / month in debt maturing would have to present a plan for their coming FX transactions.

Pres. Pesce confirmed that these moves have not been discussed with the IMF, and could prove to be a sticking point in negotiations.

On the other hand, Tuesday also saw the submission to Congress of the Fernandez Administration’s first annual budget bill, which was built on a somewhat ambitious growth projection for 2021, but showed some moves toward fiscal adjustment. Where the government now forecasts 5.5% y/y real GDP growth in 2021, we forecast a more modest 4.7% y/y rebound. Annual inflation is expected to come in at 29% y/y, in line with our forecast of 27.2% at end-2020. The deficit for 2021 is pegged at -4.5% of GDP, compared with consensus expectations of -8.1% in 2020 and -5.0% in 2021.

—Brett House

BRAZIL: PREVIEW OF TODAY’S BCB COPOM DECISION

The BCB’s Copom is scheduled to announce its monetary policy decision today at 17:00 ET, with economists surveyed by Bloomberg expecting a hold, marking the end of the easing cycle. October DIs are pricing in marginal odds of a final cut. Our house view is that the BCB will cut one final time (from 2.00% to 1.75%, chart 1), but we acknowledge that there are important risks that the cycle is over. In our view, the key points affecting the decision are:

- The BCB left the door open for a small final cut, by saying that any additional easing would be marginal. But this didn’t clarify whether the cycle is over or not.

- The BCB’s inflation target is 3.25% +/- 100 bps, while IPCA inflation currently sits at 2.44% y/y. More importantly, in the latest BCB Focus Survey, consensus views on end-2020 inflation sit at 1.94% y/y, end-2021 inflation at 3.01% y/y, and end-2022 inflation at 3.50% y/y, which means that for the BCB’s policy horizon, expectations are anchored.

- Growth has recovered much more strongly than was anticipated earlier in the pandemic, with some recent indicators implying that a few sectors are now back in positive territory on a year-over-year basis, such as manufacturing PMIs and retail sales. However, capacity under-utilization is still substantial and growth remains in negative territory.

- There is uncertainty over coming fiscal adjustments and the country’s fiscal stance remains on very shaky ground, which seems to be the Copom’s main concern.

- The BCB’s Copom has highlighted financial stability risks as the main factor limiting their capacity to ease rates, and the BRL remains the worst performing among Bloomberg’s 32 Expanded Major currencies, down -24% YTD. Brazil has a history of FX-inflation pass-through—even if it hasn’t been evident in the past couple of years.

Overall, we think there are arguments on both sides—to end the easing cycle today or to deliver a little more stimulus. A final -25 bps of easing wouldn’t do much for the economy either way, and it would be more a question of signaling: the BCB’s Copom faces a decision between sending a sign of prudence in a time of market turmoil or showing a bias toward supporting growth during a hard economic shock in which inflation expectations are still well anchored.

—Eduardo Suárez

PERU: JULY GDP AND AUGUST EMPLOYMENT CONTINUED IMPROVING SLOWLY, POLITICS REMAIN UNSETTLED

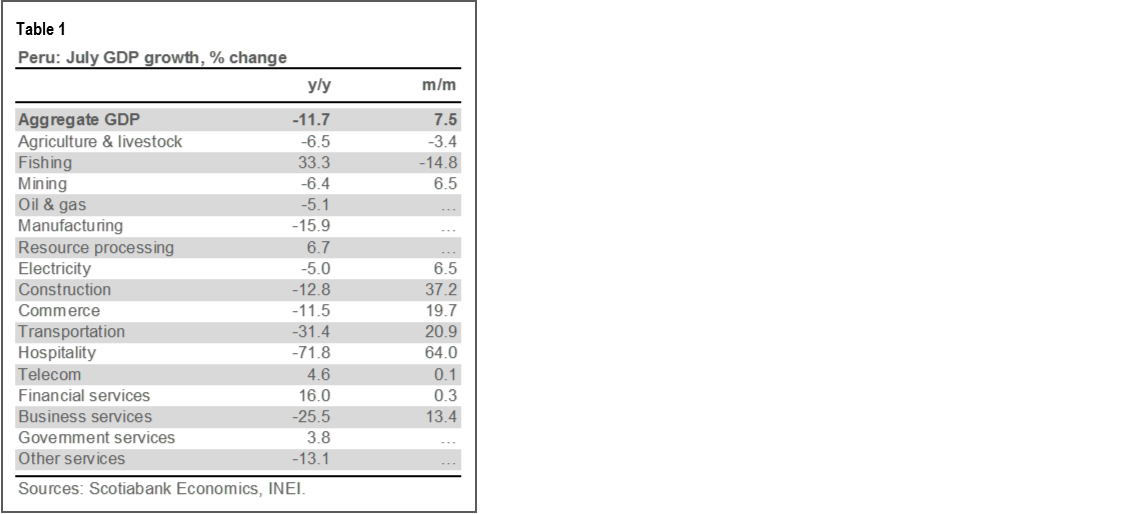

GDP in July fell -11.7% y/y, and rose 7.5% m/m (table 1), according to data released Tuesday, September 15, by the National Statistics Institute, INEI. The y/y decline was a tad higher than the -11% y/y we had been forecasting. The figure compares with an -18.1% y/y decline in June and -32% y/y in May. The 7.5% m/m growth figures also reflected an economy that is emerging from lockdown more or less as expected.

Most of the breakdown was in line with expectations. The one significant surprise was agriculture, which fell a huge -9.5% y/y (-6.5% y/y when coupled with livestock). Due to weather factors and shifts in production cycles, agriculture growth can be volatile, but not normally so strongly. The authorities attribute the decline namely to poor weather (a combination of semi-drought and high temperatures) affecting a broad range of crops.

Outside of the usual suspects, namely, resource sectors and essential goods and services, most sectors continued declining in y/y terms, but also showed mostly healthy rebounds in m/m terms. The bottom line, however, is that, while the recovery of the economy is on course, demand in July was still quite a bit off from pre-COVID-19 levels.

New information on employment in Lima was also released by the INEI on Tuesday. Unemployment in Lima came in at 15.6% for the June–August period (chart 2). This was an improvement over 16.4% during the May–July period, and in line with our forecast of 14% at year-end 2020. This was the first report of a decline in the unemployment rate since the COVID-19-related lockdown began in March. At that time, the unemployment rate stood at 7.8%.

Approximately 1.3 mn people had lost their jobs in June–August, compared to the same period in 2019. However, this represents a gain of nearly 680,000 jobs since May–July, and over 1.4 mn jobs from April–June, which was the nadir of the downturn due to the lockdown of the economy. In short, over half of the jobs lost in Lima due to the lockdown had been recovered by August.

The political scenario continues unsettled. On Monday, President Vizcarra ratified accusations of a conspiracy by members of Congress, led by Manuel Merino, who presides over Congress as its President, a role akin to Speaker in other countries. Pres. Vizcarra revealed that, in addition to knocking on the doors of the military, Merino had been putting together a “pseudo-cabinet”. Pres. Vizcarra was apparently referring to talk that a prominent member of Acción Popular, the party that Merino belongs to, had been approached and offered a cabinet position in the new Merino government. Meanwhile, the government formally requested the Constitutional Court to halt any Congressional proceedings to remove Pres. Vizcarra. As a reflection of public opinion, a poll conducted by Ipsos on September 12 was released on Tuesday, showing that Pres. Vizcarra’s approval rate was still fairly high at 57%, although it had declined from 60% in August. Meanwhile the approval rate of Manuel Merino dove from an already low 35% in August, to only 19% currently.

Meanwhile, Congress voted against a motion for the removal (“censure”) of Finance Minister Alva. The vote was 46 in favour and 73 against. The motion needed 66 votes to pass. It is likely that the events surrounding the attempt to remove Vizcarra from office may have weakened the resolve of Congress concerning the removal of Minister Alva as well.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.