Argentina: Inflation ticks up, worrying signs in the details; BCRA cuts benchmark policy rate

Peru: September tax revenue continued under-performing; new initiative for AFP withdrawals

ARGENTINA: INFLATION TICKS UP, WORRYING SIGNS IN THE DETAILS; BCRA CUTS BENCHMARK POLICY RATE

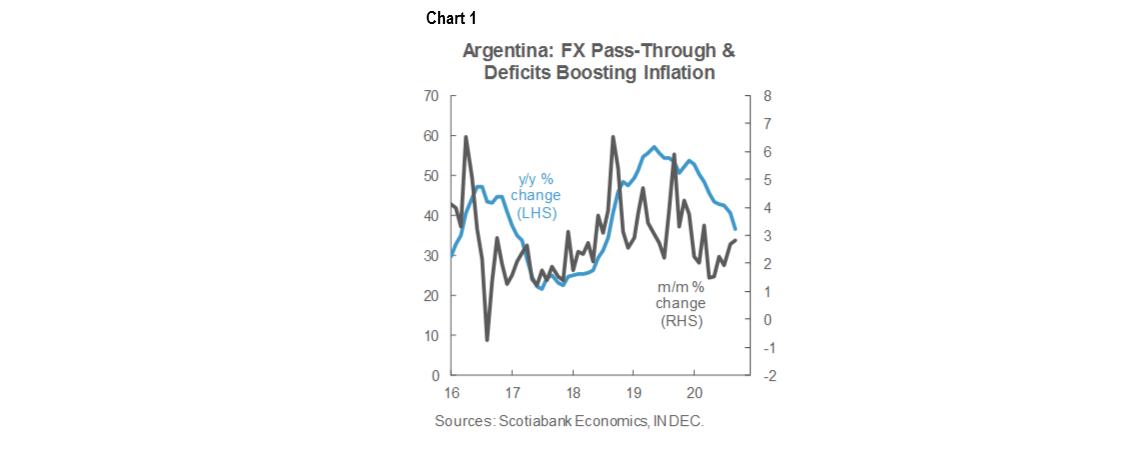

In price data released by INDEC on the afternoon of Wednesday, October 14, the national CPI basket rose 2.8% m/m in September, up from 2.7% m/m in August (chart 1). The monthly inflation print was in line with expectations, though still artificially dampened by price controls on utilities and public transportation, and official “price monitoring” on thousands of other items. Base effects from 2019 meant that annual inflation came down from 40.70% y/y in August to 36.6% y/y in September (chart 1, again).

Details in the monthly inflation print pointed to gathering inflation momentum, reflecting the ongoing slide in the ARS, some supply constraints, and continued extensive deficit monetization and expansion in the monetary base by the BCRA. Core inflation picked up from 2.3% m/m in August to 3.0% m/m in September, though base effects still pulled down the annual core number from 43.9% y/y to 38.3% y/y. Clothing prices, up 5.8% m/m in September, recorded the largest price gains of any sector in the month, which likely reflects pass-through from the weakening ARS.

While we expect monthly inflation to remain between 2% m/m and 3% m/m through end-2020 and persist around 3% m/m in 2021, base effects should continue to pull down the headline rate below 30% y/y by the end of the year before rising back above 40% y/y by end-2021. Aside from price controls, which are not sustainable, there is little in the Argentine policy mix that would augur for any slowdown in price increases.

Despite Argentina’s ongoing struggle with inflation, the BCRA took a further step on Wednesday in the re-alignment of its interest-rate complex with a cut in the benchmark Leliq policy rate from 38% to 37%. We had expected a temporary cut of this sort in Q2/Q3 to help boost the domestic economy, but we took it out of our forecasts after the BCRA stayed on hold into the beginning of Q3. We still expect this cut to be short lived.

—Brett House

PERU: SEPTEMBER TAX REVENUE CONTINUED UNDER-PERFORMING; NEW INITIATIVE FOR AFP WITHDRAWALS

Tax revenue in September was down -19.9% y/y, according to figures released by the Tax Agency, Sunat, on Monday, October 12. Although this was the mildest annual contraction since March, the first month of the lockdown, it was still a bit of a disappointment, as it represented an only 1.3% m/m increase over August. Tax revenue has been improving significantly since June (when it was down -47% y/y), but these gains seem to have slowed at levels that are still low compared with last year. Note, however, that part of the reason that tax revenue continues to be low is that temporary tax relief measures were still extant in September. Tax relief is particularly linked to income taxes, which were down -21% y/y. Meanwhile, domestic sales tax revenue, which is a better barometer of economic activity, was down a softer -7.3% y/y, and up a robust 8.4% m/m in sequential terms.

Also on Monday, October 12, a Congressional committee voted in favour of a bill that would allow non-working private pension fund (AFP) account holders to withdraw up to PEN 17,200. This would come on top of past withdrawals. As with the previous withdrawal initiative (up to PEN 12,000), only account holders who have been out of work over the past twelve months may access these funds. The committee softened a much harsher earlier version that would have allowed out of work account holders to withdraw the entirety of their retirement account holdings. The more modest bill followed a session with Central Bank President Julio Velarde, who advised them that the more ambitious version would do more damage than good. The bill must still be approved on the main floor of Congress.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.