Argentina: Government tax revenue on the rise in October

Brazil: BCB minutes indicated remaining space for easing small owing to prudential concerns

Colombia: BanRep minutes highlighted signs of recovery and uncertainty as Board remains data dependent

Mexico: Record remittances continue; indicators of asymmetrical recovery; Banxico survey narrows predicted GDP contraction

ARGENTINA: GOVERNMENT TAX REVENUE ON THE RISE IN OCTOBER

Government tax revenue rose again in October, putting it back on its pre-pandemic trend, according to data released on Monday, November 2. Total inflows to public coffers rose from ARS 606.5 bn in September to ARS 642.1 bn in October, which took revenues’ 12-month rolling sum up from ARS 6.07 tn to ARS 6.27 tn (chart 1). October tax revenues were up 43.7% y/y from a year ago, which kept them ahead of the country’s 36.6% y/y headline inflation rate and translated into a 6.4% y/y real increase. Taxes on personal assets and incomes led the gains, with demand-side VAT and trade taxes lagging.

Overall, the print will be encouraging for the Ministry of Economy, which has promised to forego budget transfers from the BCRA (central bank) through the end of 2020. The tax revenue numbers also imply that growth is set to be a bit stronger at the start of Q4 than recent real-economy indicators have suggested.

—Brett House

BRAZIL: BCB MINUTES INDICATED REMAINING SPACE FOR EASING SMALL OWING TO PRUDENTIAL CONCERNS

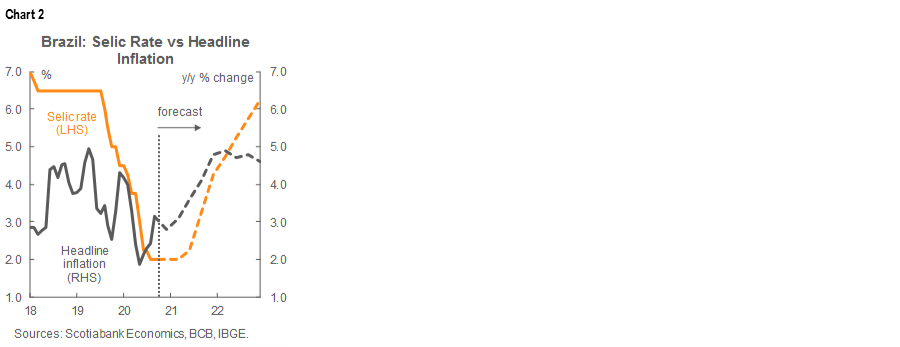

The BCB released at 06:00 on Tuesday, November 3, the minutes from its latest Copom meeting on October 28 at which it unanimously voted to hold the Selic rate at 2.00% (chart 2), a record low; the detailed account of the discussion largely reinforced the major messages conveyed in the Copom’s statement.

For Brazil’s economy, the BCB’s message is consistent with its previous themes: in the Copom’s view, the recovery has been uneven due to differentiated impacts from social distancing across industries, with relatively greater slack in Brazil’s service sectors. It also noted that uncertainty has increased owing to the iffy prospects for fiscal stimulus beyond year-end.

On the inflation front, the Copom highlighted that expectations for the relevant policy horizon are anchored near the lower bound of the BCB’s inflation-targetting range. However, the minutes underscored two-way risks, with the downside driven by economic slack and the potential hit to the economy from a longer pandemic, and the upside by possible fiscal action and improvements in financial stability. But even with two-sided risks, it appears that the Copom sees them tilted negatively: “The Committee concluded that the nature of the crisis probably implies that disinflationary pressures from reduced demand may last longer than in previous recessions.”

In terms of its assessment of the external environment, the message was mixed. On one hand, the minutes highlighted that the strong recovery we had been seeing in some sectors seems to be stalling, while on the other side, they pointed out that the stabilization in global financial markets is positive for emerging markets.

Despite the Copom’s messages on inflation, the it basically shut the door further on additional easing by indicating that, “members discussed the maintenance of signaling that the remaining space for monetary policy stimulus, if it exists, should be small. The Committee assessed that this signaling is due to prudential restrictions regarding reductions of the Selic rate and, therefore, should be kept in communication.” With regards to its forward guidance, the BCB reiterated that it sees large “tails” on both sides of its growth and inflation projections, but that it deemed current policy settings as adequate.

Overall, the minutes were useful in getting a more nuanced view of the Copom’s take on macro risks and policy, and they reduce the odds even further of any additional Selic rate cuts.

—Eduardo Suárez

COLOMBIA: BANREP MINUTES HIGHLIGHTED SIGNS OF RECOVERY AND UNCERTAINTY AS BOARD REMAINS DATA DEPENDENT

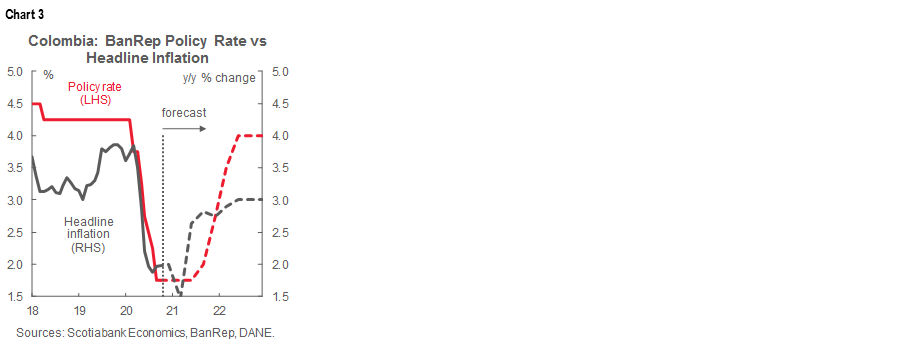

On Tuesday November 3 around 14:00 ET, BanRep published the minutes of its Friday, October 30, monetary policy meeting where it kept its headline policy rate at 1.75% in a unanimous decision (chart 3). The minutes highlighted a relatively favourable scenario, as the Board anticipated a slightly better GDP growth outlook for 2020 than their previously projected range between -6% y/y and -10% y/y (we forecast -7.5% y/y).

The Board emphasized that accelerated re-openings, fiscal support, and the liquidity provided by the central bank should sustain the economic recovery. Additionally, the minutes highlighted that recent external current-account dynamics have led to lower financing needs; nevertheless, the Board saw the augmentation of the IMF FCL as a positive development in the midst of volatile times. On the negative side, the Board indicated that the labour market remained a concern and that the second COVID-19 wave has increased uncertainty around monetary policy.

All in all, the minutes mainly re-affirmed the data-dependent, "wait- and-see approach" of the Board amidst an economic recovery accompanied by huge labour-market challenges and still-substantial pandemic-related volatility. We maintain our call that the monetary policy rate will remain on hold at 1.75% for the rest of the year and into the first half of 2021.

The BanRep also published around 18:00 its latest Monetary Policy Report in which the Bank’s staff provided updated forecasts. We will review their refreshed outlook following today’s press conference and presentation of the Report’s major themes.

—Sergio Olarte & Jackeline Piraján

MEXICO: RECORD REMITTANCES CONTINUE; INDICATORS OF ASYMMETRICAL RECOVERY; BANXICO SURVEY NARROWS PREDICTED GDP CONTRACTION

I. Record remittances continue

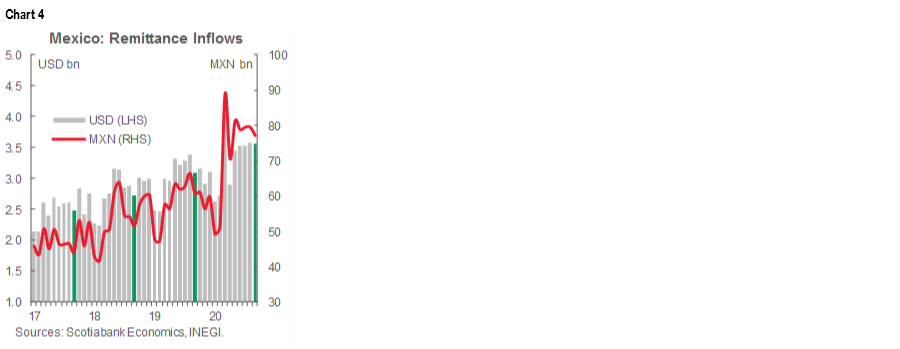

On Tuesday, November 3, INEGI released data on income remittances in September, an important source of foreign-exchange resources that also has a strong impact on consumption. September inflows totaled USD 3.6 bn (up 15.1% y/y), which meant accumulated remittances during January–September amounted to just shy of USD 30 bn (up 10.0% y/y)—record numbers for both the ninth month of the year and the first nine months of the year (chart 4). The continuous and favourable evolution of the flow of remittances reflects the positive generation of employment in the United States.

II. Indicators of asymmetrical recovery

Also on Tuesday November 3, the IMEF released its monthly economic indicator for October and the underlying details highlight an asymmetric recovery. This index seeks to characterize the economic environment based on a survey of five qualitative questions. It is constructed to help anticipate the direction of manufacturing and non-manufacturing activity in Mexico and, from the expected evolution of these sectors, infer the possible direction of the overall economy in the short term.

October’s IMEF figures imply that the rebound in economic activity has been unevenly distributed. Indeed, the manufacturing sector index increased firmly by 3.2 points from September to 50.1 and crossed over into the index’s expansionary zone (> 50). For its part, the non-manufacturing index, which covers trade and services, recorded a drop of

1.1 points from September and moved to 47.7, putting it more deeply into contractionary territory. These results, together with other soft indicators, confirm that Mexico’s recovery in economic activity is being driven mainly by external demand.

III. Banxico survey narrows predicted GDP contraction

According to the Banxico Survey of Expectations for October, released on November 3, private-sector economic analysts have edged back their expectations for 2020’s GDP contraction for a third consecutive time, on this occasion from -9.82% y/y to -9.44% y/y. However, the economic rebound expected in 2021 was also notched down from 3.26% y/y to 3.21% y/y.

Looking at the Survey’s other details:

- Expectations for both headline and core inflation at the end of 2020 increased to 3.92% y/y (previously 3.89% y/y) and 3.92% y/y (previously 3.90% y/y), respectively. For the end of 2021, both headline and core inflation forecasts increased marginally to 3.60% y/y (previously 3.57% y/y) and 3.48% y/y (previously 3.47% y/y). We emphasize that, on the horizon where monetary policy operates, both headline and core inflation expectations remain within Banxico’s target range.

- Exchange-rate projections for the end of 2020 and 2021 strengthened from the September survey and the Mexican currency is expected to end 2020 at USDMXN 21.74 (previously USDMXN 22.14) and USDMXN 22.05 (USDMXN 22.33), respectively.

- As for monetary policy, it’s worth noting that for the fourth quarter of 2020, most analysts anticipate that the interbank funding rate will be below the current target rate (4.25%), although some expect it to be at the same level or above the target.

- Regarding the factors that could hinder Mexico’s economic growth in the next six months, the most-cited issues were related to domestic economic conditions (45%), governance (22%), and external conditions (19%).

—Paulina Villanueva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.