Latam Economic Update

Argentina: June trade data stabilize, but still reflect three years of recession

Peru: In a promising speech, President Vizcarra outlines his government’s plans for his last year in office

ARGENTINA: JUNE TRADE DATA STABILIZE, BUT STILL REFLECT THREE YEARS OF RECESSION

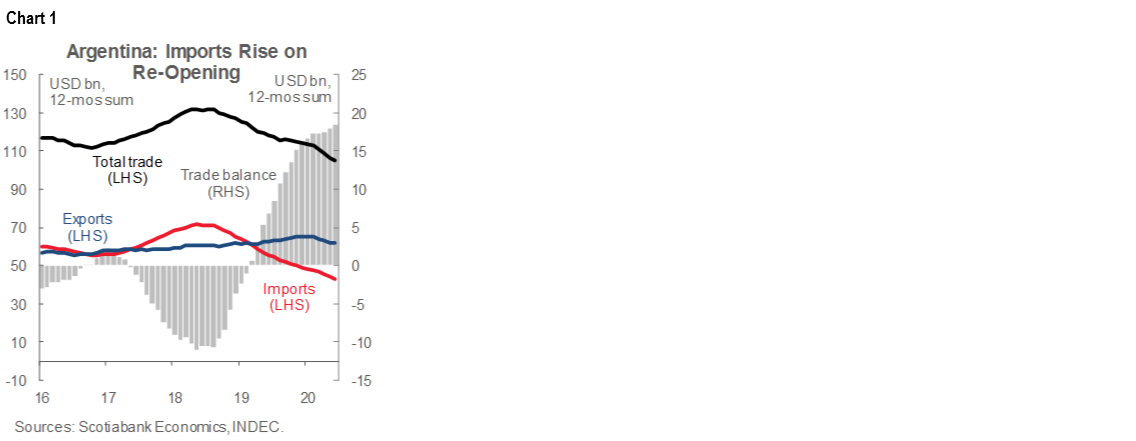

June trade data showed another strong surplus that again reflected weak import demand, but the numbers showed some stabilization from beginning of the global response to COVID-19. The June trade balance came in at USD 1.5 bn, up 39% y/y from the USD 1.1 bn recorded in June 2019; the 12-month rolling balance continued to tick up from USD 18.0 bn in May to USD 18.5 bn in June, a by-product of the collapse in import demand during three years of recession (chart 1). The 12-month rolling sum of the total value of Argentina’s trade flows (i.e., imports and exports combined) continued to fall, but did so in June slightly less quickly than in the last few months.

In the details, June import values were down -21% y/y at USD 3.3 bn (versus USD 3.2 bn in May), with ongoing declines in capital-goods imports (-27% y/y) boding poorly for the economy’s potential over the next few years. At USD 4.8 bn, exports were off by “only” -8.6% y/y as a 46% y/y rise in the value of primary goods exports partially offset declines in manufactured goods (-46% y/y) and energy (-27% y/y).

—Brett House

PERU: IN A PROMISING SPEECH, PRESIDENT VIZCARRA OUTLINES HIS GOVERNMENT’S PLANS FOR HIS LAST YEAR IN OFFICE

President Vizcarra gave his annual Independence Day Address to the Nation on Tuesday, July 28. This is typically an opportunity for the government to outline its agenda for the coming twelve months. In this case, this period will be Pres. Vizcarra’s last year in office. As we expected, Pres. Vizcarra focused his Address on COVID-19 and health issues, on the government’s strategy for economic recovery, and on his search for a new relationship with the political opposition in Congress.

On this last point, Vizcarra actually went beyond relations with Congress, and offered a five-point plan, Pacto Perú, that would encompass work with all political parties. The five points of the Pact include:

1. Building a unified health system;

2. Providing quality education for all;

3. Promoting sustainable economic growth;

4. Reforming the political and judicial system; and

5. Fighting poverty.

Pres. Vizcarra stated that he proposes to invite representatives from all political parties to craft agreements on each of these five points. It’s interesting that Pres. Vizcarra would prefer a discussion with the political parties, rather than with Congress per se. This probably reflects two observations: (1) political parties can be seen as more representative than members of Congress; and (2) members of Congress are more likely to have a personal agenda and the individual relationships that many of them have with the government are difficult. The next step is to see how the political parties respond and what venue is constructed for talks.

Some of Pres. Vizcarra’s most interesting announcements concerned the economy. What could turn out to be the most significant was the announcement of an expansion of the use of government-to-government project management for the operation of infrastructure projects (PMO). This format was used successfully to build the infrastructure for the 2019 Pan-American Games. Recently, a similar format was tendered for the reconstruction of damaged (post-Niño) infrastructure in northern Perú. Pres. Vizcarra announced that the government would apply the PMO format to the following projects:

1. Line 3 and Line 4 of the Lima Metro project. This is a PEN 30 bn (USD 9 bn) investment;

2. The improvement of the Central Highway that is the lifeline that feeds Lima; and

3. Packages of schools, of hospitals and of water projects, for a total of PEN 11 bn.

A number of other economic measures were announced, mainly enhancements to safety nets and fiscal stimulus efforts, including:

A new PEN 760 relief payment to be delivered to 8.5 mn households, for a total cost of PEN 6.4 bn;

Children orphaned due to COVID-19 will receive PEN 200 per month until they are 18 years old;

PEN 736 mn was earmarked for government purchases of small business goods;

PEN 532 mn in housing subsidies was committed; and

PEN 20 bn was budgeted in 2021 for improvements in health and infrastructure.

In addition, Pres. Vizcarra announced that the third stage of the Chavimochic irrigation project had been freed of its legal issues and was one of 2,000 projects, for a total of PEN 328 mn, where issues have been resolved and are ready to proceed.

All in all, the economic part of the Address gave the impression that the government has been working to get prepared to spend heavily over the next 12 months. The most interesting announcement, given precedents, is the greater use of PMOs, although the implementation of this format may still take some time.

The final point in the Address concerned health and COVID-19. The PEN 20 bn announcement for 2021 is a record budget for the health sector, and comes after an already high PEN 10 bn allocation in 2020. The spending plan goes beyond COVID-19. Hospital and ICU units are being expanded and the public health insurance system (Seguro Integral de Salud) is being enhanced. Pres. Vizcarra also committed to ensuring that the country has access to a COVID-19 vaccine as soon as one is available.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.