Central banks & macro data: BCCh, BCB, & BCRP on deck; more November inflation numbers

Argentina: Wealth tax approved by Senate

Colombia: November prices undershot expectations as the VAT holiday drove inflation down to a new record at 1.49% y/y

Mexico: Consumer confidence lost momentum in November

Peru: One-year Inflation expectations ticked up in November, but still far from being a concern

CENTRAL BANKS & MACRO DATA: BCch, BCB, & BCRP ON DECK

I. A trio of central-bank interest-rate decisions

- Chile. The BCCh Board will deliver its next monetary-policy decision on Monday, December 7, where our team in Santiago, the consensus of analysts, and market pricing anticipate another hold at 0.5% (chart 1). However, we do expect a more dovish tone in the Board’s forward guidance, given that we project the recent spike in inflation to be transitory (chart 2), and a possible revisiting of the 0.5% technical minimum. The December Monetary Policy Report follows on Wednesday, December 9, where we anticipate seeing the BCCh upgrade its GDP growth forecasts to reflect the impulse from the imminent second round of pension-fund withdrawals. The minutes of the December 7 rate decision are due to be published on Wednesday, December 23. Our Chile economists project the BCCh to stay on hold until Q2-2022, but markets have been pricing a first hike in late-2021.

- Brazil. The BCB’s Copom is next scheduled to meet on Wednesday, December 9, where our Brazil economist expects the Selic rate to be held at 2.00% for a fourth meeting in a row (chart 3). In view of recent boost to our growth and inflation projections, we no longer see a strong chance of additional easing at this stage, but there is a material risk that hikes could be brought forward earlier than the first move we anticipate in Q2-2021 in an effort to shore up the BRL and respond to rising inflationary pressures (chart 4). While markets have been pricing a hold on December 9, they do anticipate a first hike in Q1-2021. Following its usual calendar, the minutes from the Copom’s meeting are due to be published on Tuesday, December 15.

- Peru. The BCRP Board will make its last planned rate decision for 2020 on Thursday, December 10, where we expect the headline policy rate to be held again at 0.25% (chart 5). The meeting is likely to be uneventful, with the BCRP focused on efforts to mitigate volatility in the PEN and ensure major sectors of the economy continue to be able to access adequate liquidity. We forecast inflation, currently at 2.1% y/y (chart 6), to end-2020 at 2.0% y/y.

II. More November inflation numbers

- Argentina. October industrial production and construction activity (Dec. 9) are expected to remain at and pull level with, respectively, numbers from a year ago.

- Brazil. We expect monthly IPCA inflation (Dec. 8) to accelerate from 3.9% y/y in October to 4.3% in November.

- Chile. November inflation (Dec. 7) is projected to come down just below the 3% y/y BCCh target.

- Colombia. In a quiet week, November consumer confidence (Dec. 7) is the only planned data release.

- Mexico. Our team in CDMX expects headline inflation to slow from 4.1% y/y in October to 3.4% y/y in November, but they don’t see this as the leading edge of a broader deflationary trend.

- Peru. October’s trade surplus (Dec. 9–11) is expected to expand on stronger mining output and higher metals prices.

See our November 28 Latam Weekly for our detailed forecasts.

—Brett House

ARGENTINA: WEALTH TAX APPROVED BY SENATE

Late on Friday, December 4, Argentina’s Senate approved the Congressional proposal to impose a one-off wealth tax that would target individuals with assets of more than ARS 200 mn (around USD 2.4 mn). The tax is intended to hit between 1% and 3% of individuals’ total wealth, with a 50% tax premium on assets held abroad. Similar wealth taxes have been abandoned in much of the world as they violate the principle of not taxing the same income twice, they rarely produce the revenues expected, they generate incentives to keep capital offshore, and they may discourage foreign investment. We don’t expect this move to plug the fiscal holes created by this year’s lockdowns and it may distract from and delay more meaningful fiscal reform.

—Brett House

COLOMBIA: NOVEMBER PRICES UNDERSHOT EXPECTATIONS AS THE VAT HOLIDAY DROVE INFLATION DOWN TO A NEW RECORD AT 1.49% Y/Y

November inflation decelerated further from October in data published late on Saturday, December 5, by DANE. In sequential monthly terms, deflation deepened from -0.06% m/m in October to -0.15% m/m in November, well below expectations (i.e., 0.06% m/m in the Bloomberg survey and 0.08% m/m in the BanRep survey) and our projection of 0.08% m/m. November’s soft print pulled annual inflation down by -26 bps from 1.75% y/y in October to 1.49% y/y, well below the Bloomberg survey’s 1.71% y/y consensus expectation; similarly, core inflation came down from 1.42% y/y in October to 1.01% y/y in November (chart 7).

November’s downside surprise reflected significant effects from the most recent VAT holiday and an unanticipated reduction in tuition fees for universities and technical colleges (charts 8 and 9).

- Colombia’s third VAT holiday this year had much stronger effects in November than the previous two VAT sabbaticals in June and July. The clothing sector (-3.71% m/m, chart 9 again) provided the largest negative contribution (-14 bps) to the headline inflation rate in November, mainly stemming from a large decline in prices on clothing goods (-3.81% m/m, table 1), where the price drop was 1.8x greater than the one we observed during the first VAT holiday. Additionally, the IT & communications group contributed negatively to headline inflation (-0.02 ppts, chart 8 again) owing to reductions in prices for cellphone services (-6.73% m/m, table 1 again). Finally, leisure-goods prices (-1.13% m/m) posted a strong decline compared with the previous two VAT holidays.

- Tuition fees at universities and technical education institutes fell again by -1.03% m/m, which meant education pulled headline inflation down by -0.04 ppts (chart 8, again). This was a residual effect of an atypical month where these institutions implemented price reductions to reduce desertion. DANE indicated that the negative effect of education prices on headline inflation would continue into December.

- On the other side, rental fees and restaurants registered price gains that reflected the consolidation of the economy’s re-opening (charts 8 and 9, again). Housing-related sectors also contributed positively to November’s headline inflation as utility fees (up 0.22% m/m) and rental fees (up 0.09 m/m) turned positive again and posted the fastest expansion in six months, a signal of a mild demand recovery. We think that December will see further signs of recovery in the tourism sector.

Looking at broad categories, goods inflation fell by -102 bps to 0.01% y/y, services inflation fell from 1.75% y/y to 1.55% y/y, and regulated-price inflation fell by -33 bps to 0.58% y/y. Monthly foodstuff inflation was almost flat (0.01% m/m) in November despite the fact that wholesale prices pointed to huge increases from two months ago.

Core inflation measures also dropped: ex-food inflation came in at 1.02% y/y (down -40 bps from October), while ex-food and regulated inflation fell by -42 bps from October to 1.13% y/y in November.

Altogether, November’s drop in CPI inflation represented a significant downward surprise. However, we could see further soft price prints in the short term due to an extraordinary measurement of school fees. We also anticipate that base effects could dampen year-on-year inflation numbers in Q1-2021, but annual inflation rates are expected to begin rising again by Q2-2021.

We still forecast next year’s annual inflation rate to converge to a level (i.e., 2.8% y/y) slightly below BanRep’s 3% y/y target by the end-2021. For now, we believe November’s headline inflation reading supports keeping the policy rate at 1.75% for the rest of 2020 and into H1-2021 as we project inflation expectations to remain anchored in the target range of 1% y/y to 3% y/y.

—Sergio Olarte & Jackeline Piraján

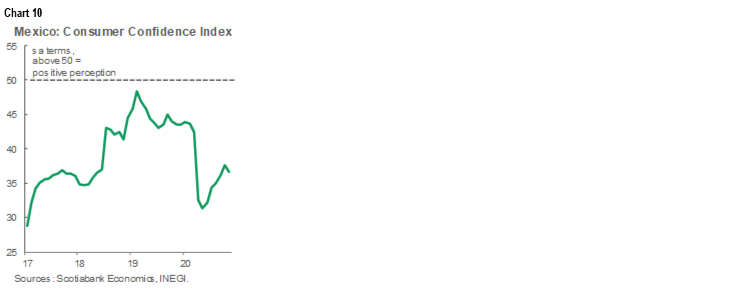

MEXICO: CONSUMER CONFIDENCE LOST MOMENTUM IN NOVEMBER

The results of the National Survey on Consumer Confidence (ENCO) for November, released on Friday, December 4, showed that sentiment weakened in seasonally-adjusted terms for the first time since June (chart 10), when the gradual re-opening of various activities started. The November reading, combined with rising COVID-19 new case numbers and ongoing uncertainty around the pandemic, likely foreshadowed a slowing in consumer spending in the coming months. Digging into the details:

- In November, the Consumer Confidence Index (CCI) came in at 37.1 points in nsa terms, -6.8 points lower than in November 2019, which marked a 12th straight month of year-on-year declines;

- In seasonally adjusted terms, the CCI decreased in November from 37.6 to 36.7, it’s first monthly decline after five consecutive months of increases; and

- All five components of the CCI (nsa) remained down compared with their levels in November 2019. These included assessments of the current and expected situation of households and the country, as well as evaluations of consumers’ current capacity to acquire durable consumer goods. In the same vein, all five of the components also fell in seasonally-adjusted month-on-month terms, with the greatest declines in those sub-indices related to current and expected perceptions of the economic situation of households, followed by those related to perceptions of the current and expected economic situation.

—Paulina Villanueva

PERU: ONE-YEAR INFLATION EXPECTATIONS TICKED UP IN NOVEMBER, BUT STILL FAR FROM BEING A CONCERN

The BCRP reported on Thursday, December 3, that market expectations of inflation over the next 12-month period had risen from 1.6% y/y in October to 1.7% y/y in November. The BCRP obtains this reading from a monthly survey of research analysts and financial institutions. The BCRP uses this information to determine its current estimate of the real interest rate (i.e., the interest rate minus the expectation for inflation 12 months from now), which is a key input for the central bank’s formulation of monetary policy. Thus, the real reference rate now stands at -1.45% versus -1.35% previously. However, so long as one-year inflation expectations remain within the BCRP target range (1% y/y to 3% y/y), we expect the BCRP to remain focused on stimulating the economy and will keep the reference rate at 0.25%. That said, we do expect inflation expectations to continue drifting up toward 2% y/y, following inflation itself which hit 2.1% y/y in November. Note that market inflation expectations are mildly lower than our forecast of 2.0% for November-December 2021.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.