Latam Economic Update

Colombia: July consumer confidence remained at low levels

Mexico: Private consumption and investment deteriorated further in May, but auto industry recovery continued in July

Peru: The new Cabinet is reasonable, but will Congress think so?

COLOMBIA: JULY CONSUMER CONFIDENCE REMAINED AT LOW LEVELS

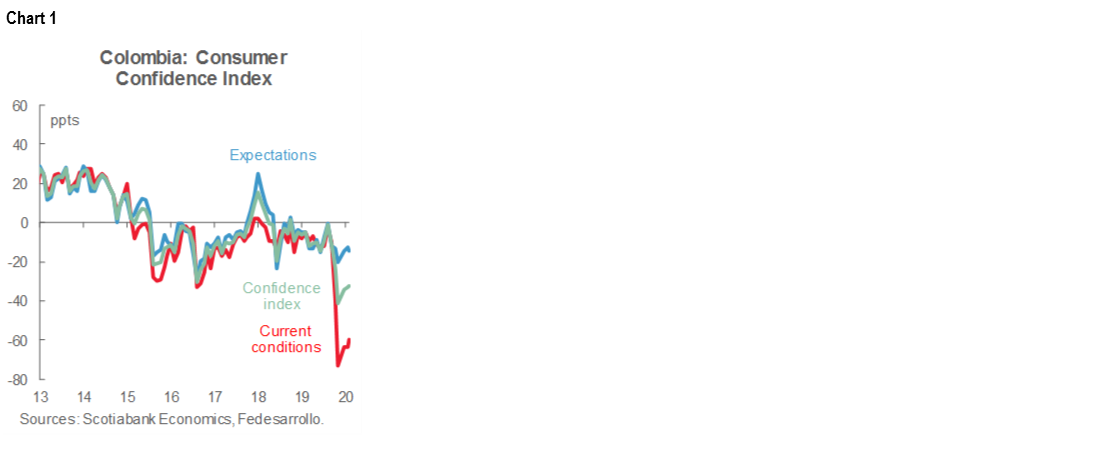

July’s Consumer Confidence Index (CCI), released on August 6, stood at -32.7 ppts—little changed from June's result of -33.1 ppts, but another month of small gains (chart 1). July’s reading shows that consumer sentiment remains fairly deep in pessimistic territory: the index can range from +100 to -100, where zero is neutral. In July, the Current Conditions Index improved to -59.9 ppts versus the previous -63.6 ppts in June. However, the Expectations Index deteriorated slightly to -14.6 ppts (versus the previous -12.7 ppts), partially offsetting the recovery on the assessment of current conditions. The mild improvement in the impression of current conditions could imply that the worst part of the employment-market’s problems are over, but recovery will be slow. The spread between the Expectations and Current Conditions Indices remained positive in July, which implies that consumers expect a better future. Any weakening in consumers’ assessment of their long-term prospects should be monitored closely.

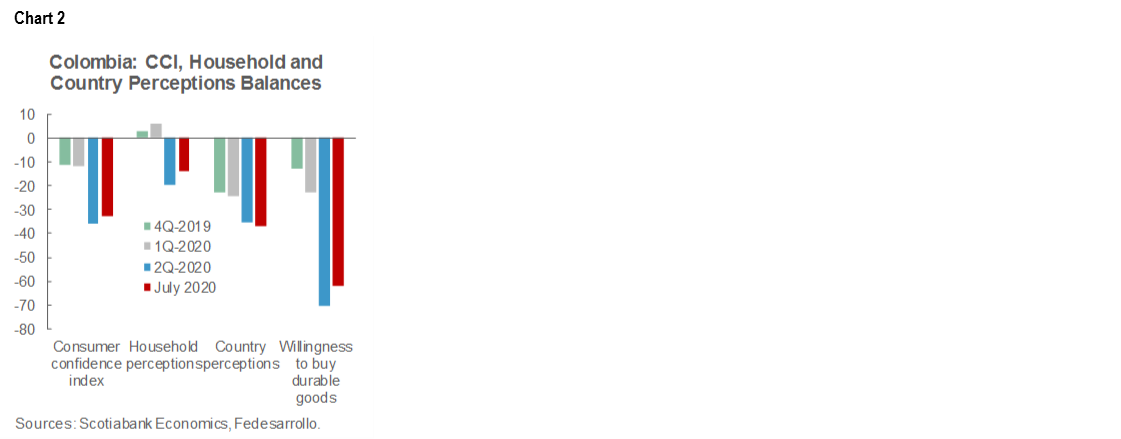

Consumer caution continues to dominate economic landscape: consumers’ willingness to buy durable goods is still weak (chart 2). Consumer confidence improved in July in two out of five cities surveyed; but in the main cities—Medellin, Barranquilla, and Cali—confidence deteriorated again, which we associate with the new regional lockdown measures. In Bogota, sentiment improved despite the increase in COVID-19 cases, probably owing to the new scheme of zonal lockdowns which is perceived as a tolerable measure to enable economic activity. Additionally, Bogota showed a strong increase in consumers’ willingness to buy houses, which can be related to subsidies for low-income homes.

By socio-economic levels, July’s indices showed a mixed picture. High-income earners' confidence fell slightly again, while low-income confidence levels increased somewhat. This is compatible with the increased willingness amongst this cohort to buy houses due to government efforts to subsidize the residential building construction sector, as stressed above. Consumers’ inclination to buy vehicles and durable goods—such as furniture and home appliances—was broadly unchanged compared with June, and remained at historically low levels, representing a significant challenge for economic recovery.

The apparent stagnation in consumer confidence implies that weak demand could weigh against further and/or faster economic recovery. In July, the re-intensification of lockdown measures in Colombia’s main cities may have weighed on any nascent rebound in sentiment: as the government moved to impose stricter measures, it emphasized that the pandemic will last a long time. In the coming months, any new improvements in consumer confidence will continue to depend heavily on the re-opening process and the employment situation.

—Sergio Olarte & Jackeline Piraján

MEXICO: PRIVATE CONSUMPTION AND INVESTMENT DETERIORATED FURTHER IN MAY, BUT AUTO INDUSTRY RECOVERY CONTINUED IN JULY

I. Auto industry recovery continued in July, but still at lower levels than before the pandemic

According to data released on Thursday, August 6, the Mexican auto industry showed some improvements in its year-on-year variations in July, but January–July volumes were still lower level than in the same period of 2019.

- Domestic sales of new cars improved from an annual decline of -41.1% y/y in June to a -31.1% y/y drop in July. With this, the January–July period was down -36.8% y/y (chart 3) versus -41.7% y/y in January–June.

- Auto production increased after four months of annual declines as industry activities re-opened further. Production increased by 0.7% y/y in real terms, (versus -29.2% y/y in June); yet the January–July period’s production was still down -35.5% y/y from the same period in 2019.

- Finally, the contraction in exports moderated in July from -38.8% y/y to -5.5% y/y, with exports down by -31.7% y/y in the first seven months of 2020.

Although auto industry activity is still at lower levels than before the pandemic, production and exports are recovering at a relatively swift pace as the rebound in the US unfolds. However, disruptions and uncertainty regarding COVID-19 are expected to continue through the coming months, which would hinder a total restoration of the industry to its pre-pandemic state.

II. Gross fixed investment drop at record pace in May

Additional data released on August 6 showed that in May gross fixed investment (GFI) dropped for a 16th consecutive month in year-on-year terms. The accelerating pace of decline reached -39.5% y/y in May versus -36.9% y/y in April, the swiftest monthly drop on record since 1995 (chart 4). For the January–May period, GFI fell sharply by -20.6% y/y, also the weakest pace on record.

- By components, equipment and machinery investment’s setback deepened from -37.9% y/y in April, to -46.7% y/y in May. Domestic machinery investment dropped from -52.6% y/y to -56.0% y/y, while investment in imported machinery and equipment contracted further, going from -28.9% y/y in April to -40.1% y/y in May.

- Construction investment slowed its decline from -36.1% y/y to -33.7% y/y, with its residential subcomponent improving from -40.6% y/y to -36.8% y/y and the non-residential component up from -31.5% y/y to -30.5% y/y.

- On a monthly basis, seasonally adjusted GFI figures showed a much smaller drop, going from -28.9% m/m in April to -4.5% m/m in May, although these last numbers might be subject to revisions owing to the impact of COVID-19.

Uncertainty continues to hinder growth in GFI: both the pandemic and the business environment are drags on investment growth.

III. Private domestic consumption remains weak

Private domestic consumption further accelerated its historical decline in the year-on-year comparison between May 2020 and May last year. On the other hand, seasonally adjusted month-on-month measures show the path of consumption declines slowing, according to data published on August 6, by INEGI.

- Growth in private domestic consumption fell further from -22.3% y/y in April to -24.8% y/y in May, versus 0.3% y/y a year earlier (chart 5). May’s decline marks consumption’s biggest year-on-year pullback on record.

- Consumption of services, domestic goods, and imported goods all saw deeper year-on-year contractions in the move from April to May.

- In the accumulated January–May period, consumption was down by -9.9% y/y (versus 0.8% y/y in the same period of 2019), its weakest performance for this stretch since records became available in 1994.

- After consumption registered its largest month-on-month decline in April with a -19.6% m/m sa contraction, sequential consumption growth improved to -1.7% m/m in May, driven, predictably, by the gradual processes of re-opening that began throughout the country.

The consumption figures continue to reflect the partial closures of most of the country's economic activities in order to minimize the spread of COVID-19.

—Miguel Saldaña & Paulina Villanueva

PERU: THE NEW CABINET IS REASONABLE, BUT WILL CONGRESS THINK SO?

The new Cabinet was sworn in by President Vizcarra on Thursday, August 6. This Cabinet will be headed by Walter Martos, a retired army general who was, until yesterday, Minister of Defense. Martos is an odd choice, and yet an understandable selection at the same time. Odd, because Peru is facing health, economic, and political crises, and Martos is not particularly experienced in any of these three areas, although he has been part of the government’s COVID-19 task force. Furthermore, a retired military leader is not a usual cabinet head in Peru. And, yet, Martos is an understandable choice because someone like him, who is not controversial—and, indeed, has not been politically visible—is perhaps more likely to be accepted by Congress than more obvious alternatives. His prestigious military career, having been Chief of the High Command of the armed forces, might also help. However, given the erratic behaviour of the current Congress, there is really no guarantee as to how its members will respond to Martos’ selection.

Martos had been Minister of Defense since October 2019, which allowed him to work closely with President Vizcarra, and with most of the Cabinet. Aside from Martos, only four of 18 Cabinet positions have changed hands: Jorge Chávez replaces Martos at the Ministry of Defense; Antonina Sasieta is the new Minister of Vulnerable People; Javier Palacios replaces Martín Ruggiero at the Ministry of Labour; and Luis Incháustegui replaces Rafael Belaunde at the Ministry of Energy and Mines. The changes at the Ministry of Labour and at the Ministry of Mines were a partial concession to Congress, which had criticized Ruggiero and Belaunde for being too young and too pro-business. However, the Cabinet roster is not entirely conciliatory, as the Minister of Education, Carlos Benavides, has been kept on even though there had been widespread speculation that he was the individual that many members of Congress most wanted out of Cabinet. Benavides is linked to the university reform effort, which many members of Congress with personal interests at stake would like to lay to rest. President Vizcarra had previously stated that the university reform agenda was non-negotiable. It will be interesting to see how members of Congress react to the ratification of Benavides.

All other Cabinet members remain in their posts. Of particular importance, both María Alva and Pilar Mazzetti were re-ratified in the key positions of Minister of Finance and Minister of Health, respectively. Overall, this new Cabinet is plausible and reasonably pro-market. This is not a Cabinet that will dramatically change government policy, which is good for stability and continuity. There is no reason why Congress should find this Cabinet unacceptable, but, then again, there was no real reason why it should have found the previous Cabinet unacceptable either.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.