Latam Economic Update

Colombia: Coincident indicators beat expectations while imports led to a narrowing trade deficit

Mexico: Banxico cut benchmark rate by -50 bps to 4.50%

COLOMBIA: COINCIDENT INDICATORS BEAT EXPECTATIONS WHILE IMPORTS LED TO A NARROWING TRADE DEFICIT

I. June’s coincident indicator improved more than anticipated

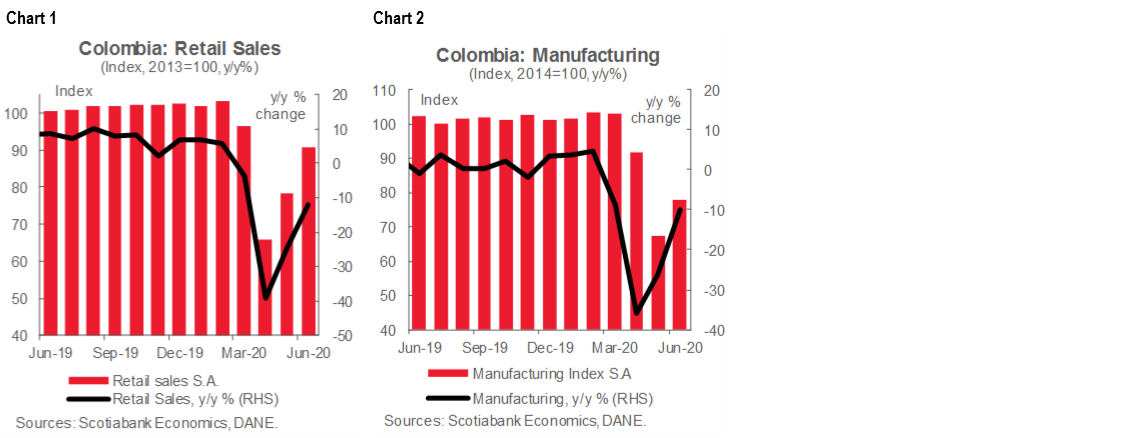

On Thursday August 13, DANE released real retail sales and real manufacturing production data for June. Both indicators came in above expectations, showing that the economy is improving at a faster pace than anticipated. Real retail sales declined by -14.2% y/y (chart 1), better than market expectations (-16% y/y). Real manufacturing production fell by -9.9% y/y (chart 2), also better than expected (-15% y/y).

According to our estimates for June, around 20% of the economy was shut down. High-frequency data showed that the re-opening process continued in June, which implies better numbers in both indicators for the month. Prospects for further recovery are positive since the main cities are developing strategies to open more sectors such as commercial flights and restaurants. For now, June’s numbers could lead to a better-than-expected Q2 GDP result (to be published later today).

On the retail sales side, gasoline (-23.2% y/y), vehicles (-37.9% y/y), and clothing accounted for 80% of the contraction. These contractions are directly related to mobility restrictions and weaker demand due to the COVID-19 shock. On the positive side, staples consumption continued performing well, with foodstuffs (up 2.0% y/y), and cleaning products (up 28.1% y/y) both showing gains. Additionally, the VAT holiday led to better results in household appliances purchases (+29.3% y/y).

On the manufacturing side, production in 31 out of 39 sub-sectors fell in y/y terms. The worst-performing sectors were those related to the oil sector and clothing, which accounted for one-third of the contraction. Oil refining contracted by -26.9% y/y, clothing fell by -35% y/y on lower demand pressures. Mining-related construction materials continued contributing negatively, however it was in a lower proportion than previous months as construction re-opening is gaining momentum.

It is worth noting that the manufacturing decline is equivalent to a shutdown of around 3.3 business days, which is smaller than our estimate for the extent of May’s closure (8.6 days). Manufacturing has contracted by -12.4% y/y year-to-date.

June’s indicators surprised us positively, affirming that the worst of the lockdown’s effects on the economy were in April and that the economic recovery is gaining momentum. July’s data should improve further, although probably at a more moderate recovery pace. In the coming months, the country’s main cities, such as Bogotá and Medellin, are kicking off new pilot plans on commercial flights and restaurants that could continue leading the recovery. Additionally, Barranquilla lifted some mobility restriction and shopping areas are getting better dynamics. In terms of monetary policy, yesterday’s positive data surprise supports BanRep’s gradual approach in adjustments to the monetary policy rate. We think BanRep will cut the monetary policy rate by -25 bps to 2.0% at the August 31 meeting.

II. June’s imports fell by -27.2% y/y, monthly trade deficit contracted by -37% y/y

June’s import data, released on Thursday August 13, came in at USD 2.9 bn (chart 3), and remained close to the lowest levels since February 2010, which represented a contraction of -27.2% y/y. Manufacturing-related imports fell by -25% y/y and accounted for most of the y/y decline. Year-to-date, imports contracted by -19.7% y/y, and helped stabilize the trade deficit. In the forthcoming months, we expect further moderation in the external balance due to a high base in 2019 for the annual comparison in capital goods imports and weaker domestic demand in 2020 due to the pandemic.

From the perspective of imports by use, there were declines in all three major items. Capital imports declined -28.7% y/y (chart 4) due to contractions in transportation-related sub-sectors (-59.8% y/y) and construction (-57.2% y/y). Consumption-goods imports fell by -16% y/y (chart 4 again), owing mainly to a significant decline in durable goods imports (-48.2% y/y). Non-durable goods imports fell -9.6% y/y. Raw materials imports contracted by -31.9% y/y (chart 4 again), mainly due to a drop in fuel oil imports (-81.5 % y/y).

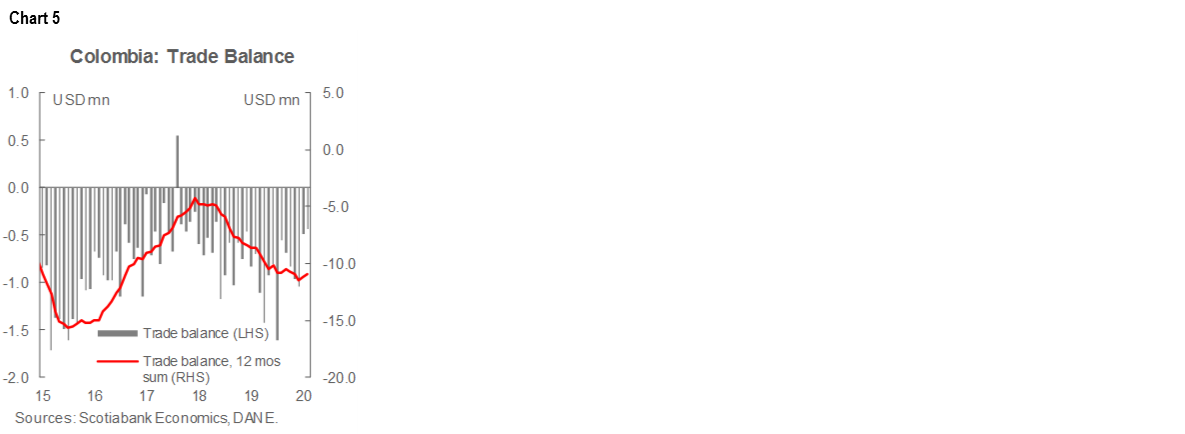

A generalized weakening in domestic demand reflected in import data should prevent further deterioration in Colombia’s external accounts. The trade deficit came in at USD 443.5 mn in June, -37.4% y/y, which took the YTD deficit to USD 4.02 bn (chart 5), showing that the external balance is reacting to automatic stabilizers since imports shrank more than in the previous month. All of these should help maintain the current account deficit at around 4.1% of GDP or less in 2020.

—Sergio Olarte & Jackeline Piraján

MEXICO: BANXICO CUT BENCHMARK RATE BY -50 BPS TO 4.50%

Banxico lowered the benchmark rate to 4.50% as the easing cycle may be near. At its sixth monetary policy meeting of the year on August 13, 4 of the 5 members of Banco de Mexico’s Board of Governors decided to lower the overnight interbank rate—for the tenth consecutive time—by -50 bps to a level of 4.50%, in line with market expectations. The remaining member voted for a -25 bps cut.

Banco de Mexico noted that the economy shrank sharply in Q2-2020 as the impact of the pandemic intensified. Thus, slack conditions are expected to widen in a context where significant downside risk for growth persist.

Regarding inflation, the press release stated that headline inflation expectations rose for the end of 2020 owing to recent increases in energy prices and changes in the composition of core inflation, however, for the next 12 and 24 months headline inflation is expected to be around 3%, consistent with its inflation target. Overall, the balance of risk for inflation remains uncertain. Key downward pressures, as a wider output gap and worldwide downward inflationary pressures remain, while other events, such as a possible further depreciation of the MXN, logistical and supply-related problems and potential stickiness of core inflation, could increase upside inflationary pressures.

Banxico provided some cautious guidance on the way forward, noting that “available room for maneuver will depend on the evolution of the factors that have an incidence in the outlook for inflation and its expectations”. With this, the end of the easing cycle seems near, but will clearly rely of the future path of inflation.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.