ON DECK FOR WEDNESDAY, MAY 13th

KEY POINTS:

- Bland markets await potentially key developments

- Trump-Xi Jinping meeting starts tonight amid low expectations

- US PPI to further inform estimates for the Fed’s preferred inflation gauge

- BoC’s deliberations are unlikely to reveal anything new

- Canada should avoid the ‘Golden Dome’

- Canada’s gas refinery margins are soaring

- Canadian insolvency hysteria

- Aussie wage growth remains modest

An otherwise light calendar will have markets fixated on any further developments concerning Iran and the start of US-China bilateral meetings this evening.

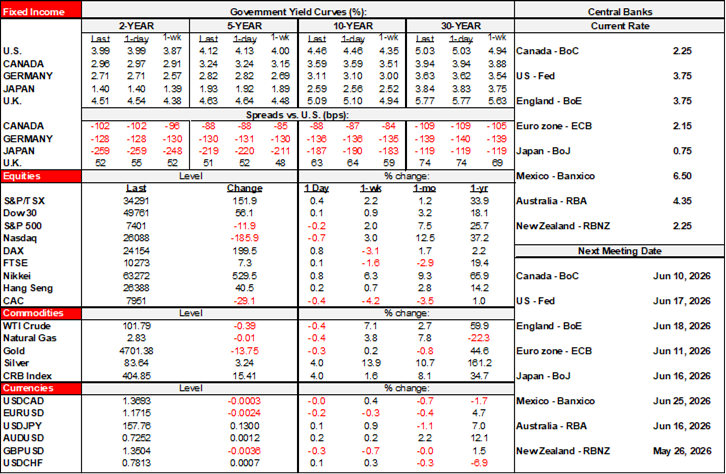

Markets are starting off the day in rather bland fashion. Oil is meh. Sovereign bond yields are little changed. Ditto for equities. The dollar is a touch firmer but flat against most crosses. Markets are clearly waiting to seize on new information.

TRUMP ET AL GO TO CHINA

Trump just landed in Beijing with his large entourage of officials and corporate leaders as this note is being published. The first bilateral meeting is thought to occur late this evening (10:30pm–onward, or 10:30am Thursday in Beijing). There will be plenty of pomp and circumstance and probably praise for Trump given he seeks it. Based upon past practices there may be a joint statement sometime in the wee hours of Thursday morning (ET), or 1pm–onward Thursday afternoon local time. The joint statement and any reported sense of progress—or lack thereof—could be impactful through tonight’s Asian market session and into Thursday’s N.A. open.

On the docket in the meetings are a) Iran, b) tariffs, c) Taiwan, d) AI, and e) possible other trade issues. Expectations are mixed but I think there is a high bar set against major breakthroughs versus token announcements perhaps like repackaging Boeing orders that may have been placed in any event. I’ve read a lot of accounts of what may be expected and they all share one thing in common: low expectations and nervousness. Of the two leaders, I would think Trump would be more likely to blink as China has dug in against his threats and measures and given his pattern of behaviour ahead of midterms amid sagging polling and affordability challenges. China knows that Trump is a wildcard who says one thing, does another, threatens a lot, and goes back on his commitments. Xi Jinping is no fool.

US PRODUCER PRICES TO INFORM PCE EXPECTATIONS

The US releases producer price figures for the month of April this morning (8:30amET). Headline prices are expected to rise by 0.5% m/m (Scotia 0.4%) with core producer prices (ex-food and energy) up 0.3% (Scotia 0.3%).

Key will be translating several components like airfare, some health sector prices and portfolio administration fees into weighted contributes to PCE inflation that is due out on May 28th and combining that with CPI contributions to the PCE estimate.

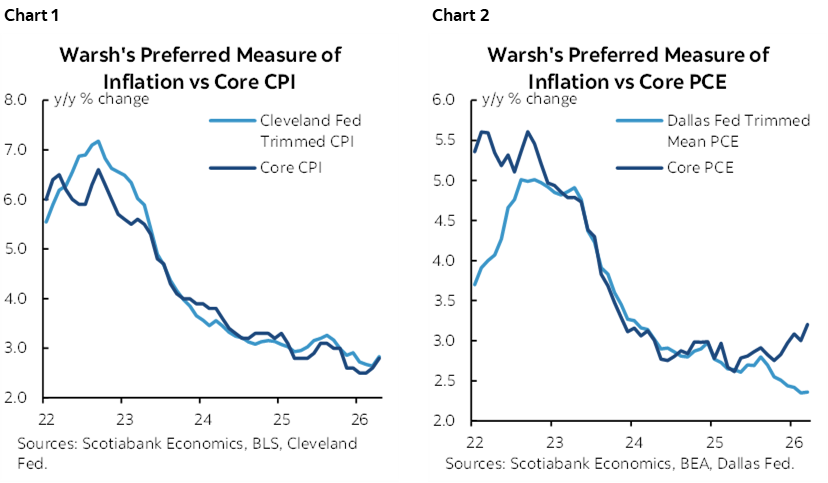

As for yesterday’s US CPI figures (recap here) of note is that the Cleveland Fed’s trimmed mean CPI reading matched traditional core CPI last month (chart 1). So did their weighted median CPI measure. At least on a CPI basis, incoming Fed Chair Warsh’s preference for trimmed inflation measures over traditional core inflation suffered a blow. We’ll see what happens with core PCE and trimmed core PCE at month end given that’s where more of the divergence has been occurring (chart 2).

BOC’S SUMMARY OF DELIBERATIONS

Zzzzzzzz…..the BoC releases its Summary of Deliberations (1:30pmET) that attempts to reflect the dialogue that was conducted in the lead up to the April 29th decision. It was forced upon the BoC by the IMF that demanded improved transparency, but it falls short of more useful minutes. I expect absolutely nothing from today’s release given abundant communications on game day in the statement and the MPR and press conference, then media interviews, and in two rounds of parliamentary testimony. It will just be a re-hashed exercise in what you should already know.

OVERNIGHT STUFF

The won ignored a one-tick increase in South Korea’s unemployment rate to 2.8% in April but tumbled along with the Kospi stock index after headlines hit about strike risk at Samsung and general negativity around chip stocks.

Australian wages continue to post moderate growth of 3.3% y/y and 0.8% q/q (chart 3).

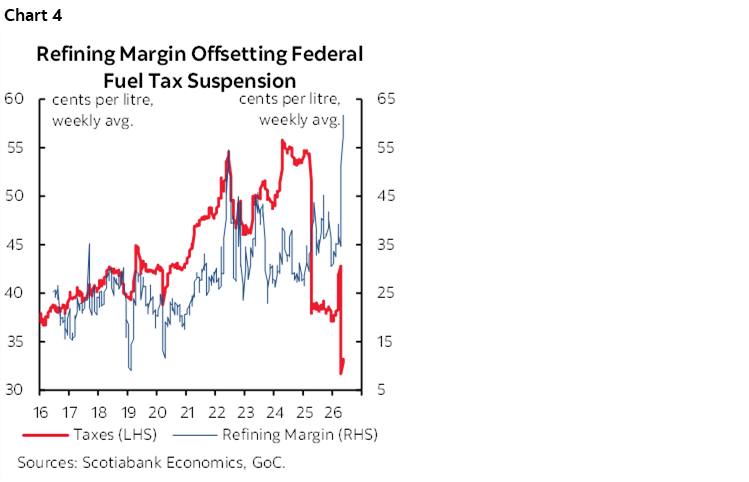

CANADIAN REFINERY MARGINS HAVE GOBBLED UP THE FUEL TAX CUT

Have a look at chart 4. It shows Canadian refinery margins, defined here as the spread between wholesale gasoline prices and crude prices. They’ve exploded and the timing of the move raises questions.

One reason why refining margins may have widened is because analysts point to a tighter gasoline market than even what’s going on in crude and due to supply factors as well as a pick-up in demand into the Spring and Summer driving seasons. That could explain some of the widening which is basically a fancy way of saying that refineries have pricing power.

Yet the refining margins have particularly widened since the 10 cent/litre fuel tax suspension on April 20th. Back then, then margin was 47 cents/litre. Today it is 60 cents. That 13-cent widening has eaten the tax cut.

Whether that’s because of the general economics of the gasoline market or because the incidence effects of the tax cut flowed to producers is unclear but I suspect it’s a bit of both. As a result, you really can’t say with any clarity that the tax cut has benefited consumers as the price per litre of the regular stuff has gone from about C$1.71 to $1.91. It’s feasible that the higher grades may have seen at least as much widening.

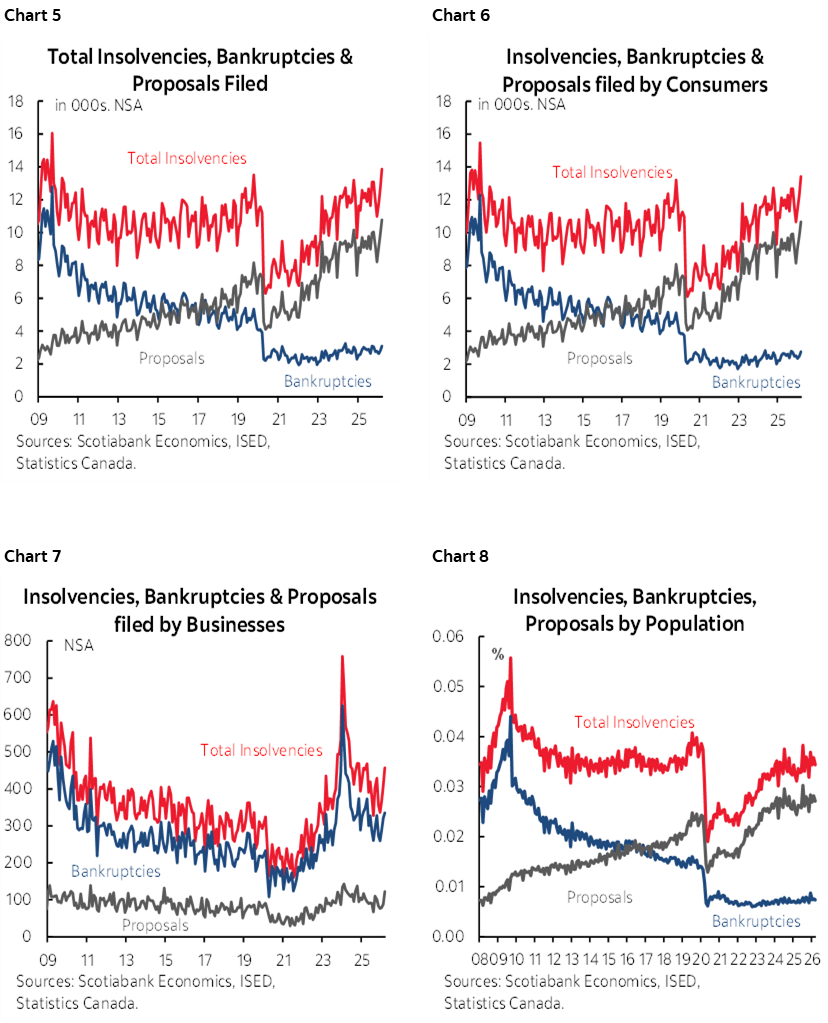

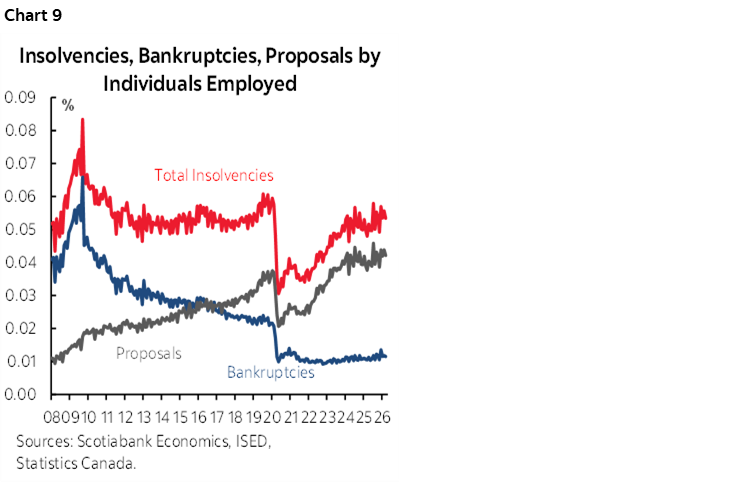

CANADIAN INSOLVENCIES—FACTS VS HYSTERIA

What’s going on with Canadian insolvencies? Are they as bad as some are depicting?

Enter the five charts 5–9. They show that the total number of business and consumers bankruptcies remains low. The number of consumer bankruptcies remains very low along a flat trend as the number of proposals to work out terms has continued to rise and which is driving higher total insolvencies (the sum of bankruptcies and proposals). On a per capita basis and per employed person basis, consumer bankruptcies, proposals and insolvencies are very low. Canada has a more collaborative borrower-lender set of arrangements than, say, the US where strategic defaults and jingle mail are more prevalent at times of stress. This is a strength of the Canadian system.

Shifting to business insolvencies, the picture is a little different. Bankruptcies are off the peak but higher than proposals and higher than the pre-pandemic experience, but still relatively low. Some businesses are indeed struggling. In other cases, creative destruction is driving change and coverage needs to be careful. You wouldn’t want to quash all bankruptcies with supports in a way that would interfere with the reallocation of resources away from nonviable businesses toward others that can use the workers and resources more productively.

CANADA SHOULD AVOID THE GOLDEN DOME WHITE ELEPHANT

The US Congressional Budget Office issued an updated assessment of the full 20-year project costs of the Trump administration’s ‘Golden Dome’ idea. It’s now up to US$1.2 trillion to develop, deploy and operate over 20 years. Every time they estimate it the bills goes up by hundreds and hundreds of billions. Last year, the CBO said it would cost US$542 billion just for the space-based components. Trump said last year that the whole thing would only cost $175 billion. The CBO’s fiscal projections are typically way off from reality for various reasons and a project like this one is extremely difficult to cost out, but the escalating price tag probably has yet to peak given the history of defence and infrastructure projects.

The best advice to Canada in my opinion is to avoid participation. Supporters will say that a nuclear strike would be more costly. Detractors would say it’s unproven technology, that Israel’s dome lets through plenty of missiles, and that all you need to do is slip a terrifying weapon under the dome. Getting strung along by cutting a cheque to participate risks Canada spending hundreds of billions on unproven technology with no exit once you’ve embarked along this path.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.