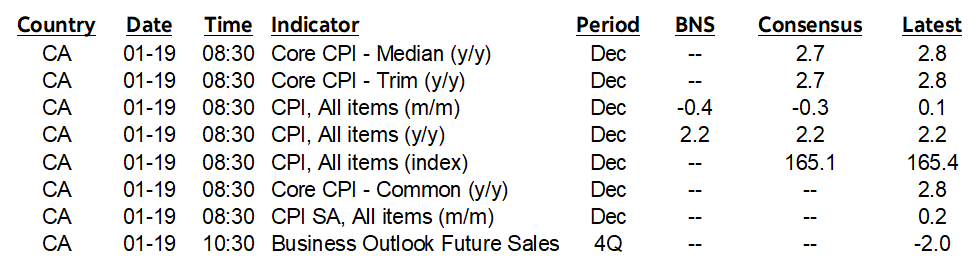

ON DECK FOR MONDAY, JANUARY 19TH

KEY POINTS:

- Tariff threats and troops sink risk appetite

- China’s economy performed largely as expected to end 2025

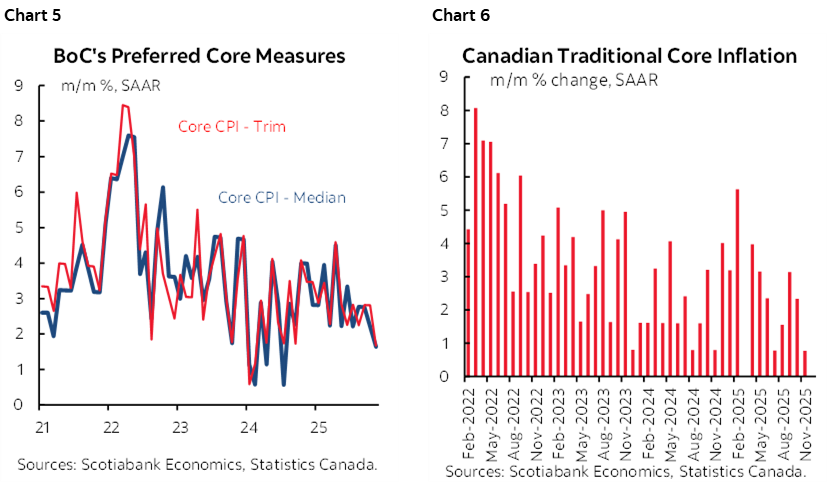

- Canadian CPI: was the dip in core measures an aberration?

- BoC’s Q4 stale surveys due today

- US markets shut for MLK Jr Day

- Global Week Ahead — Happy Anniversary?! (reminder here)

Gold is up by about US$65/oz to $4,660, stocks are broadly lower by 1%+ across most major benchmarks and the dollar is slightly softer against major crosses. EGBs are slightly richer at the front end in a bull steepener move. US market participants are generally watching from the sidelines given the US holiday.

The culprit is rising tensions caused by Trump’s aggression toward Greenland as an extension of his hemispheric ambitions as Europe responds with troops and tariffs in an effort to stop the steal. Canada is close to approval for sending troops in a show of solidarity with Europe which it frankly must if it wants Europe’s support for any US sovereignty challenges against Canada. Enter the irony of Trump’s ‘Board of Peace’ even if we plug our noses and ignore Putin’s participation.

The EU is preparing about €93 billion of retaliatory tariffs to counter Trump’s weekend threat that an extra 10% tariff would be applied against countries opposing his will to snatch Greenland. That may come to include Canada, and/or it may threaten CUSMA trade negotiations that are stalled in any event.

I’ve said from the start that trade agreements with the US administration would have short shelf lives and become practically worthless. Capitulation on the bad terms that Europe unwisely agreed to would have the US administration repeatedly coming back for more on some other issue, like metals, or hegemonic territorial ambitions. Be careful what you agree to in the short-run as US trade aggression is an insidious multi-act play. Canada has seen likewise, after the CUSMA/USMCA deal was supposedly the best trade deal in history, only to be attacked again in Trump 2.0. And here we are, with passage of said ‘deal’ with Europe in jeopardy within the European parliament. Tensions rising between allies—hopefully not entirely in a past tense—and rising domestically with 1,500 troops off to Minnesota. Americans fighting Americans, and Americans confronting allies.

CHINA’S ECONOMY PERFORMS AS EXPECTED

China updated a set of macro figures that had little effect given how close they were to expectations and the dominance of other market drivers.

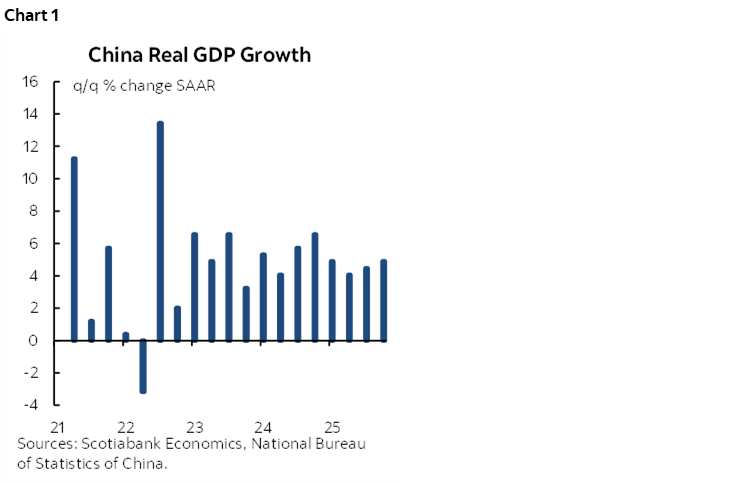

- Q4 GDP grew by 1.2% q/q SA (1.1% consensus) for the strongest gain in three quarters (chart 1).

- Retail sales were up 0.9% y/y in December (1% consensus). They fell in m/m seasonally adjusted terms in an extension of a pattern since mid-year (chart 2).

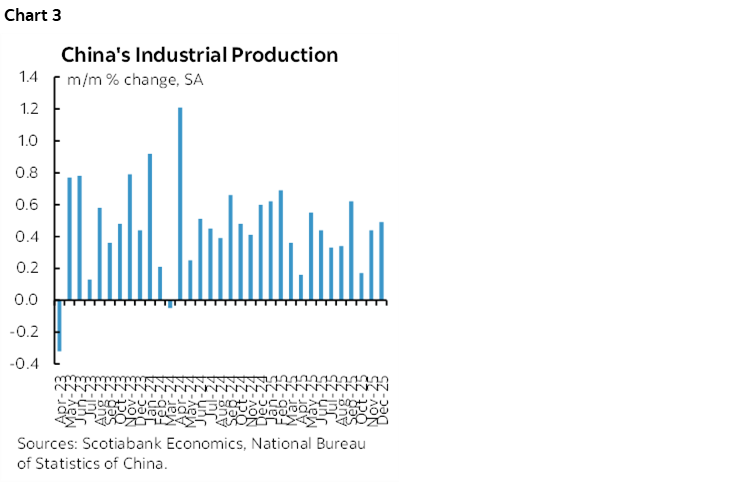

- Industrial production was up by 5.2% (5.0% consensus) and posted another m/m gain (chart 3).

- The jobless rate held unchanged at 5.1%.

- Fixed investment continues to fall (-3.8% ytd/ytd) with property investment down by 17.2% ytd/ytd.

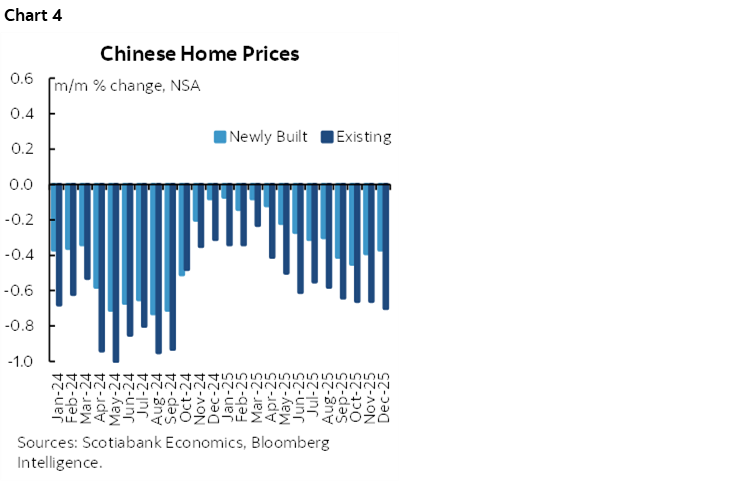

- House prices continue to fall (chart 4). New home prices fell by another –0.4% m/m SA in December for the 31st consecutive monthly decline. Resale prices fell by another –0.7% m/m SA in December for the 32nd consecutive monthly decline. Monetary easing faces inelastic demand for money given a lack of confidence in an environment of continually falling prices.

CANADA TO UPDATE CPI

Canada refreshes CPI figures for December that frankly won’t really matter to the BoC (8:30amET). The signal that they are on hold for an extended period is clearly communicated. See my Global Week Ahead for further explanations of our BoC views and a preview of CPI.

Consensus is looking for a -0.3% m/m seasonally unadjusted dip in CPI as per the polling convention. Estimates vary from -0.1% to -0.6% (Scotia -0.4%) except one outlier that seems to have gotten the sign wrong or that was inputted incorrectly.

Very few bother to input estimates for the y/y rates of chance in weighted median and trimmed mean CPI because, well, they’d be doing so on a total lark and they’re not the measures that matter. The sensitivities of the calculations to tiny movements in unobservable individual prices can swing the estimate of the 50th percentile price change (weighted median) and the 20% of prices in both tails that get removed (trimmed mean) make for only random chance to getting it right. Further, they’re not even y/y measures and are mislabelled as such; they’re rolling 12-month weighted calculations of the m/m changes.

What does matter are the trends in m/m seasonally adjusted changes in the various core measures of CPI. Charts 5 and 6 show the prior month’s sharp deceleration. Whether that was the start of a new trend or an aberration and whether the details stand up to scrutiny will be what matters a bit.

So let’s see the numbers and then judge accordingly.

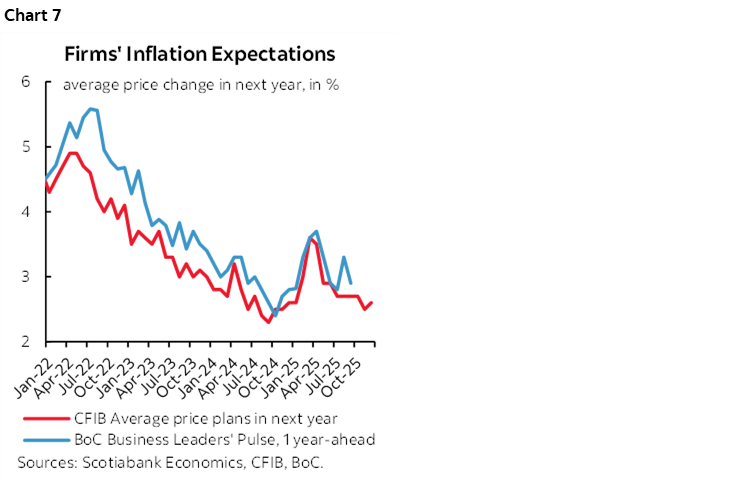

The Bank of Canada will then refresh its lagging quarterly business and household surveys two hours afterward. They’ll include refreshed measures of inflation expectations that are likely to slip lower based on higher frequency leading indicators (chart 7). So. Businesses and consumers are bad at forming expectations, don’t understand CPI figures, and routinely get it wrong.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.