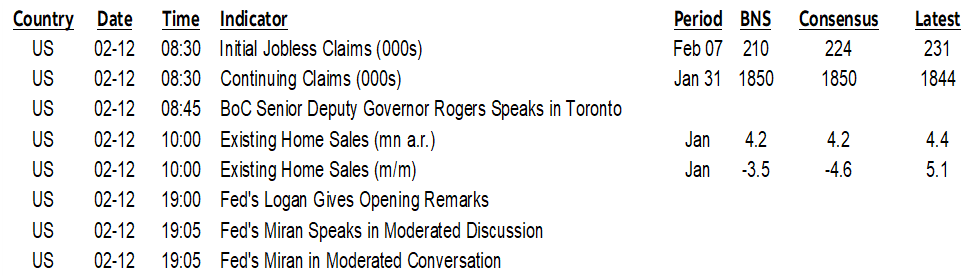

ON DECK FOR THURSDAY, FEBRUARY 12TH

KEY POINTS:

- Mild risk-on sentiment after dubious nonfarm beat

- Why the US household survey was cooked last month…

- …and hence the half million gain in jobs and the dip in the UR should be ignored…

- ...and next month’s household survey correction is likely to be a doozy

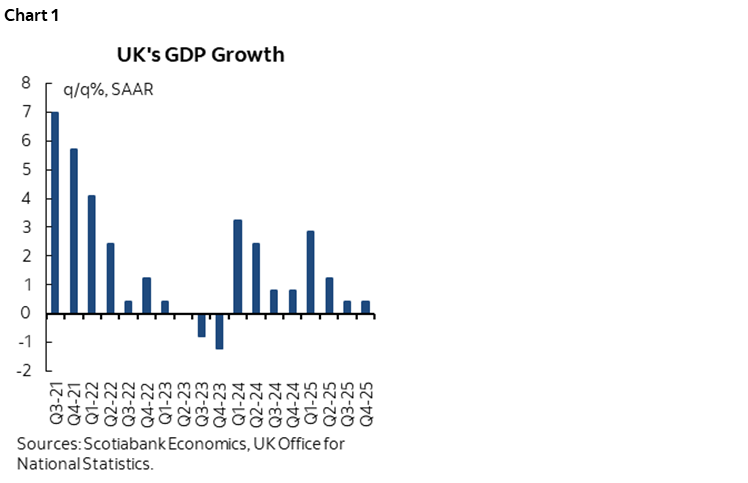

- Soft UK macro readings were ignored

- Nikkei loses team as the show-me phase settles in

- BoC’s Rogers to half-heartedly speak on AI this morning

- US home resales, claims and limited Fed-speak on deck

- Congress’s performative, self-serving tariff stunt

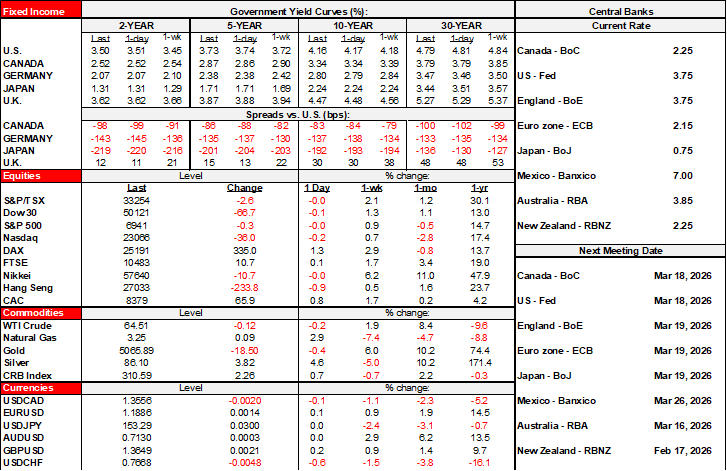

There are shades of risk-on behaviour across global markets this morning. Equities are broadly higher with N.A. futures up by about ¼% at the time of writing and Europe led by an over 1% gain by Germany’s DAX. Japan’s Nikkei has run out of gas over the past couple of sessions following large post-election gains and is now in the show-me phase. The dollar is slightly softer and CAD has shaken off yesterday’s laughable USMCA tear-up rumour. Sovereign bonds are treading water.

Why? Because overnight developments were light in the wake of an illusory gain in nonfarm payrolls and there isn’t much on tap for today.

UK MACRO UPDATES WERE IGNORED

UK macro readings generally disappointed but markets didn’t pay much heed. UK rates are not performing any differently than elsewhere, nor are pound sterling and the FTSE 100. Here’s the low down:

- Still weak GDP grew 0.1% q/q SA nonannualized in Q4 with 0.2% expected (chart 1).

- December GDP grew as expected (0.1% m/m SA), but the prior month was revised down a tick to 0.2%.

- Factories and construction stumbled. Industrial output fell -0.9% m/m (0% consensus) after a strong prior gain and manufacturing was part of that (-0.5%, prior 1.9%). Construction fell -0.5% m/m (+0.5% consensus) with upward revisions to show a smaller contraction.

- services output expanded 0.3% m/m in December (0.1% consensus) but was revised two-tenths lower to +0.1% in November.

- the trade deficit narrowed as imports (-2.4% m/m) fell faster than exports (-1.0%).

US — MINOR MACRO REPORTS, PERFORMATIVE STUNTS

The House voted by a thin margin to eliminate Trump’s tariffs against Canada. And it’s going nowhere. It will go to the Senate, likely pass there, and then off to Trump’s desk to get vetoed. The six Republicans who joined 213 Democrats (one was opposed) are acting in this fashion for two reasons. One is self-interest as their own hides will be on the line on November 7th. Two is because they know it’s not going anywhere anyway. My question to all of them is where were you over the past year before you began to fear voters?

Weekly claims data (8:30amET) and an expected fall in existing home sales during January (10amET) are on tap.

A pair of Fed officials speak tonight. Dallas Fed President Logan (7pmET) only delivers opening remarks, and then Governor Miran speaks a few minutes later. Miran said yesterday that he still believes rates can be lowered notwithstanding an overly rosy interpretation of the jobs report.

BOC ON AI

Bank of Canada Senior Deputy Governor Rogers begrudgingly appears this morning. I say begrudgingly because there will be no speech, no media, and no audience Q&A. Right, really into this aren’t we. It will be a 45 minute fireside chat at 8:45amET at a business school along with former Finance Minister Bill Morneau (here). The session is labelled “productivity and AI.”

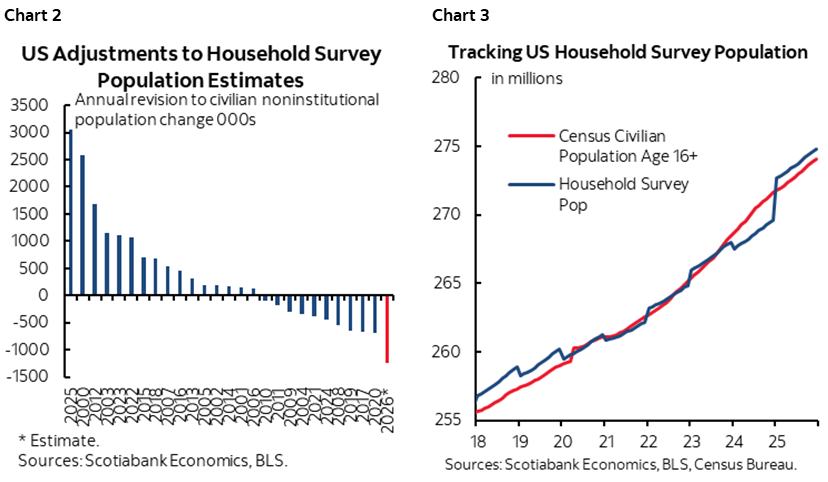

WHY A RECORD DOWNWARD REVISION TO THE US HOUSEHOLD SURVEY IS COMING

As follow up to my high scepticism toward yesterday’s US job market readings (here) there is one issue I hinted at that requires further explanation. I flagged that the unusual continued use of outdated population counts in the companion household survey—from which the unemployment rate is derived—by the BLS likely distorted the household survey’s readings for employment and the labour force. Normally those population counts would have been revised in January’s report.

Some number crunching shows how vulnerable the household survey will be to revisions next month.

The issue that I noted is that the BLS delayed the annual incorporation of revised population counts it normally does each January to next month in February's report in March.

The purpose of the annual population count revisions is to benchmark what the BLS has been applying in terms of assumed population growth by month to what the Census Bureau estimates to have been the population change. They do it once per year only to the single month and do not incorporate revisions stemming from the updated population counts over prior months. That’s why there is always a discrete jump or drop in January’s estimates of the noninstitutionalized population 16+ within the household survey every January off of which employment and labour force changes are then derived.

This time, however, they'll be revising down. By a lot. That’s because ever since January of last year, the BLS has been using the CBO’s projected level of population counts as at that time and based on the 2024 vintage. This means they’re using population counts dating back to before ‘Inauguration Day’ after which immigration policy tightened rather sharply.

How much of a difference could this make? I tentatively figure that using current Census Bureau counts as at January this year would revise down the BLS estimate of the 16+ noninstitutionalized population by about 1.25 million people. This difference is derived from tracking the Census Bureau’s monthly population counts up to the present and the BLS household survey’s counts for the 16+ noninstitutionalized population. This would be a record downward revision as shown in chart 2 that shows this estimate along with annual population count revisions normally in January of each year. Chart 3 shows how the BLS measure of the 16+ noninstitutionalized population is presently overshooting the Census Bureau’s estimates.

If we apply a steady 59.8% emp:population ratio from this latest report, then the household survey's measure of employment could be revised down by about 750k jobs in February’s report next month as a one-off level adjustment. If we also apply a steady labour force participation rate of 62.5% from this latest report, then the labour force would be revised down by about 780k.

Because of this delay in revising population counts, January’s estimated 528k gain in employment and 387k gain in the labour force were misleading. Both would have probably been strong negatives if not for the delayed incorporation of more realistic population counts.

In short, I have no confidence in the household survey’s readings and hence the dip in the unemployment rate. And it’s not going to get any better. In fact, the issue may persist throughout this year if immigration policy continues to tighten.

This adds to normal reasons to have little confidence in the household survey’s readings. Like the ginormous confidence bands around the estimated change in unemployment as flagged in my nonfarm note. Like falling survey response rates that were particularly bad last month because so many Americans were digging out of snowstorms during the household survey’s reference week.

How the household survey actually changes next month is also complicated by whatever happens at the margin, but the downward hit from revised population counts and the falsely high jumping off point from January’s readings are likely to make for a very weak set of household survey readings.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.