ON DECK FOR THURSDAY, SEPTEMBER 4

KEY POINTS:

- Markets bracing for a dovish payrolls reading ahead of today’s teasers

- Miran’s Senate grilling likely to contain some fireworks

- US job cuts increased in seasonally typical fashion

- ADP private payrolls, initial claims are unlikely to matter to nonfarm

- US trade deficit widened

- US ISM-services expected to signal continued growth, watch jobs and prices

- US vehicle sales will slightly dent retail sales

- Negara held, sounded done

- Inflation readings from Sweden, Switzerland, Thailand didn’t sway markets

- Chinese equities hit by the state’s anti-speculation measures

- Australian trade is holding up well—so far

- Florida and Harvard grads

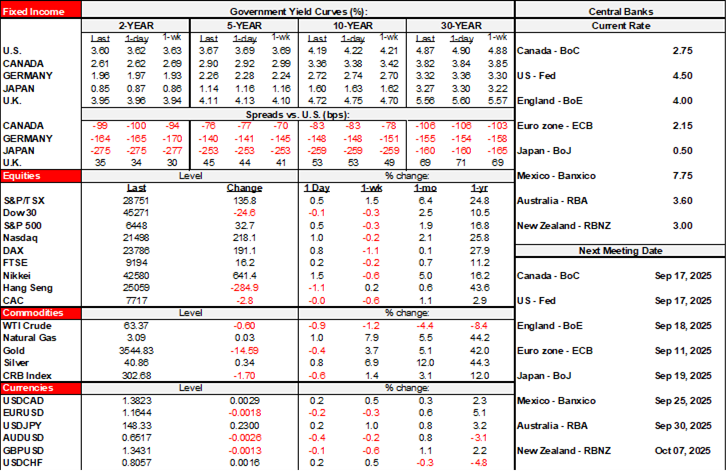

Now it starts to get more interesting. While a series of US readings is bound to spark volatility this morning, key is that markets are bracing for a dovish nonfarm print tomorrow. Fed funds futures are priced for a cut on the 17th, about half of another in October, and by December lean toward 50–75bps of cumulative cut pricing. It could swing in either direction after nonfarm. Sovereign bonds are catching a bid across the board this morning and so are most equity benchmarks outside of France. China was an exception where equities fell by 1–2% after the state indicated it would lean against speculation after the recent rally with measures like easier short selling rules.

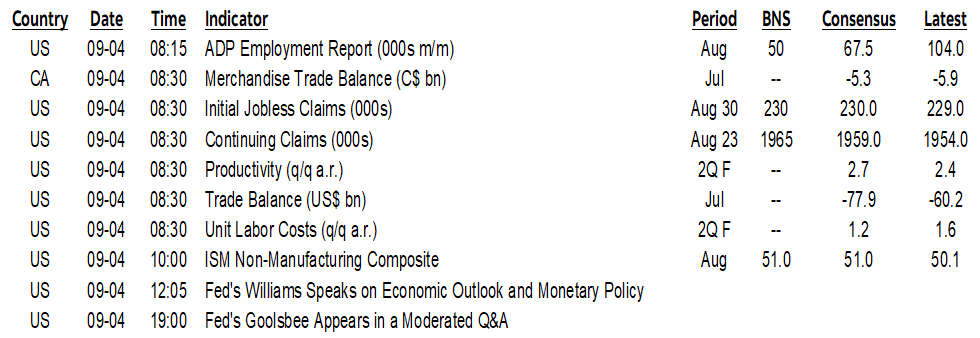

Most of the focus will be upon the U.S. of A this morning as warm-up acts will arrive before the big show tomorrow. Here’s the lowdown on what to expect:

- Challenger job cuts climbed in August to about 86k which is the highest since May. They had fallen back to the 50–60k/mth range over the prior couple of months which is neither here nor there by way of key nonfarm implications. There is seasonality in this series over recent years that front–loads layoffs at the beginning of the year and then ebbs with this year behaving no differently in that regard (chart 1). Only a blow out number would have possibly been of any consequence, but even then, the connection to tomorrow’s nonfarm is likely to be tenuous given how layoff packages work.

- Next up is ADP private payrolls in August (8:15amET). Yawn. They’ve been weak for several months now with July’s 104k gain the highest since March but not high. It’s a poor gauge for purposes of predicting nonfarm but I’ll not the historical odds relative to nonfarm expectations after we get the number (chart 2).

- initial jobless claims follow 15 minutes later. We’re outside of the August nonfarm reference period with this print and so it’s likely to be faded. Initial claims backed up slightly in August’s reference period which is the pay period including the 12th of each month depending on pay frequency, but not by enough to really matter.

- The trade balance for July is unlikely to contain material new information (8:30amET). We already know the merchandise component that widened by about US$18 billion to a deficit of $104B and the services surplus that gets tacked on today is usually very stable.

- Then it’s ISM-services time with August’s reading (10amET). Most expect a slight improvement, but it’s prone to surprise. Aside from anecdotes, keys will be employment that has been in contraction of late despite what services payrolls say, and prices paid that have been on a strong upward trend to the highest since late 2022 as memories of past challenges resurface.

- Then Stephen Miran’s grilling before the Senate begins just as ISM hits (watch here). Frankly, this is what could be the most interesting thing this morning in my opinion. He asks you to believe that he’d respect Fed independence. Meadow muffins! I can picture the wolf in grandma’s gown when he says it. Miran is a dyed in the wool MAGA adherent who is part of Trump's plan to stack the Fed and undermine all institutions in your choice of populist or authoritarian fashion—or why choose. Expect aggressive grilling and aggressive pushback in his testimony tomorrow that will probably wind up simply rubber stamping his candidacy in time for the Sept 17th FOMC decision.

Also note that late yesterday’s US vehicle sales landed on the screws at 16.07 million SAAR, matching consensus and Scotia’s estimate but the range was 15.8 to 16.4. US vehicle sales fell by -2.1% m/m SA which in weighted terms will shave about ¼% off of August retail sales all else equal.

And last, we have developments in the labour market from the state where apparently science education has some work to do. Hello polio, we missed you. Measles too. HPV—isn't that a tv channel? Tetanus is a planet, right? Oh come on, mumps can't be that bad. What's a little diphtheria among friends. Walk it off, it'll all only make you stronger. I’m speaking of course in reference to the supposed ‘doctor’ who violated his profession’s duty to provide leadership in caring for people by taking steps to eliminate vaccine mandates for children in the state of Florida. What’s the matter with Harvard grads anyway? Not only the state’s surgeon general, but the crazies who graduate with PhDs in economics from Harvard and go on to undermine democracy with protectionist beliefs that 99% of economists would reject; looking at you, Miran, and you too, Navarro. Over-lettered and lacking common sense. Anyway, aside from the fact that the health of children—who can’t vote—will be placed at risk for years to come, the cold hard reality in terms of the economics is that if such measures gain popularity, then workforce absenteeism is likely to be higher in future, healthcare spending is likely to go up, corporate profits will likely suffer, and progress toward eliminating such scourges is likely to be reversed. What these people fail to realize is that the externalities of putting whole populations at risk trumps the reticence to embrace science at the individual level among a minority of folks. What a shame.

OVERNIGHT CENTRAL BANK DEVELOPMENTS

Riksbank watchers got a bland inflation report for August that didn’t do much to local markets. Swedish CPI slipped by -0.4% m/m as expected and underlying inflation was -0.2% (-0.3% consensus). Market pricing for the September 23rd decision remains at about -10bps but rises toward two-thirds of a cut priced by Nov/Dec in keeping with guidance offered on August 20th about “some probability of a further interest rate cut this year.”

Swiss CPI remained very soft at -0.1% m/m NSA and 0% y/y with core at just 0.7% y/y. Markets continue to expect the SNB to remain on hold later this month and by year-end.

Thai markets shook off core CPI that held at 0.8% y/y as expected with headline at -0.8% y/y.

Bank Negara Malaysia held its overnight rate at 2.75% as widely expected. After easing in July for the first time since the pandemic, the central bank indicated it was done by saying it “considers the monetary policy stance to be appropriate and supportive of the economy and price stability.”

Trade down under is holding up well. Australia’s exports surged by another 3% m/m in July after a 6.3% prior gain, while imports fell 1.3% after a smaller revised dip of 1.5% in June. The nominal trade balance moved to its highest since early 2024.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.