ON DECK FOR MONDAY, SEPTEMBER 15

KEY POINTS:

- Markets in a positive mood to kick off a packed week

- China’s economy put in a mixed performance in August

- Canadian home resales post fourth monthly gain…

- …as interest sensitive readings keep gaining

- Canadian manufacturing and wholesale posted sharp gains

- US quiet with just Empire on tap

- Global Week Ahead — You’re Gonna Need More Coffee! (reminder here)

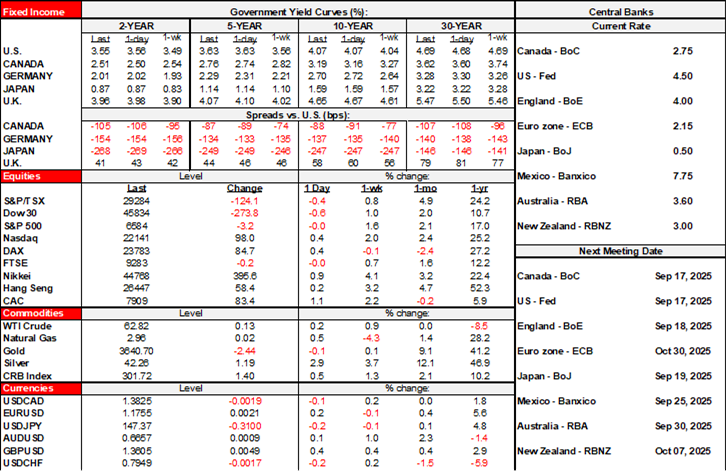

A fresh week that will be stacked with central bank decisions and global data is kicking off with a handful of releases out of China and Canada. The dollar is broadly weaker. European sovereign bonds are outperforming US Ts. Stocks are in the black with N.A. equity futures slightly positive and European cash markets outperforming.

MIXED CHINESE DATA

China released several readings for the month of August. Some were better than the headlines in my view because they emphasized base effect driven slow downs in y/y readings that dominate newswire coverage instead of month-over-month gains. Other readings extended their weakening trends.

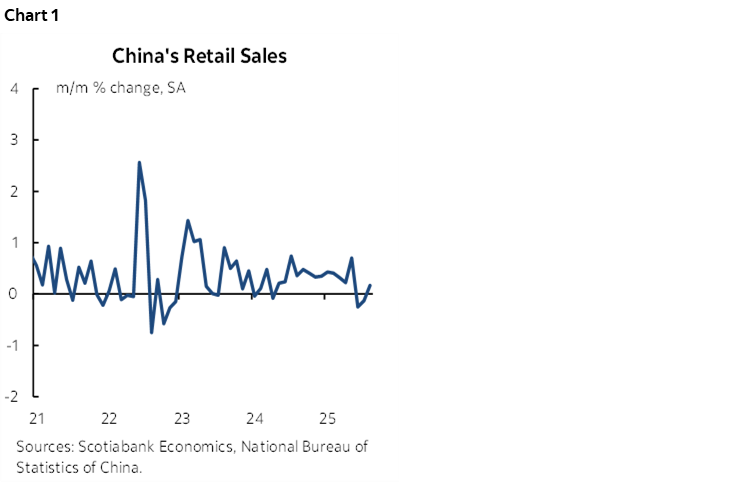

- Retail sales were up by 0.17% m/m SA in August and rebounded from the prior -0.1% reading (chart 1). Base effects drove the y/y rate lower to 3.4% (3.7% prior).

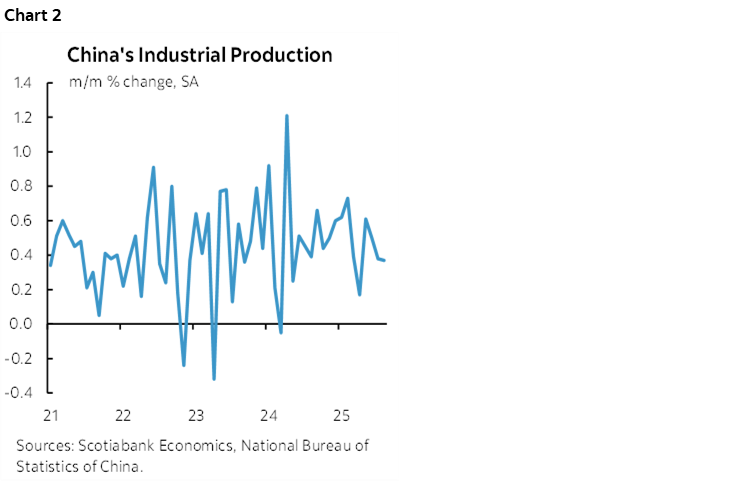

- Industrial output climbed 0.37% m/m SA for a second month in a row and has been growing at a relatively rapid pace for several months (chart 2). Base effects drove a weaker y/y reading to 5.2% (5.7% prior).

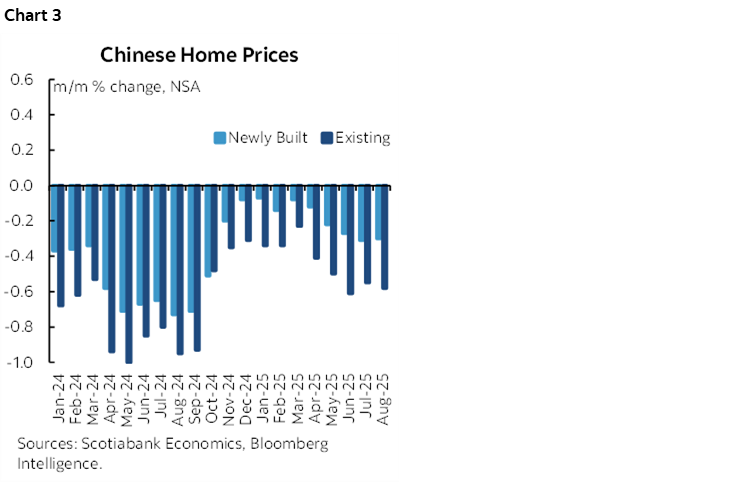

- Home prices continue to slide (chart 3). New home prices fell 0.3% m/m SA for the twenty-seventh month in a row and resale prices fell 0.6% m/m SA for the twenty-eighth monthly decline in a row. Rate cuts can’t help property markets given a lack of confidence and expectations of further capital losses.

- China’s jobless rate ticked up to 5.3%.

- Fixed investment fell for a third straight month (-0.2% m/m SA).

CANADA’S HOME SALES KEEP ON GAINING

We have more evidence of traction on the interest sensitives in Canada in lagging response to rate cuts.

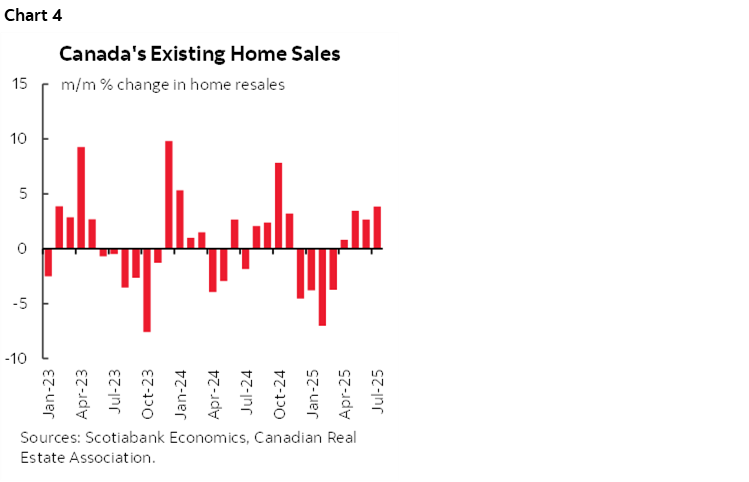

Canada registered a fourth consecutive monthly gain in seasonally adjusted existing home sales during August (+1.1% m/m SA). Chart 4. New listings were up 2.6% m/m SA. The sales to new listings ratio fell to 51.2%. Months supply fell to 4.4 for the lowest since January and remains below the long-term average of about 5.0 months which places the market roughly in balanced territory. Prices were little changed (-0.1% m/m SA) but down 3.4% y/y.

CANADA TO REFRESH MINOR MACRO GAUGES

Canada refreshes some minor data for July this morning. We already have advance guidance from Statcan pointing to strong gains in manufacturing sales and wholesale sales and revisions plus details like volumes will round out the picture (8:30amET).

QUIET IN THE US

There is nothing meaningful on tap in the US today, just the first of the regional manufacturing surveys when the Empire gauge arrives (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.