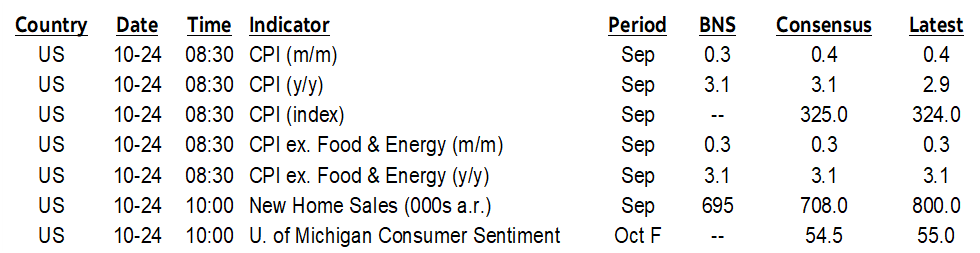

ON DECK FOR FRIDAY, OCTOBER 24

KEY POINTS:

- Global markets await US CPI

- US core inflation is expected to be firm

- Why markets are shaking off Trump’s termination of US-Canada trade talks…

- …and why Ontario’s ad hit a raw nerve

- PMIs: Quicker growth in Europe, unchanged to slightly cooler in Asia-Pacific…

- …with the US on tap

- UK consumers continue to spend

- Japanese core CPI was flat, BoJ unlikely to rush a hike

- Russia’s central bank cuts by half what was expected

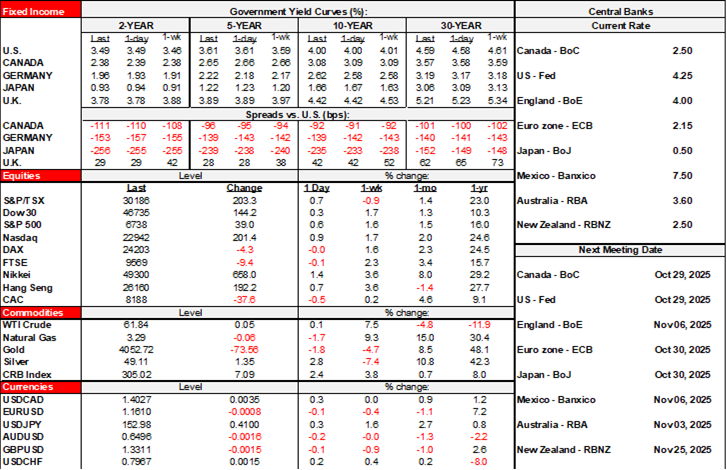

Global asset classes are generally staying close to home as they await US CPI. Sovereign bond yields are slightly higher across the Eurozone partly because of better-than-expected PMIs. Stocks are little changed on balance with S&P futures up a bit, TSX futures flat, and European cash markets little changed. The dollar is broadly firmer.

KEEP CALM TOWARD CANADA-US TRADE TALKS

There is little market reaction to Trump’s social media post that trade talks with Canada have been terminated. CAD has depreciated by about ¼% since the announcement. TSX futures are flat and hence only slightly underperforming US equity futures. The Canadian 2-year yield is down by 1–2bps this morning versus flat US 2s. Big. Whoop.

Here is Trump’s post. Here is the Ronald Reagan Foundation’s ‘X’ post that lashed out at Ontario’s ads. Here is former President Reagan’s full radio address from 1987 that was featured in the Ontario government’s ad campaign. Judge for yourself.

Ontario’s ad is not ‘fake’ as Trump claims and the Reagan Foundation is wrong to have lashed out about the use of a publicly available radio address. If Reagan were alive, he may well disapprove of the post by whomever is running his foundation. Ontario’s ad is based exactly on what Reagan said. Reagan was clear that a very specific trade dispute with Japan over semiconductors was not the tip of the iceberg for broader protectionism. Reagan went on to rail against protectionism and the general use of tariffs while expressing strong support for free trade including with Canada. Besides, even if the Ontario government ad misrepresented Reagan’s views—which it didn’t—then Mr. Trump is expressing a sudden aversion to bending the truth.

The funny irony here is that in the wake of Trump’s post, now the whole world knows what Reagan said about tariffs as opposed to this just being targeted ads by the Ontario government. Premier Ford got under Trump’s skin and now the world knows what one of the most respected Republican Presidents would have thought of Trump’s trade wars. Today’s Republican party is unfamiliar relative to its past.

Why a muted reaction? Maybe markets finally get that President Trump is an overly emotional, erratic and impulsive President. What he says one day can flip around soon afterward. Markets might also understand this as a diversionary tactic from the fact Senators split town yesterday and hence gave up trying to end the Trump administration’s government shutdown. Regardless, what was revealed was perhaps the Trump administration’s heightened sensitivity toward possibly losing the Supreme Court’s coming review of Trump’s tariff powers in a couple of weeks.

US CPI IS FINALLY COMING

The Bureau of Labor Statistics releases CPI for the month of September this morning (8:30amET). Despite the ongoing government shutdown, the BLS is taking the step of calling back employees to put out the numbers because of the requirement that Q3 CPI must be known for purposes of setting cost of living adjustments for benefits over the coming year.

The release will also help to inform expectations for the Fed’s preferred PCE gauges that don’t arrive until October 31st and hence after the FOMC decision on the 29th. The producer price gauges are unlikely to be released before the 29th to help complete the PCE picture unless the shutdown ends soon.

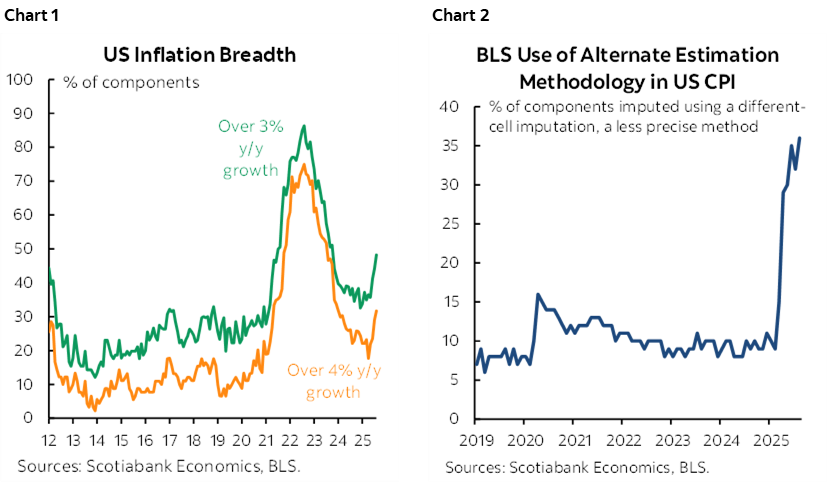

I won’t repeat earlier analysis that was provided back here. Scotia’s house estimates are for increases of 0.3% m/m SA for both total CPI and core CPI excluding food and energy. Consensus is at 0.4% for headline and 0.3% for core. Watch the breadth of price increases which has been on the rise again (chart 1). The imputed share of the basket that is estimated through alternative means might stay high in light of budget cuts which would continue to dent data quality (chart 2).

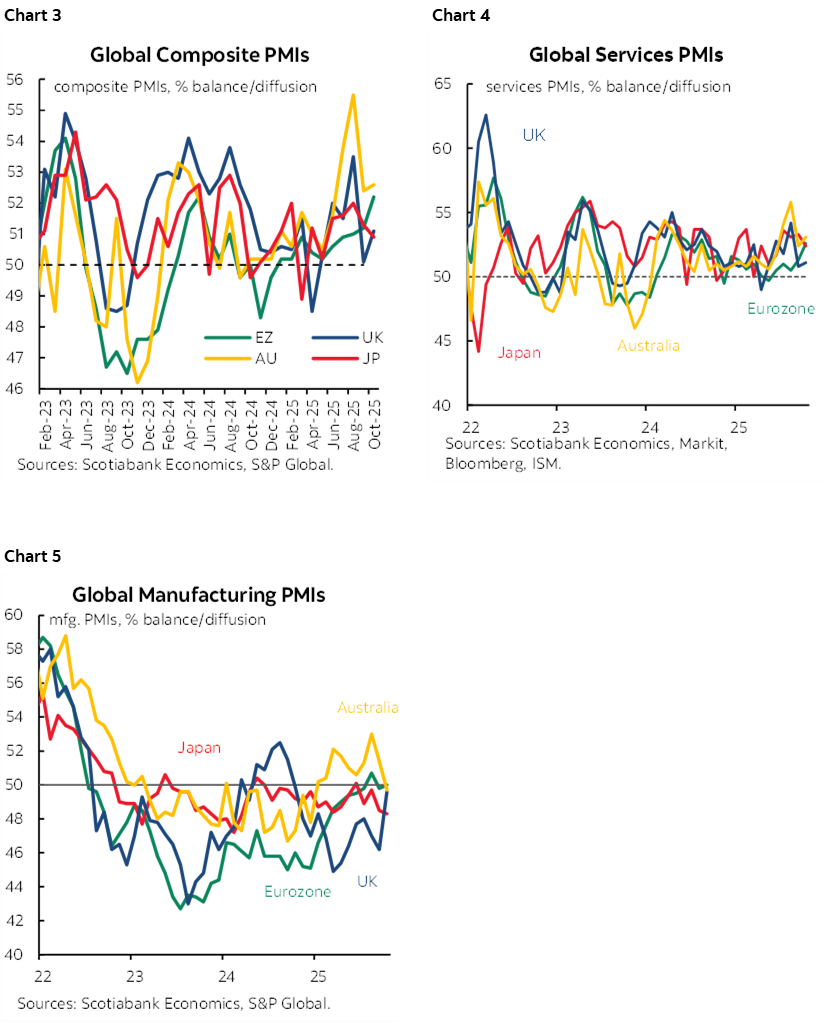

GLOBAL PMIS—FASTER GROWTH IN EUROPE

Updated global purchasing managers’ indices were collectively a touch more encouraging. Growth accelerated in Europe with Asia-Pacific PMIs indicating either little change or a slight deceleration. Charts 3, 4, and 5 show the readings.

- the Eurozone composite PMI accelerated (52.2, 51.2 prior) because growth in services picked up while manufacturing is neither expanding nor contracting.

- the UK composite PMI accelerated by a full point to post mild growth (51.1) primarily as manufacturing’s pace of decline ebbed (49.6, 46.2 prior) and services were little changed while still posting mild growth.

- Japan’s composite PMI slipped four-tenths to 50.9 which signals barely any growth. The deceleration was almost entirely driven by slower growth in services as manufacturing remains in mild contraction.

- Australia’s composite PMI was statistically unchanged (52.6, 52.4 prior) as services accelerated a touch by manufacturing slipped into mild contraction

- India’s composite PMI slowed by 1.1 points to a still robust pace of growth (59.9). Services cooled to a still rapid pace of growth while manufacturing accelerated.

- the US will update its S&P PMIs this morning (9:45amET).

OTHER DEVELOPMENTS

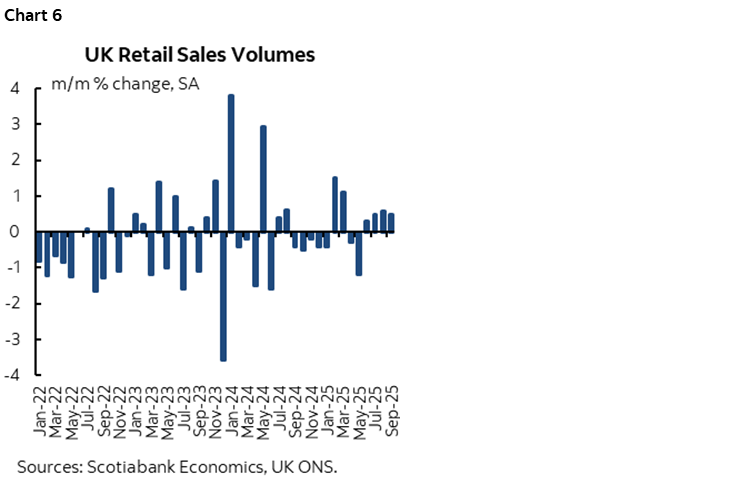

UK consumers were feeling a little friskier than expected last month. Retail sales expanded by 0.5% m/m SA against consensus expectations for a -0.4% drop and the prior month was revised a touch higher (0.6% from 0.5%). Sales ex-gas were even firmer (0.6% m/m, consensus -0.6%, prior 1% up from 0.8%). The trend remains firm (chart 6).

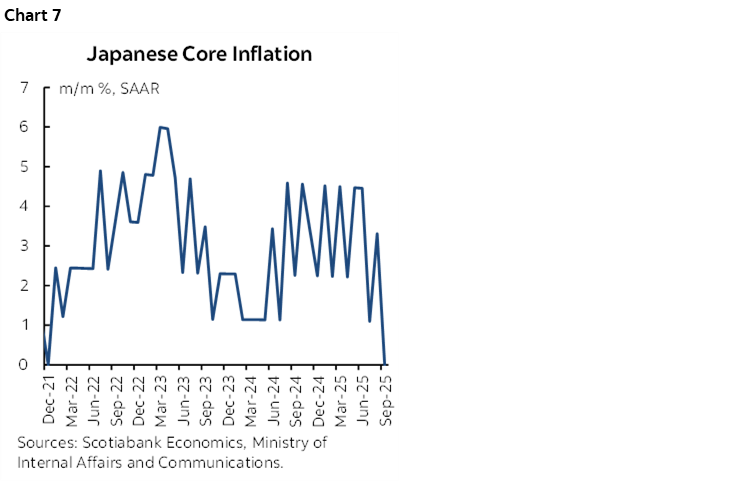

Japanese core CPI was flat in m/m seasonally adjusted and annualized terms during September. It’s just one data point, but it’s a sudden deceleration to the weakest reading since December 2021 (chart 7). Core inflation has slowed on a three-month moving average basis. There was no real market reaction despite the BoJ’s prior guidance that it “will hike when the outlook matches our forecast.” Markets retained pricing for no change by the BoJ next week and half a cut in December while JGBs were unchanged and the yen did not immediately react on a generally firm day for the dollar.

Russia’s central bank cut its key rate by 50bps to 16.5% which was half of what consensus expected.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.