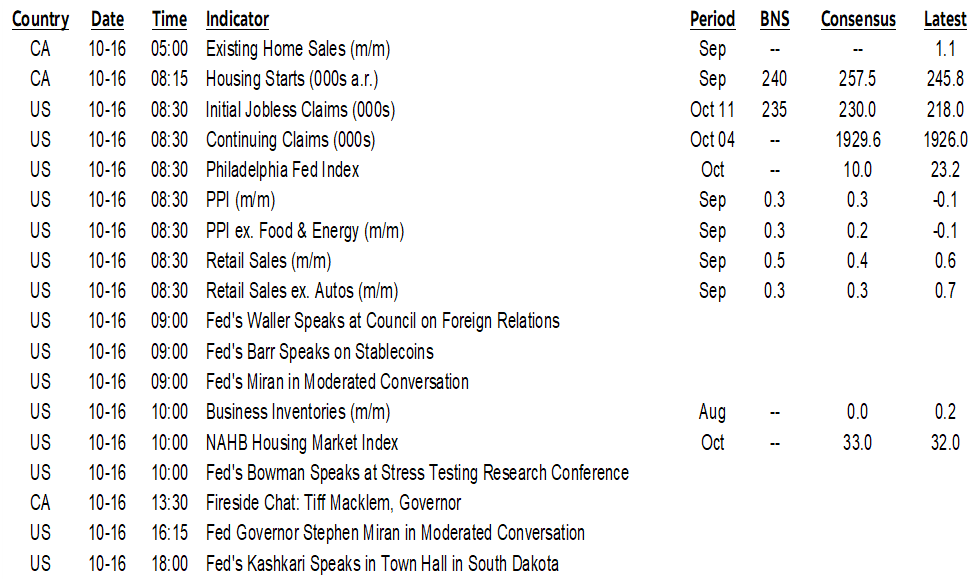

ON DECK FOR THURSDAY, OCTOBER 16

KEY POINTS:

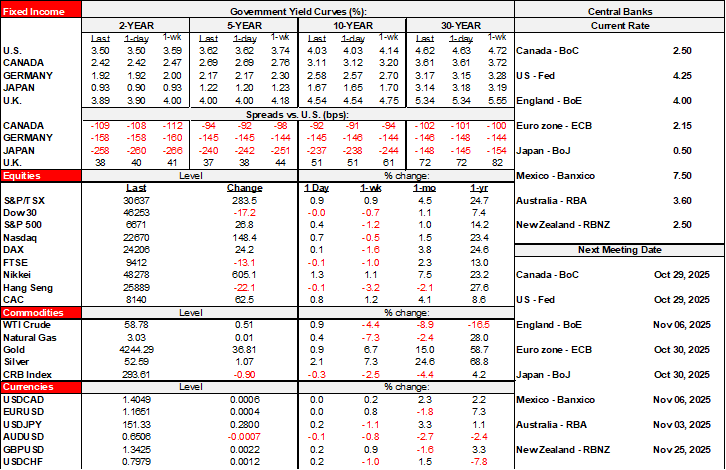

- Mixed asset classes absent major developments

- BoC’s Macklem enters the lion’s den

- Canadian home sales halt gains at least temporarily

- Canadian business inflation expectations move lower. So did hiring sentiment.

- Aussie bonds outperform after soft jobs…

- …as RBA cut pricing doubles

- Mixed signals on the health of the UK economy

- Bleak signals for Japanese capex

- Mounting shutdown toll on US macro data

Mild risk-on sentiment is driving equities gently higher across N.A. futures and European cash markets except for London. Australian government bonds are outperforming post-jobs in an otherwise dull global sovereign debt space. The dollar is little changed as slight gains by some crosses are offset by slight underperformance by the A$ and yen.

BoC’s Macklem, UK and Aussie macro data, and light data from the US and Canada are the main drivers today as global earnings continue to roll in.

BOC’S MACKLEM TO SPEAK BEFORE BLACKOUT

BoC Governor Macklem takes the fight to Washington—epicenter of misguided trade policies that are damaging the Canadian, global and US economies. He’ll speak at the Peterson Institute for International Economics in a moderated session starting at 1:30pmET. No published remarks are expected. No press conference is scheduled. There will be audience Q&A. There will be a webcast available off the PIE website and I think Bloomberg will also run a feed.

What should we expect from Macklem? Jobs rebounded, but the trend is weak. GDP growth is weak and spare capacity continues to build. Will he opt to hold until he sees the budget? Is he committed to meaningful insurance stimulus which one extra 25bps cut is not? Might he intimate we’re at the fine-tuning stage for monetary policy adjustments which can merit insertion of buzz words like ‘gradual’, or Poloz’s line from 2015 that policy adjustments at such a stage don’t need to go back-to-back in a straight line while there is merit to keeping some powder dry? I’d like to hear from him and then see next week’s batch of inflation readings.

Another possible topic may be financial regulations in Canada. As written in my weekly, Ottawa is dragging its feet compared to other jurisdictions when it comes to open banking, real time payments systems, and stablecoin and therefore holding back innovation in Canada especially in fintech. What else is new, Canada waits for the US and other jurisdictions to act on everything from vaccines to finregs before it maybe acts in lagging fashion.

CANADIAN HOME SALES BREAK THE STREAK, SMALL BUSINESSES SEND MIXED SIGNALS

The Bank of Canada’s Business Outlook Survey arrives on Monday but we already have solid reason to expect it to show a mild further decline in inflation expectations. The CFIB’s measure of inflation expectations in its business confidence survey was updated this morning and serves as a timelier monthly leading indicator for the BoC’s quarterly measure. Chart 1 shows the connection. Still, inflation expectations in the short-term remain moderately higher than the 2% inflation target. The BoC’s consumer survey will also be watched on Monday for any progress on what are still high inflation expectations among consumers.

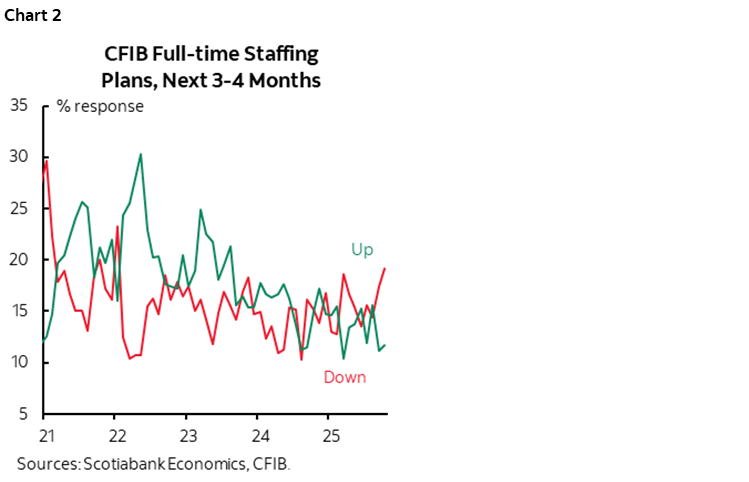

Also note that small business plans to downsize employment climbed to their highest since October 2021 (chart 2).

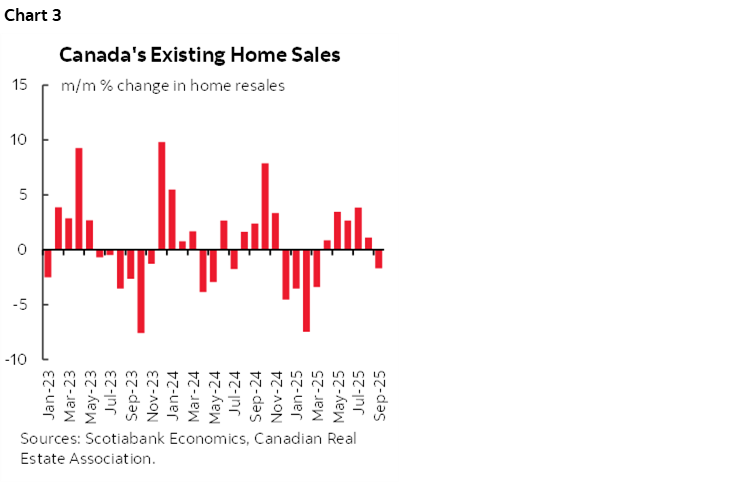

Canada’s stretch of four monthly increases in existing home sales came to at least a temporary end in September (chart 3). Sales fell by 1.7% m/m SA. The sales to new listings ratio fell to 50.7% from 51.2% previously which remains in balanced territory. Months supply was unchanged at 4.4. Repeat sale home prices were little changed (-0.1% m/m SA).

Housing starts in September (8:15amET) will inform whether the four-month surge over April through July that stumbled a bit in August are on a new, softer trend.

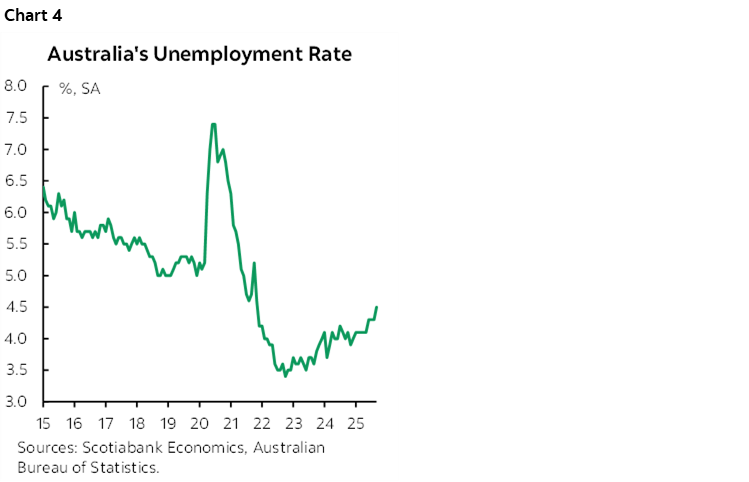

AUSTRALIA’S JOB MARKET IS PLODDING ALONG

Aussie jobs boosted bets that the RBA may cut at its next decision on November 4th. Those odds doubled to about a two-thirds chance at a 25bps cut. Australian 2s rallied by 9bps overnight in a bull steepener and the A$ is among the weakest performers this morning.

Australia gained about 15k jobs last month which was around the 20k consensus especially considering the statistical noise factor. However, the gain was marred by a downward revision 12k prior loss. Since April, Australia has only gained about 38k jobs for an average monthly gain of just over 7k. The unemployment rate moved up to 4.5% from an upwardly revised 4.3% the prior month (was 4.2%) and it is 1.1 points higher than the trough in 2022 (chart 4).

CONFLICTING SIGNALS ON THE HEALTH OF THE UK ECONOMY

The UK economy generally met expectations for August’s readings. GDP grew 0.1% m/m SA, matching consensus. Industrial output doubled consensus expectations (0.4%) but services were unexpectedly flat and construction shrank -0.3% m/m with downward revisions. Exports fell by 1.2% m/m and imports also slipped (-0.7%) as trade with the EU was the main source of weakness.

FALLING DEMAND FOR JAPANESE MACHINES

Japanese core machinery and tool orders fell -0.9% m/m SA in August against expectations for a mild rebound from the 44.6% prior decline. They’ve fallen in three of the past four months. Machine tool orders are often treated as a leading indicator for capex.

LIST OF SUSPENDED US DATA RELEASES KEEPS GROWING

The list of suspended US data releases will continue to grow today. We should be getting retail sales, PPI and claims, but won’t. Only homebuilder confidence in October is due out including model home foot traffic as a leading indicator of new home sales (10amET).

The biggest US banks are out of the way as earnings season continues. KeyCorp—in which Scotiabank holds about a 15% stake—beat expectations with EPS of US$0.41 (consensus $0.38).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.