ON DECK FOR TUESDAY, OCTOBER 14

KEY POINTS:

- Risk-off sentiment has three drivers

- Volatile US-China trade tensions escalate again

- Markets not so impressed by strong US bank earnings

- Chair Powell to speak

- UK jobs and wages drive lower yields

- US policies hit small business confidence who turn sour on the economy

- Global Week Ahead — Shutdown Upside (reminder here)

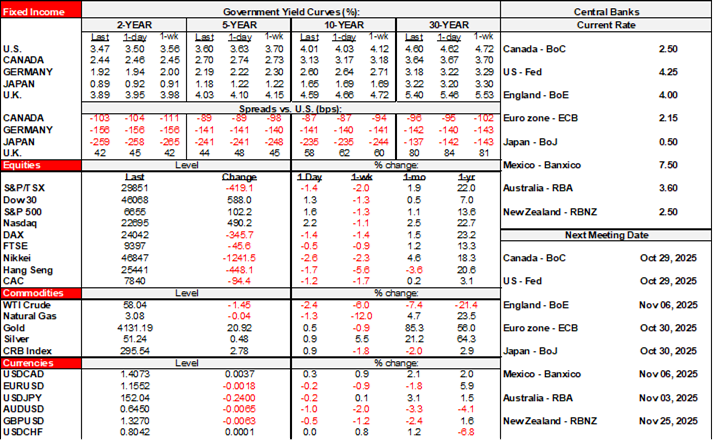

Trade tensions and apprehension ahead of the start of the earnings season for major US banks and a speech by Fed Chair Powell are dominating global markets. Stocks are mildly lower with S&P futures down by over 1%, TSX futures slightly lower (-0.1%) as Canada catches up from Thanksgiving, and European benchmarks are ½% to 1½% lower. Sovereign bond yields are broadly lower and led by gilts (jobs, see below). Oil is off by over 2%. The dollar and yen are leading the way on safe haven demand.

US-CHINA TRADE TENSIONS FLARE

China-US trade tensions have been seesawing since late last week. China applied sanctions overnight on the US units of South Korea's Hanwha Ocean Co, a shipping company. Hanwha is alleged to have helped US trade investigations into the shipping industry, including China's. Watch for Trump's response given his erratic behaviour since Friday when he said an added 100% tariff on Chinese imports would be imposed but then backed down on Sunday. Frankly, China is the lone economic power with the backbone to stand up to Trump's trade wars with no apparent off ramp.

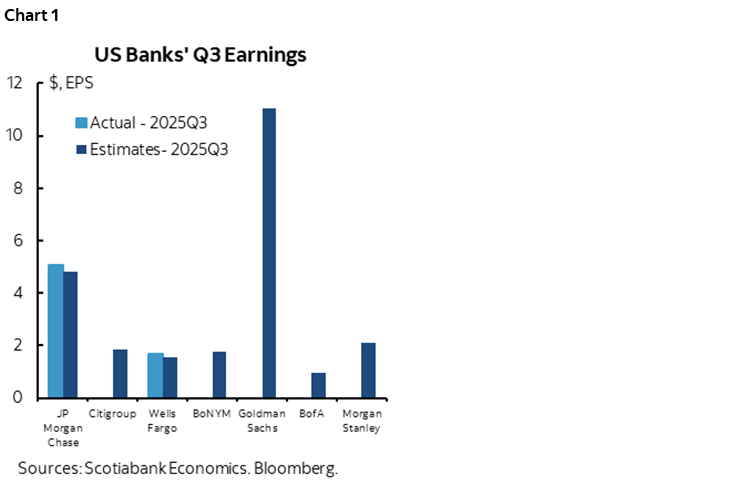

US BANK EARNINGS — NOT ENOUGH, SO FAR

Earnings from JP Morgan, Goldman, Citi, and Wells Fargo are arriving in today's pre-market from about 6:30–8amET. JP Morgan beat with EPS of US$5.07 (consensus $4.83) alongside revenue beats across trading segments and an ROE of 17%. Wells Fargo’s EPS was US$1.66 (consensus $1.55) and also beat on revenues with ytd ROE of 15%. GS and Citi are pending. Chart 1.

As an aside, I’ve seen folks comparing Canadian bank ROEs to US bank ROEs by cooking the books including the thousands of tiny US local banks. Compare big Canadian banks to big US banks and Canadian banks are generally on par with US banks or earn lower ROEs. In any event, there are many drivers of ROE differences across firms.

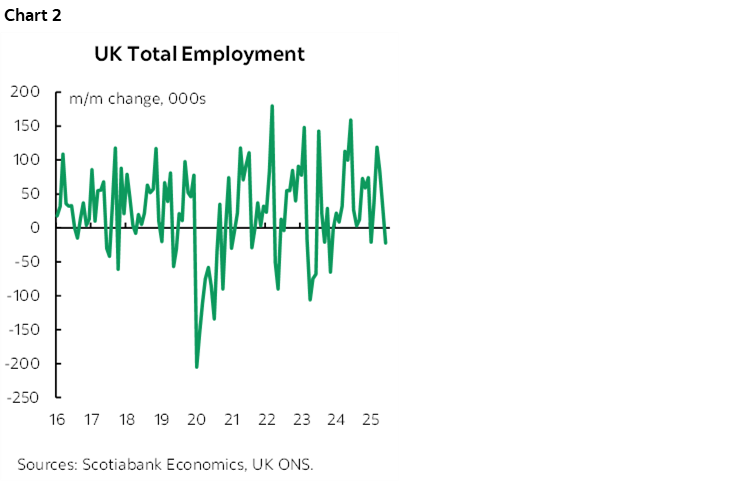

UK JOB MARKET COOLING

UK growth in jobs and employment abated last month. The result is combining with global trade tensions to drive outperformance of gilts that are richer by about 6bps across the curve. Here’s the rundown:

- total employment slipped by 22k in August (chart 2). This follows a string of four consecutive gains. 358,000 total jobs have been gained year-to-date with off-payroll, smaller businesses leading.

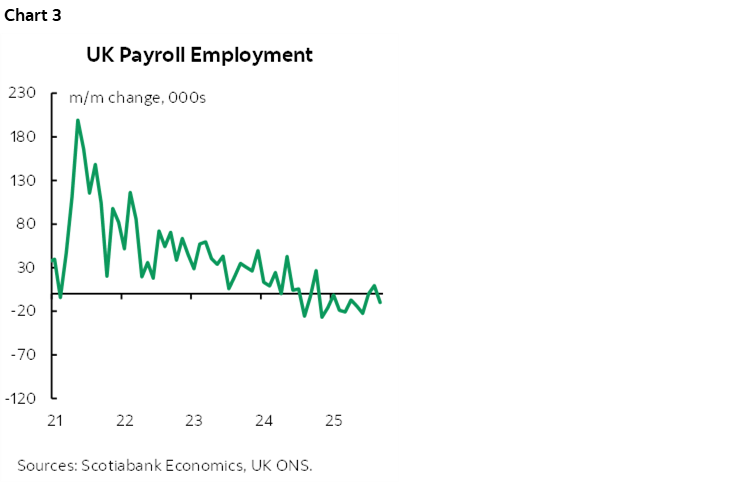

- fresher payroll employment renewed declines with 9.8k lost jobs in September for the first drop since June. 84,000 payroll jobs have been lost so far this year. Chart 3.

- Job vacancies fell to 717k in September (-11k). They remain slightly above the long-run average but have been on a downward trend since April 2022.

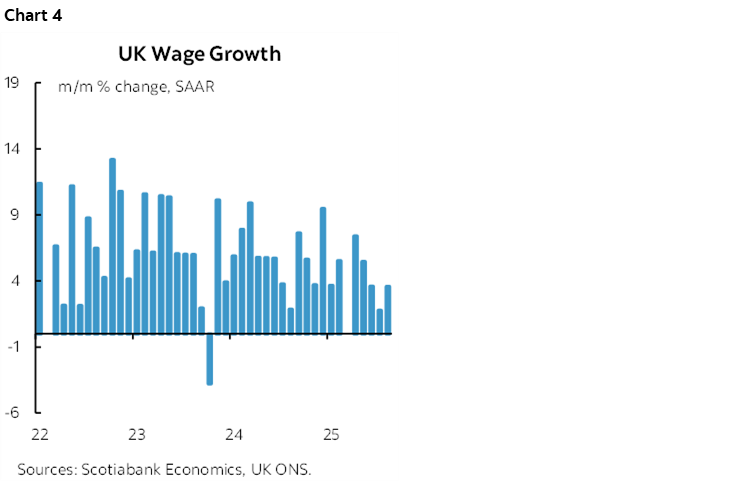

- wage growth picked up a bit to 3.6% m/m SAAR in August. The three-month moving average sits at 3% m/m SAAR in a noticeable cooling of pressures compared to much of the rest of the post-pandemic period. Chart 4.

FED CHAIR POWELL TO SPEAK

Chair Powell speaks at a NABE conference over lunch followed by a moderated discussion (11:30amET-1:10pmET).

See my weekly for previews of the bank earnings season and Powell's speech.

US POLICIES HIT SMALL BUSINESS CONFIDENCE

US NFIB small business confidence slipped in September (98.8 from 100.8). Plans to hire slightly improved but only 16% of firms indicated such plans. Price expectations moved up and the share of small businesses expecting a better economy fell by 11 points to 23% with only 11% saying now was a good time to expand. There is no other data due out into the N.A. open.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.