ON DECK FOR WEDNESDAY, NOVEMBER 5

KEY POINTS:

- Markets treading water, CAD and GoC’s shake off federal Budget

- Yes Canada’s Budget fell short of the hype…

- ...but here’s why I’m ok with that

- US ADP private payrolls expected to register a mild gain

- US ISM-services expected to post slight growth

- Four votes favoured Dems over Trump

- US Supreme Court IEEPA tariffs review commences today, could take months

- US Treasury refunding announcement is unlikely to surprise

- Riksbank held as expected

- European factory data beat expectations

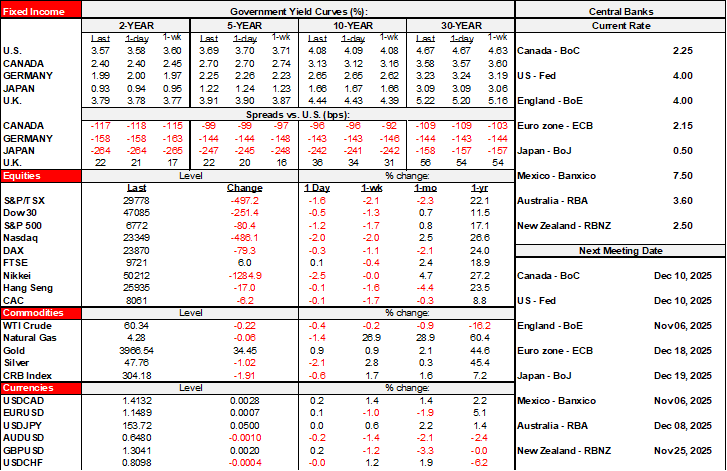

Global asset classes are mostly treading water this morning. Sovereign bond yields are mostly little changed, ditto for equities that have a slightly negative bias on balance, and the dollar is split against major crosses. CAD is minimally affected by the budget with only a third of a cent depreciation perhaps because the budget fell shy of some of the hype, while the Canadian sovereign yield curve is largely flat this morning.

CANADA’S BUDGET FELL SHORT—AND I’M OK WITH THAT!

On balance I’m ok with the Budget. Sure, there was more hype and sloganeering in advance that didn’t quite translate into the actual plans, but I’m ok with that. I would’ve liked to have seen more emphasis upon tax reform and regulatory reform. But what I’m focused upon is the big picture and the high level signals provided in this budget. For details, please see Rebekah Young’s piece. My thoughts follow.

The Budget largely ended the pattern of rushing to stimulate here-today-gone-tomorrow consumption with transfers and other stimulus supports that then gave way to a vacuum with nothing sustainable to show for it beyond more Amazon orders. It’s about time, as a very high share of Canadian GDP (87%) goes toward short-term spending which is the highest since 1979. The country never wants to take a step back from this model of pouncing on soft patches for consumption in favour of a program designed to raise living standards over time. Hands are always out and that comes at the expense of longer-run planning, investment and productivity. Ergo declining living standards.

Further, our base case macro view—and that of the private sector consensus used by Finance—isn’t great, but it doesn’t scream out a need for emergency short-term measures especially if the supply side of the economy is also getting hit. Don’t make the same mistakes all over again by overstimulating demand amid a supply shock. For that, the government deserves credit.

Further, given that Trump is in a snit and his next moves are as unpredictable as his prior moves, it may be wise for Carney to have held off on larger measures now. Don’t run the well dry.

Perhaps most important is that the Budget didn’t fail to preserve future optionality as I had feared it might by really blowing out deficits and debt. If things go south to a greater extent, there is room to revisit.

The strong message in this Budget, however, is that it is willing to allow a period of adjustment to occur rather than blocking resource reallocations by putting band-aids all over everything. I still think that part of Canada’s productivity problem is that we held on to overly large stimulus supports for too long coming out of the pandemic and prevented more efficient resource reallocations of labour and capital.

I also like tossing the ball back to the private sector to take advantage of investment incentives. If you don’t invest now, then you have no right to whine about productivity. Now rise to the occasion, Corporate Canada! Tax accountants are less than impressed by the budget it seems, but they should be doing their jobs advising companies to seize the moment here. Further, I’m generally not a fan of government driving massive state-directed investments; there is clearly some in here, but at least for now it is held somewhat in check to areas where government is more like to have a role.

Then again, I’m not running for office or in a political office. It remains to be seen whether Canadians are open to coming off the methadone the previous administration hooked them on. The NDP is on the fence, the Conservatives are sulking in opposition saying they won’t support, and it sounds like the BQ won’t support the budget. I would expect it to pass with adjustments by doing what’s needed to get a couple more votes to add to the Libs’ 170 seats after a turncoat crossed the aisle.

Other points include the following:

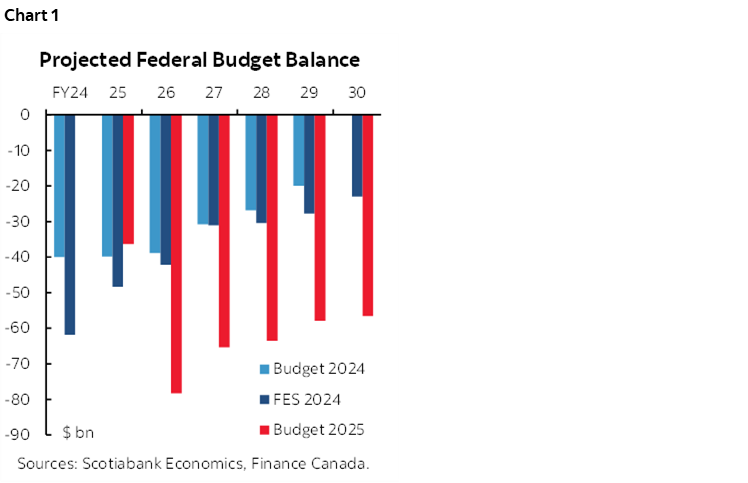

- the deficits could have easily been bigger and uglier (chart 1). As a share of GDP, they peak in the 2½%-ish percentage range and then fall back a bit. If the economy is worse than expected, the ratio is likely to rise further but probably temporarily. Remember that the fear was we could see them top $100B and stay higher for longer than proposed. That could have put borrowing costs at risk and fed rolling sovereign debt shocks that the market is not indicating as a risk this morning.

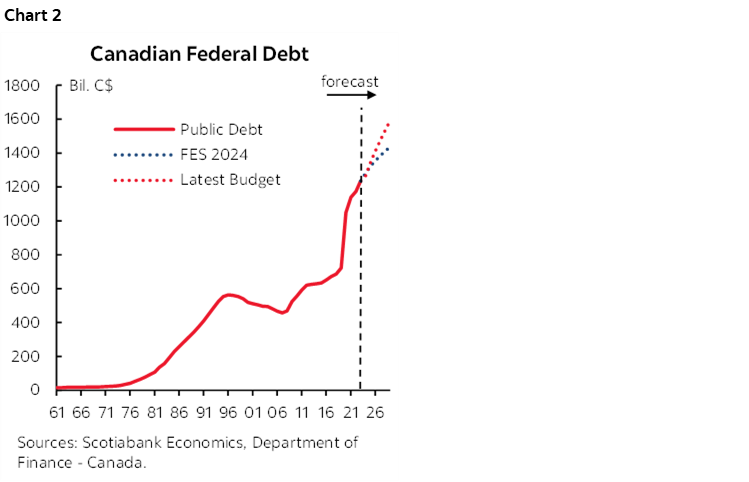

- the debt-to-gdp ratio doesn’t explode. It’s higher in nominal dollar terms (chart 2) but as a share of GDP it cruises in the low 40s percentage wise.

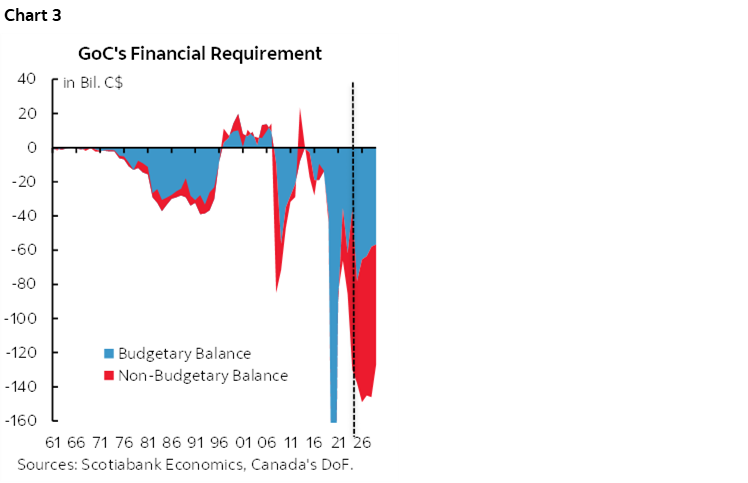

- Chart 3 shows the surge of financing requirements. It was already expected to be high and driven by both on- and off-budget requirements. Much of it reflects allowing deficits to adjust automatically to weakness versus really slamming on the brakes, and much of the rest reflects inducements.

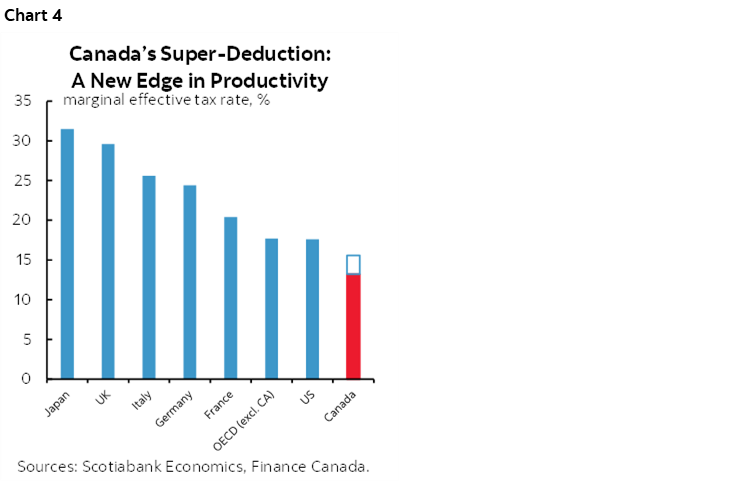

- For example, the Budget hands the ball to companies to invest or shut up about productivity. I prefer corporate tax reductions that are delivered with a carrot approach; use investment incentives, rather than here’s your tax cut and go pay it out to shareholders with nothing else to show. The super-deduction—if seized—restores some tax competitiveness (chart 4).

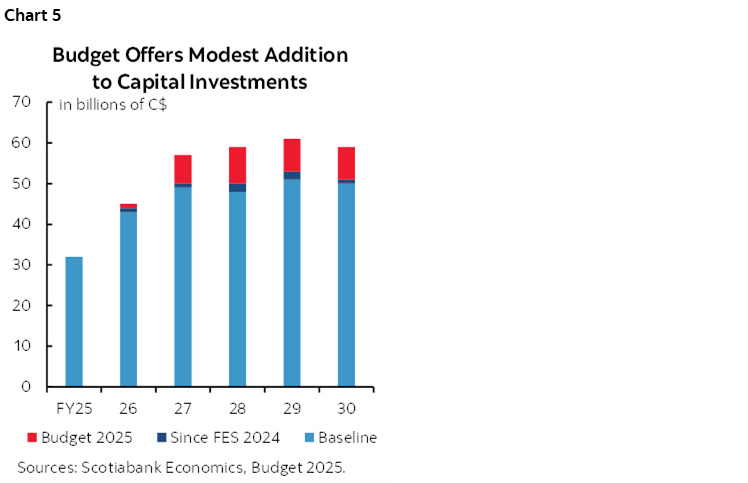

- Chart 5 shows that while capital investments rose, they didn’t blow the lights out compared to what was already in the plans. More of the emphasis in the budget is upon providing inducements to invest rather than state-directed investments though there is some of that and the government would argue it’s needed.

- program spending grinds to a halt in nominal terms (0.5% per year) and shrinks in real terms but without cutting the large number of social programs that the Trudeau administration introduced (childcare, dental care, pharmacare etc). They could free up more for investment.

- the growth-sucking oil and gas emission caps are gone. I’d rather have a democracy like Canada supplying the world than some of the despots and miscreants in other countries who profit from the energy business.

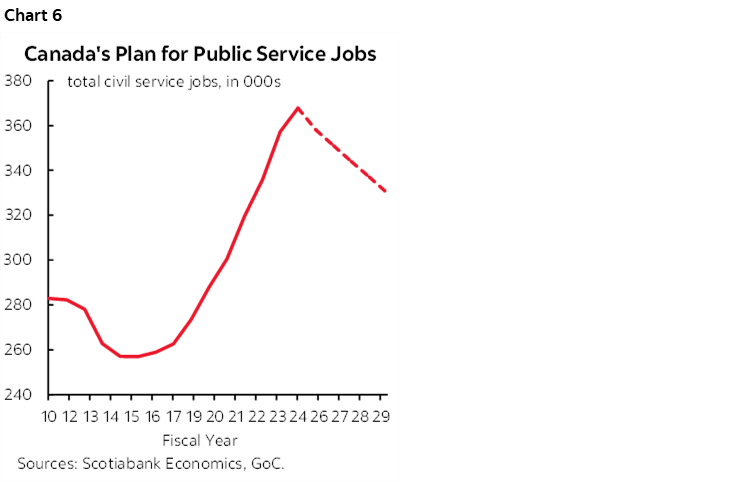

- curtailing the number of civil servants is long overdue (chart 6). If anything, they could have gone further in my opinion and freed up more folks to address years of labour shortages in the private sector, assuming there is a match. It’s a bloated, inefficient and productivity-sapping workforce.

- the Budget got rid of silly taxes that were administratively complex, costly to collect and to comply with, and petty, like the tax on “luxury” vehicles, boats and planes, and the tax on “underused” housing. These were purely performative stunts by the old regime.

- it capitalizes on the misguided US steps to impose a US$100k/yr fee on H1-B visa applications for highly skilled workers by offering increased funding for attracting and retaining talent. C$1.7B will be spent on recruitment of 1,000 “highly qualified international researchers.”

- personal taxes did not go up. Hey, let’s celebrate small victories. They didn’t go down either except for the previously announced measures for the lower income tax bracket and how that trickles through in limited fashion to higher income brackets.

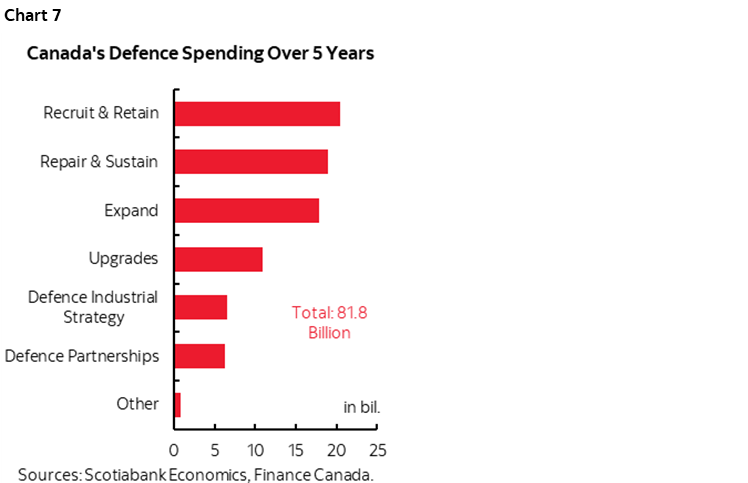

- defence spending goes up, but mostly on salaries and training over the five years (chart 7). If subs and planes are to be bought, then it’s likely to appear later. C$30B increase over 5 years. Outside of the budget horizon would be the rest of the 5% of NGDP target by 2035, or plans change. And wow, of the C$84B in extra defence spending over the next five years, one quarter will be spent on pay hikes and recruiting for members of the armed forces plus $19B to fix air force infrastructure, $10.9B on digital infrastructure and cyberdefence, and $1.9 billion goes to armoured vehicles, drones, long-range strike capabilities whatever exactly that means. Ok, so this one’s mixed, since I don’t see enough to retool the pathetic state of Canada’s armed forces.

- I like the one-liner hint at privatizing airports. Possibly. Maybe. Nothing by way of plans. But it’s a step in the right direction to free up public capital for other purposes and maybe even drive more efficient management of the assets.

- Curtailing the temps category of immigration is also welcome (chart 9). Canada overshot on this category which carried its own costs, while permanent residents offer more leveraged growth opportunities over time.

- I’m even ok with seeking efficiencies at Statcan given guidance that the "frequency of data collection will be reduced where the requirements can be met through statistical modelling or other modern methods. Collectively, these measures will ensure that the agency remains sustainable and focused on delivering the most critical and relevant data for Canadians." Focus on the priorities and ditch some of the fluffy stuff.

- a vague stablecoin step is outlined: “Budget 2025 also announces the government’s intention to introduce legislation to regulate the issuance of fiat-backed stablecoins in Canada. This legislation will require issuers to maintain and manage adequate asset reserves, establish redemption policies, implement risk management frameworks, and protect the sensitive and personal information of Canadians. The legislation will also include national security safeguards to support the integrity of the framework so that fiat-backed stablecoins are safe and secure for consumers and businesses to use. To administer the relevant legislation, the Bank of Canada will retain $10 million over two years, starting in 2026–27, from its remittances to the Consolidated Revenue Fund. Administrative costs in subsequent years are projected to be $5 million per year and will be offset from stablecoin issuers regulated under the Act. Related amendments to the Retail Payment Activities Act will also be made to enable the regulation of payment service providers that carry out payment functions using prescribed stablecoins."

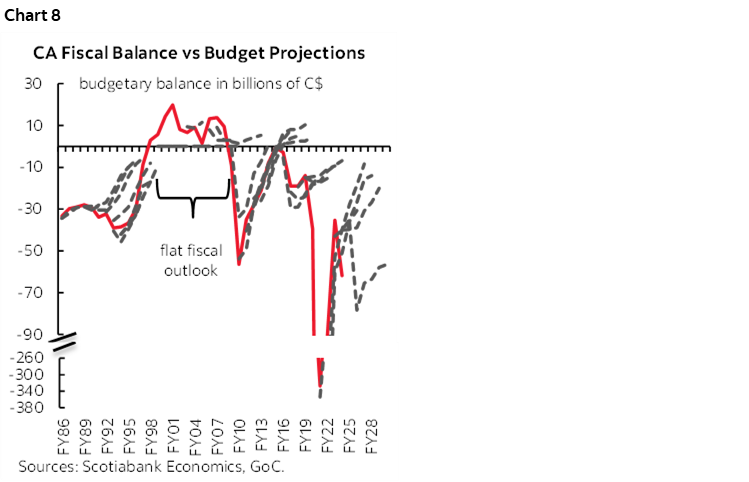

Overall, recall the concern going into this. It was a Budget that could have thrown caution to the wind and ramped up more debt than it did and for a longer period. That may still actually be in the PM’s mind over time given that rolling out large cap-ex and defence plans takes years. If so, then be cautious toward this set of numbers. They could still be a fairy tale given a) Ottawa’s pathetic track record at forecasting budgetary balances (chart 8) and b) given the potential future policy bias that may heap on large further spending over the next several years and beyond the projection period when we get into the horizons of big ticket projects and expensive toys for the armed forces. There is definitely a risk of a Trojan horse impact on the budget in future, but there is also the opposite risk that things could turn out better for the Canadian economy than feared over time. Lagging pass through of rate cuts, some fiscal supports, lagging spending by the past surge of new arrivals, the lowest effective tariff rate of any of America’s trading partners, and CAD’s flexible shock absorber adjustments could be accompanied by a future release of pent-up demand with trade negotiations hanging in the balance.

TRUMP HAD A TERRIBLE ELECTION NIGHT…

Trump had a terrible night as all his horses fell out of the running in a pretty clear repudiation of his leadership while perhaps putting a significant part of his real estate empire at risk. The results nevertheless fan my concern that his extreme policies could motivate an extreme pivot in the other direction.

Mamdani smoked Cuomo in NYC's mayoral contest with 50.4% of the tabulated vote versus 41.6% (here). Even combining the weak showing by the Republican candidate (Curtis Sliwa) who got 7.1% with Cuomo would have still handed Mamdani the win.

The Dems won both Governor spots in Virginia with a margin of 577.5% to 42.3% (here) and NJ by a margin of 56.2% to 43.2% (here).

The icing on the cake was California's redistricting vote that passed with about 64% support (here) and is estimated to flip about five more Republican seats to Democrats.

…AND IT COULD SOON GET WORSE FOR HIM

The Supreme Court’s hearing into the legality of Trump’s IEEPA tariffs begins at 10amET today. Lower courts that took up the three lawsuits by businesses ruled that his use of the legislation was illegal and violated the intent of the legislation. It’s unclear when a decision will be offered as some point to the Court normally taking months to do so which could stretch it well into 2026, while others think the Court may respect the administration’s desire to treat it more urgently.

As argued in my weekly, a ruling against the administration won’t stop tariffs; it would just remove the quickest and most flexible tool in Trump’s arsenal (see chart 19 here).

US MACRO DATA ON TAP

We’ll get ADP private payrolls for October (8:15amET) and ISM-services for October (10amET) this morning. Both measures are from private groups that are unaffected by the government shutdown.

ADP should post a modest gain given tracking of the weekly figures that they have started to offer back to July. The usual caution applies against any clear implications for nonfarm payrolls whenever they get released. ADP samples only its clients that are skewed toward larger employers and hence under represent smaller payroll firms, exclude government, and has a very different methodology compared to nonfarm. ADP commonly throws off multiple misleading signals.

ISM-services is expected to continue to post mild overall growth, mild growth in new orders, rapidly rising prices, and shrinking employment.

US TREASURY REFUNDING

Treasury market participants will have a keen eye on the 8:30amET Quarterly Refunding Announcement (here). It sets auction sizes and composition. Monday’s marketable borrowing estimates for Q4 were lowered by US$21B to US$569 billion compared to previous guidance while guiding that 2026Q1 would borrow at a similar pace of US$578 billion (here). No one really expects big surprises or deviations from guided issuance and emphasis upon t-bills.

LIGHT OVERNIGHT DEVELOPMENTS

Sweden’s Riksbank held its policy rate unchanged at 1.75% this morning as widely expected and priced. Guidance continued to state that the policy rate is “expected to remain at this level for some time to come.” Guidance also stated that the outlook was not judged to have changed materially from September with fresh forecasts including updated explicit policy rate projections due at the December 18th decision.

German factory orders rebounded sharply by 1.1% m/m in September and the prior month’s -0.8% drop was revised up to a smaller drop of -0.4%.

French industrial output also exceeded expectations at +0.8% m/m in September (0.1% consensus) following the prior month’s -0.9% drop (previously -0.7%). The gain was led by a 0.9% rebound at manufacturers.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.