ON DECK FOR THURSDAY, MARCH 6

KEY POINTS:

- The Trump-inspired global bond sell off continues…

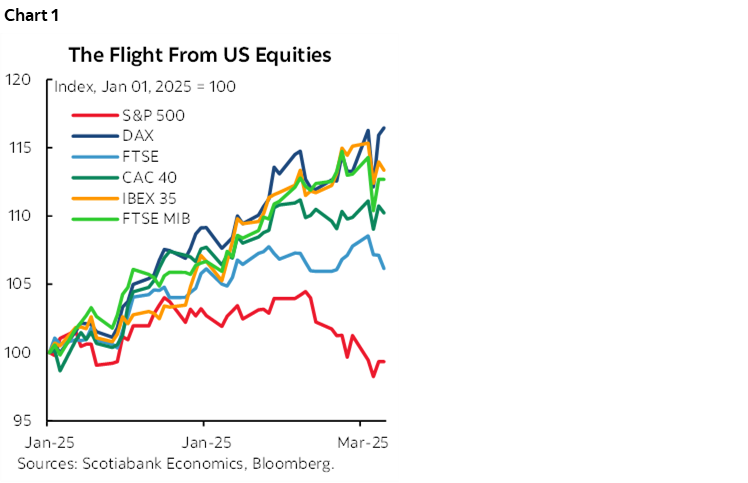

- ...while continuing to drive capital flows out of US equities into Europe

- US fiscal plans are on ice as an extended CR is being pursued

- The ECB’s new quandary: stunning demand-side fiscal expansion

- Canada-US trade negotiations at a stalemate...

- ...and what probably actually happened on yesterday’s Trudeau-Trump call

- Trump is likely to hit the roof again when he sees the full US trade deficit

- Was Q4 strength in Canadian trade pulled forward?

- US mass layoffs and claims on tap

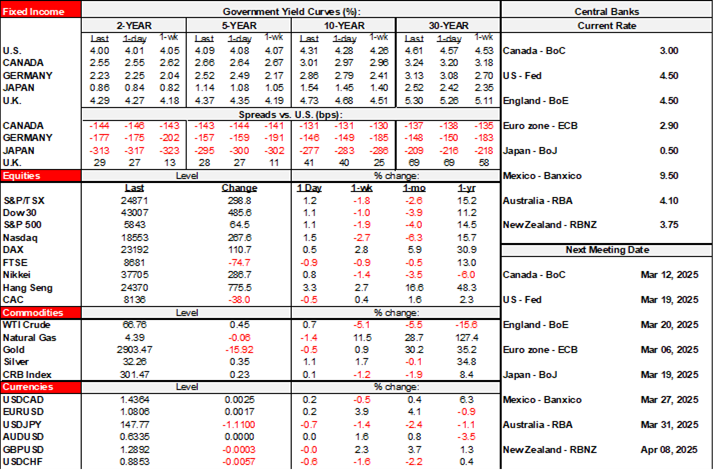

The DJT-inspired global bond sell off is continuing this morning. US isolationism is driving European debt issuance plans skyward to foot the bill for being on its own. On the heels of Germany’s earlier announcements, we have French President Macron leading the charge with talk of a nuclear umbrella into a security summit today that is likely to advance talks to increase spending across the EU. They’re talking trillions of euros and of course recall that nothing ever goes bust when Europe becomes fiscally wreckless! The consequences continue to reverberate throughout world markets. EGBs are selling off again in bear steepener fashion that is lifting the yields on 10s by 6–8bps across benchmarks following yesterday’s massive rise, and with UK yields rising by less. US Ts and Canadian government bonds are also bear steepening, but by less than EGBs. Asia-Pacific markets got hit by carry influences themselves as yields ‘down under’ rose by double digits overnight and 10-year JGBs are 10bps cheaper. Give global bond PMs a hug today, or at least a free coffee.

The impact on equities continues to be one of capital flight from US equities into European and Asian benchmarks that has been going throughout this year so far. Trump is making equity investors relatively richer—in Europe (chart 1). This morning, however, it is characterized by less selling pressure on European exchanges than in US equity futures, with exceptions being further gains in Germany and Italy. Asia-Pacific markets rallied with equities broadly higher in China, Japan, South Korea and India. The reasons this is happening include a) relatively improved European growth prospects due to fiscal injections, and b) profound US policy uncertainty that is harming growth prospects across N.A. Recession risk is real in the US and for the first time in many years we’re looking at portfolio rebalancing effects that are challenging the US economy’s relative supremacy—and that of its stock market.

THE US IS PREPARING FOR AN EXTENDED TUSSLE OVER FISCAL PLANS

On the latter point, US fiscal policy plans are on ice for now. Hence why the Trump administration is now pushing for a continuing resolution to fund the government beyond next week’s March 14th deadline until the end of the fiscal year on September 30th. The bill would extend funding at present levels that have continued to rise despite limited DOGE efforts. A shutdown driven by GOP dysfunction is probably unlikely when they hold the (slim) majorities in both chambers, but the symbolism is stark and they can’t lose many House Freedom Caucus votes that are typically opposed to stopgaps. The main message here is that they think they’ll need that much time to negotiate the terms of a fiscal arrangement within a highly divided GOP and subject to the deficit constraints of the budget reconciliation process as Musk’s chainsaw runs out of wood.

LIGHT OVERNIGHT DEVELOPMENTS

Overnight calendar-based developments were light. Riksbank-watchers were not thrilled about a CPI overshoot on headline and core CPI that has Sweden’s rates curve underperforming all others while markets see the central bank on hold for the foreseeable future. Bank Negara Malaysia held its policy rate at 3% as expected. South Korean inflation undershot expectations for headline and core and the won is underperforming. Turkey’s central bank cut its one-week repo rate by 250bps as expected.

THE ECB IS IN A QUANDARY

The ECB will be the main event with an expected 25bps cut (8:15amET) followed by President Lagarde’s press conference (8:45amET). Massive fiscal expansion in Germany and the prospect of more to come across the EU that could stretch into the trillions of spending stimulus has resulted in full year rate cut pricing being shaved by a full quarter point to just under 75bps of cuts through to year-end including today’s. That may remain too much. I suspect Lagarde may be much more guarded in light of the implications of fiscal expansion, weakening fiscal guardrails like Germany’s debt brake, the bond market effects, and the tariff threat. Most of the planned spending is demand stimulus that does little to nothing for the supply side. Markets are sterilizing some of the fiscal expansion, but how its effects combine with potential tariffs to shape the inflation outlook is uncertain. Nothing ever goes wrong when Europe spends dollops of money on its war machine and abandons any pretense to fiscal prudence.

TRUMP WILL HUFF AND PUFF ABOUT THIS

The US trade deficit is expected to widen from $98.4 billion to -$129B which mostly reflects the deterioration on the goods side (8:30amET). Watch for angry outbursts from you-know-who and who still doesn’t get what’s driving it, or chooses not to in order to suit other political purposes.

US-CANADIAN TRADE NEGOTIATIONS ONGOING

Canada-US trade negotiations will be ongoing, but I remain skeptical that we’ll see material traction. There was no progress after hours. The collapse of the auto sector has been postponed or avoided, but the two sides are probably at an impasse.

LIGHT US, CANADIAN DATA ON TAP

We’ll also get US mass layoffs data for February (7:30amET) and weekly claims (8:30amET) that will help to understand whether the prior week’s rise was an aberration, or the start of a weakening led by fired federal civil service workers.

Canada updates trade figures for January after the strong Q4 numbers (8:30amET). At issue is whether the Q4 strength was pulled forward at the expense of Q1.

And if all that isn’t enough, then brace yourself for tomorrow when US and Canadian jobs arrive along with Chair Powell’s speech on the outlook just before going into blackout.

WHAT REALLY HAPPENED ON THE TRUDEAU-TRUMP CALL?!

What really happened on yesterday’s call between Canadian Prime Minister Trudeau and US President Trump accompanied by Vance and Lutnick? Only the folks on that call or directly briefed may know the truth, but I suspect there is a version of what happened that starkly differs from the one Trump conveyed afterward. Recall that Trump said this afterward:

“Justin Trudeau, of Canada, called me to ask what could be done about Tariffs. I told him that many people have died from Fentanyl that came through the Borders of Canada and Mexico, and nothing has convinced me that it has stopped. He said that it’s gotten better, but I said, “That’s not good enough.” The call ended in a “somewhat” friendly manner! He was unable to tell me when the Canadian Election is taking place, which made me curious, like, what’s going on here? I then realized he is trying to use this issue to stay in power. Good luck Justin!”

Regular readers—or anyone who has followed the issue even casually—know that this isn’t about fentanyl. The hint at overtly interfering in Canada’s election is stunning, but not surprising for Trump or, for that matter, the behaviour of US administrations in various countries over time. And we don’t know when the election will be either; it could be called as soon as next week for April, or perhaps May based on the best info we have to date.

But the version of what happened that I think is likely closer to the truth is that Trump et al were sent packing. Canada’s stance is that it won’t negotiate a de-escalation of tariffs for as long as any US tariffs remain in place. That’s the correct approach in my view and it reflects poorly upon US negotiating skills. The US administration keeps dangling the threat of more tariffs on April 2nd and so why would Canada reverse its retaliatory measures now? The US has only offered a 30-day suspension of auto tariffs, which it had to do in order to avoid almost immediate plant closures rippling across N.A. There is loose US talk of possibly suspending or exemption a few agricultural tariffs, like potash, since hitting fertilizer prices would slam Trump’s agrarian base into Spring plantings and cause crop yields to plummet and food prices to soar. If Canada were to relax some measures, then there are zero assurances that the US wouldn’t keep theirs or increase the tariffs and other antagonistic measures. This is not a US administration that is even remotely trusted in Ottawa.

Canada’s stance has to be to dig in. To not accept any US tariffs. To take the hit up front in order to avoid ruining the economy for the long-term and to avoid being pushed into a bad agreement for many years or decades. This is the lesson Trump should have learned in dealing with Canada the last time into the 2018 CUSMA deal. The newbies in the rest of his administration should perhaps go back and review the lessons of that period.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.