| ON DECK FOR TUESDAY, MAY 14 |

KEY POINTS:

- Markets await the start of US inflation readings

- US producer prices offer a warm up to tomorrow’s CPI

- Fed’s Powell will be on a low risk panel

- Gilts and sterling looked through jobs and BoE comments…

- …that combined to make a June cut a highly data dependent stretch call

The main focus this week is a pair of US inflation readings starting with today’s US producer prices. Gilts and sterling are doing about what they should in shaking off the aftermath of the updates on UK labour markets and comments by the BoE’s Pill. Sterling is roughly flat so far on the day. UK 2s were holding at cheaper levels following yesterday’s mild sell-off and staying there post-jobs before rallying after Pill’s remarks and then shaking off almost all of that effect as well. I’ll explain why UK markets were right to look through it all in my opinion.

The UK posted better than expected labour market readings. The figures don’t scream out for rate cuts. Here are the takeaways:

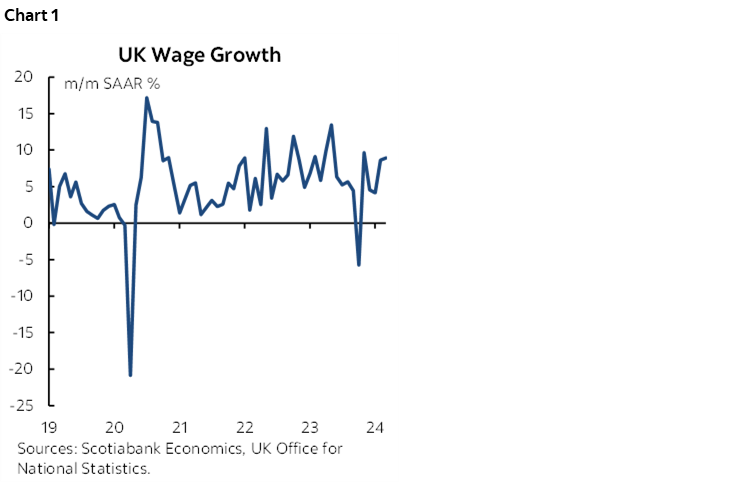

- Wage growth is soaring. Pay ex-bonuses increased by 8.9% m/m SAAR in March, after 8.6% in February (chart 1). Both figures are double the pace of the prior two months. They are far in excess of inflation and poor productivity.

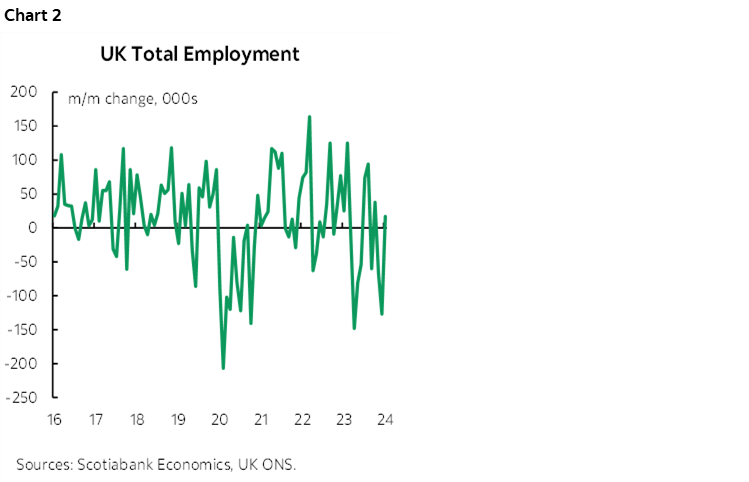

- +17k jobs were created in March’s figures for total employment which contributed to a strong beat to expectations for the 3m/3m change to deteriorate from a loss of 156k to -220k and instead it landed at -178k (chart 2). It’s only the first gain in total employment in three months and one of two gains in the past five months.

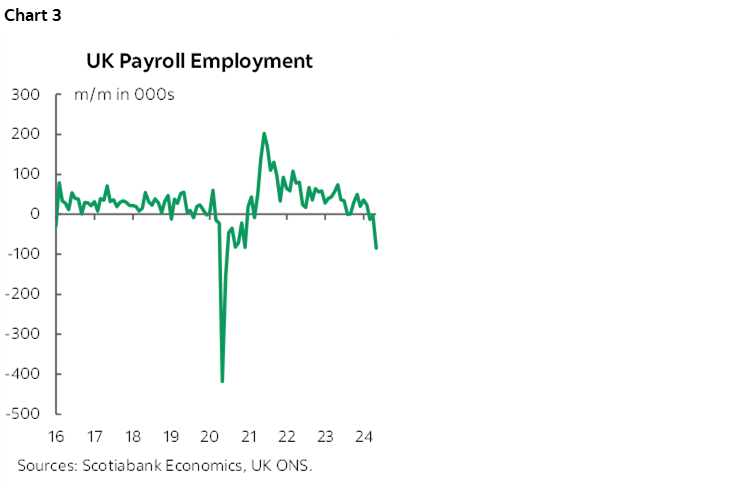

- Payrolls—a timelier subset of total employment—were mixed as they fell by 85k in April, but mainly because the prior month’s 67k drop was revised to just -5k (chart 3).

- The unemployment rate ticked up to 4.3% which is about a half percentage point above the cycle low but still signalling a tight labour market.

As for BoE Chief Economist Hugh Pill’s comments he didn’t sound like there is a rush to cut by the June 20th meeting. Maybe they will, but there is enough reason to note the doubt in his comments. Here’s what he said:

- “It’s not unreasonable to believe that through the summer we will begin to see enough confidence in the decline in persistence that bank rate will come under consideration.” Does he know that summer doesn’t technically start until just hours after the June 20th decision? If so then we’re talking August, not June.

- That said, he did emphasize the next two batches of CPI figures and the next set of employment market readings which makes it sound like he’s very data dependent on the path to June and that it could go either way.

- Pill also noted that there is “some way to go” to bring inflation down and that much of the softening of inflation has been driven by food and energy prices, and that wage gains are “quite well above given developments in productivity, what would be consistent with the 2% inflation target being met on a lasting and sustainable basis.”

I found that Pill’s comment that “we can cut bank rate, while still leaving some restriction in the system,” was on the mark and implied that his bias is toward slow and methodical easing perhaps by contrast to Governor Bailey’s intimation that rate cuts could be delivered quicker than markets think.

US producer prices will offer a warm up to tomorrow’s CPI (8:30amET). Higher energy prices are expected to lift the headline by more than core.

Fed Chair Powell is on a panel this morning (10amET) after PPI but before tomorrow’s CPI. I don’t expect much by way of anything different from him. It’s at an event in the Netherlands with ECB member Klaas Knot. Governor Cook will also speak at 9:10amET.

Nothing material is due out of Canada today, just wholesale trade for March which is expected to drop in nominal terms based on advance guidance (8:30amET). If anything, Canada will be impacted by the start of the US inflation figures.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.