| ON DECK FOR MONDAY, MARCH 18 |

KEY POINTS:

- It’s a light start to an active week

- A recap of this past week's key global macro developments

- Global Week Ahead highlights

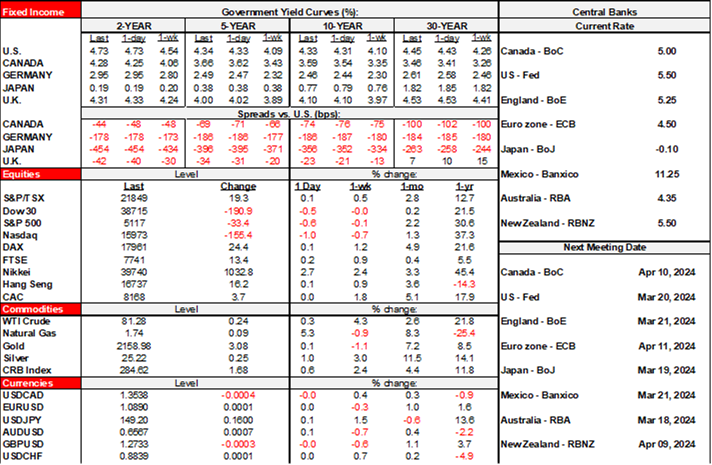

It’s a very quiet start to a packed week. There is a mild risk-on feel with equities gently higher across global exchanges and led by the Nikkei ahead of the BoJ this week. Sovereign yields are little changed and so is the USD with little variation among the major crosses.

China data was mixed overnight. Retail sales were in line with expectations, industrial production beat and so did fixed investment, while the unemployment rate edged up.

Eurozone CPI revisions left the initial prints unchanged for February.

There will be very little into the N.A. session. Canadian existing home sales slipped by 3.1% m/m SA during February and took a breather after two strong months and ahead of the key Spring season. Canadian resale home prices were flat and ended a string of five monthly declines. Canada also updates producer prices for February but they are mostly driven by CAD and commodities and therefore typically contain little new information (8:30amET). The US updates the NAHB homebuilder confidence measure for March (10amET).

The rest of my morning note will recap key observations from the past week when I was away and expectations for this week’s key global developments.

KEY HIGHLIGHTS FROM THE PAST WEEK

Here are my observations on key developments during the past week when I was not publishing. I do them for my own purposes anyway and figured they may be worth sharing as a recap.

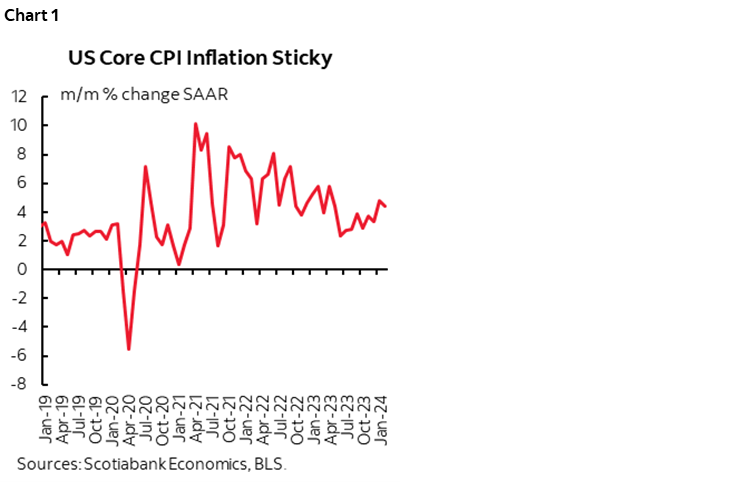

- US core CPI: February’s print surprised higher than expected at 0.4% m/m SA, or 4.4% m/m SAAR. That’s the second consecutive 0.4% print after a pair of 0.3% readings over November and December. Clearly it’s premature to declare victory over inflation as the readings are on an upward trend (chart 1).

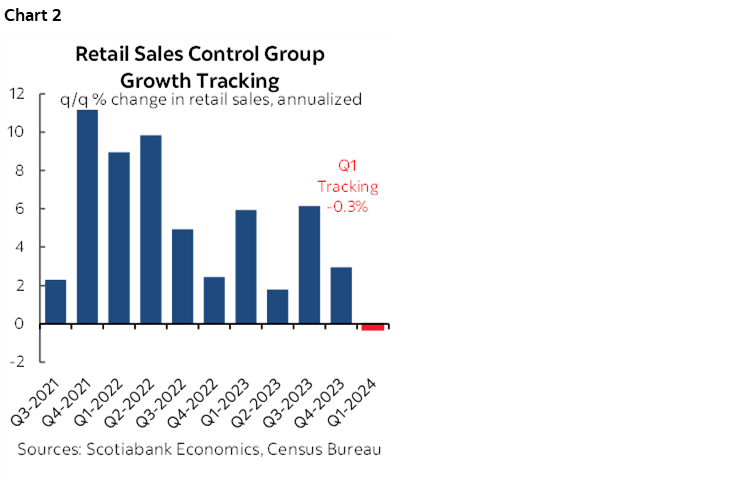

- US retail sales: February’s reading mildly disappointed expectations. Sales were up 0.6% m/m (0.8% consensus) with downward revisions to the prior month (-1.1% instead of -0.8% m/m). The key ‘control group’ that serves as input into total consumption was flat (0.4% consensus). Q1 is tracking a decline in nominal terms so far (chart 2).

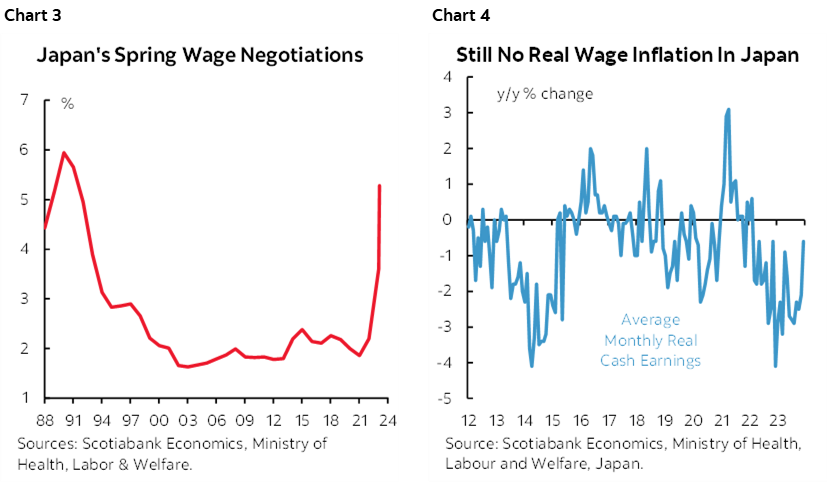

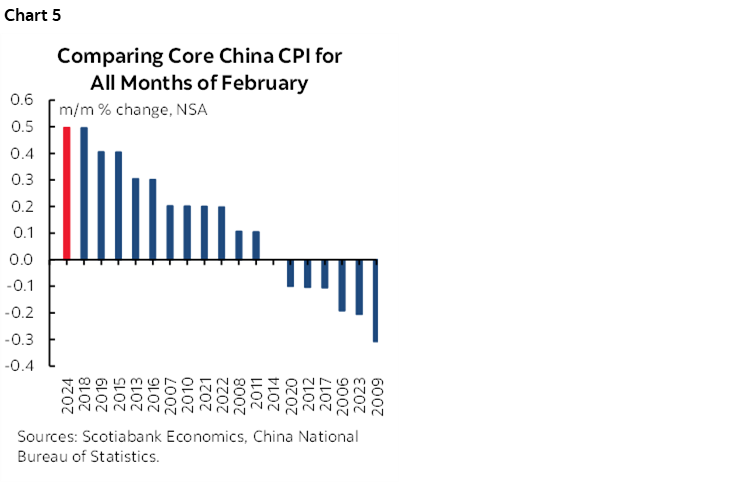

- Japan wages: The annual Shunto round of Spring wage negotiations between unions and large employers resulted in a preliminary estimate of a 5.3% wage gain when the figures were released on Friday. They arrived before this week’s BoJ decision (see below). This gain follows the 3.8% rise last year and makes for the strongest back-to-back gains since the early 1990s (chart 3). The challenges that remain include Rengo’s negotiations only affect less than a fifth of the workforce and that wage gains are not yet moving through the broader economy in real terms (chart 4).

- Chinese fake 'deflation' is over: Inflation figures for February were released just before the start of last week and provided cover for the PBOC to hold. CPI was up 0.7% y/y (0.3% consensus). Core CPI in month-over-month seasonally unadjusted terms was tied for the strongest month of February on record (chart 5). China was never in true deflation defined as a sustained decline in a broad array of prices that was expected to persist and alter behaviour. The casual definition of declining y/y headline CPI was distorted by base effects and narrow drivers, and we now have significant m/m momentum in core prices. What is happening is basically in line with what I’ve previously argued (here).

- The PBOC held: China’s central bank met most forecasters’ expectations by holding its key 1-year Medium-Term Lending Facility Rate unchanged at 2.5% on Thursday. A minority expected a cut that made no sense.

- Expansionary Canadian provincial budgets: Two more of the larger provinces conformed to my expectations that bloat in government spending would intensify and further complicate challenges facing the Bank of Canada. Quebec and Alberta added spending and you can read recaps here and here. BC kicked off the season with an expansionary budget on February 22nd. Other than that, Canada was very quiet but posted beats in housing starts and wholesale sales and a miss in manufacturing sales.

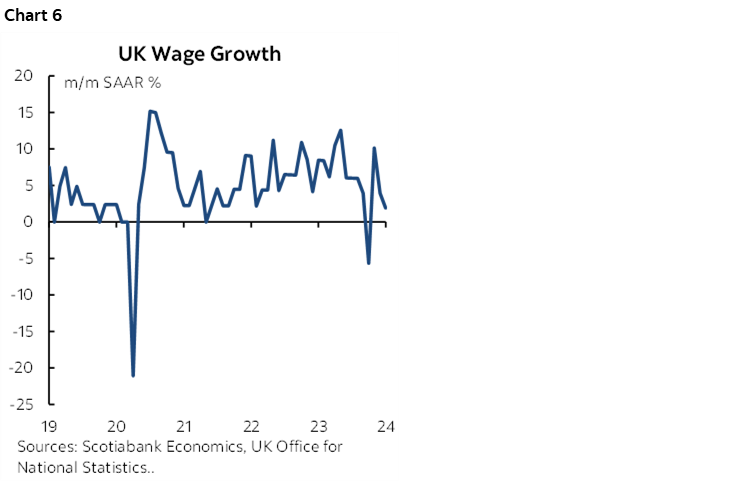

- UK wage growth moderated: Wage growth cooled in January in m/m terms at a seasonally adjusted and annualized rate but remains along a volatile path (chart 6).

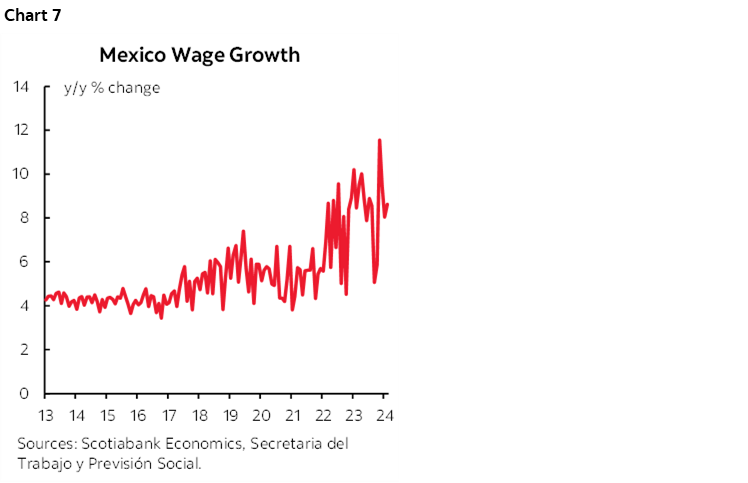

- Mexican wage growth remains hot: Mexican wage growth also eased but remains high (chart 7).

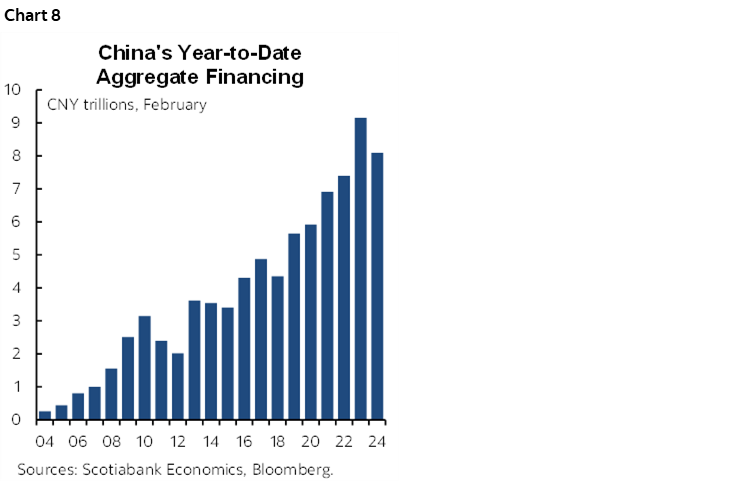

- China’s credit growth slowed: Chinese financing activity eased off in February after a torrid start to the year in January. The stronger than usual surge in January and moderation in February may have been due to shifting timing of the Lunar New Year effects. Still, the two months combined are shaping up to be the second strongest on record (chart 8).

KEY EXPECTATIONS FOR THIS WEEK

Here are brief highlights of key expectations for this week.

- FOMC (Wednesday): This will be a full set of communications including the statement (2pmET) and Summary of Economic Projections with the dot plot (2pmET) and followed by Chair Powell’s press conference at 2:30pmET. Expect a hawkish tone that is in no rush to be easing and therefore I continue to think market participants should be paying the June contract at a minimum and likely later ones as well. Our house forecast remains unchanged in expecting a first cut in Q3 and 100bps of cuts by year-end; I think the clear risk is less than that and perhaps no cuts whatsoever. The dot plot may downshift from 75bps of cuts this year to two given how close the dispersion of the dots between the two estimates was at the December meeting. Expect a fuller discussion on balance sheet plans including QT timelines, but with no decision to be announced at this meeting. Nothing I’m reading from key Fed officials makes it sound like they think the QT plans need to be adjusted imminently. A recent Bloomberg survey showed only 2 participants expecting an announcement to adjust QT at this meeting and only a minority expecting an announcement in May. Most expect June or later.

- BoJ (Tuesday): Will the era of negative rates that was introduced in 2016 come to an end this week? That’s unclear but entirely possible. A significant minority of 11 forecasters within Bloomberg’s consensus survey of 40 participants expects a hike overnight while the majority expects no change. The BoJ loves to surprise and puts little stock in the value of setting up policy shifts. Weekend media reports including a Nikkei newspaper story leaned toward an imminent shift. Friday’s aforementioned wage figures added to sentiment even though they were in the ballpark of expectations. My views on the BoJ and how I think it needs to tread very carefully were expanded upon in the prior week’s Global Week Ahead here.

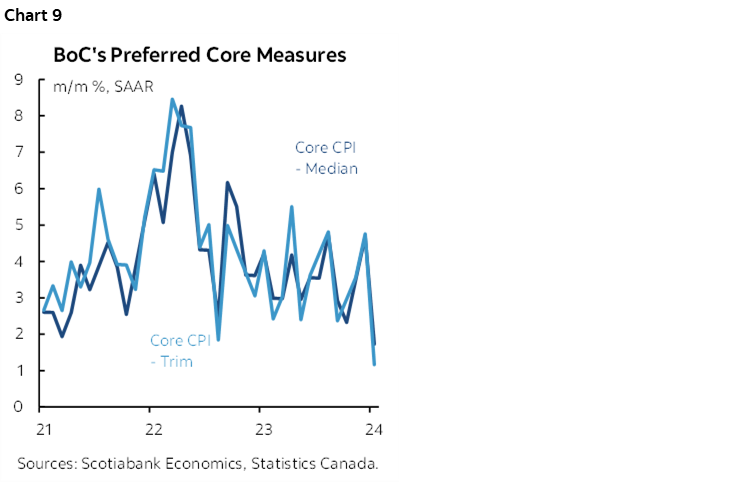

- Canadian CPI (Tuesday): I’ve estimated a headline rise of 0.7% m/m NSA with the year-over-year rate climbing from 2.9% to 3.2%. Key, however, will be whether the trimmed mean and weighted median ‘core’ CPI gauges rebound from January’s soft readings (chart 9). I think they might but won’t be fussed if it takes a little longer to get away from unusual distortions that pushed the readings lower in January. For a recap of what drove January’s softness go here.

- BoC's speech on balance sheets (Thursday): Deputy Governor Gravelle delivers what was once a hotly anticipated speech at least in the minds of those focused upon the BoC’s Quantitative Tightening plans. Why are you delivering this speech? Oh, because you committed to doing so before Governor Macklem basically made it pointless. Macklem did so back here when he said they didn’t think QT was the reason behind why the CORRA measure was overshooting the overnight rate and that this was instead due to demand for long bonds on rate cut expectations that drove demand for funding higher. I’m less sure of that. CORRA was overshooting o/n since the end of last Summer when rate cuts weren’t even in the cards. Instead of curtailing QT, the BoC has invoked a complicated patchwork of messy funding tools ranging from prior use of repo operations to now using receiver general auctions and cash management bills to address pending maturities of GoC bond holdings into next month. It’s QT that’s distorting funding markets and instead of admitting it the BoC is messing up funding markets. In any event, Gravelle’s speech might fill in a few details but willl probably just reinforce the QT plans he outlined in his speech last March, even though, in my view, the BoC should be more open to reducing QT earlier than planned.

- BoC Summary of Deliberations (Wednesday): Pointless, move on. This was supposed to be the BoC’s version of meeting minutes at the behest of the IMF but it is only a very general rehash of prior communications with little to no value added.

- BoE (Thursday) and UK CPI (Wednesday): While no policy changes are expected at this meeting, key will be whether they signal more strongly that they are open to nearer-term easing. I doubt they will go out on a limb in doing so just yet even if they have in mind a path toward easing by summer. There was one dissenter who favoured doing so at the prior meeting and forecasts generally supported easing over 2024H2. Wednesday’s CPI readings for February may inform last minute positioning after a relatively soft m/m core reading in January.

- Canadian retail sales (Friday): Statcan had previously guided that nominal sales fell –0.4% m/m SA in January but this number may be revised. More important may be preliminary guidance for February along with the details for January including volumes.

- RBA (11:30pmET): Tonight’s RBA decision is expected to leave the cash rate unchanged at 4.35% and to continue to err on the hawkish side. It will likely prefer to wait until it sees CPI for Q1 on April 23rd given that Q4 saw only a relatively mild deceleration in weighted median and trimmed mean CPI in q/q terms.

- Chinese banks' LPRs (Tuesday): Tomorrow night’s (ET) decisions are expected to leave the 1– and 5-year Loan Prime Rates unchanged after the PBOC held its policy rate last week which matters to the 1-year, and after banks were pressured into cutting the 5-year rate the last time on February 20th.

- Banxico (Thursday): Mexico’s central bank is expected to cut its overnight rate by 25bps this week without waiting for the Fed.

A number of other global central banks will issue decisions this week and I’ll expand upon them in daily notes throughout the week. They will include Norges Bank, the Swiss National Bank, Brazil’s central bank, Bank Indonesia, Taiwan’s central bank and for entertainment purposes I suppose we can acknowledge Turkey’s decision and begrudgingly Putin’s central bank.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.