ONE-TWO PUNCH DERAILS PLAN TO BALANCE

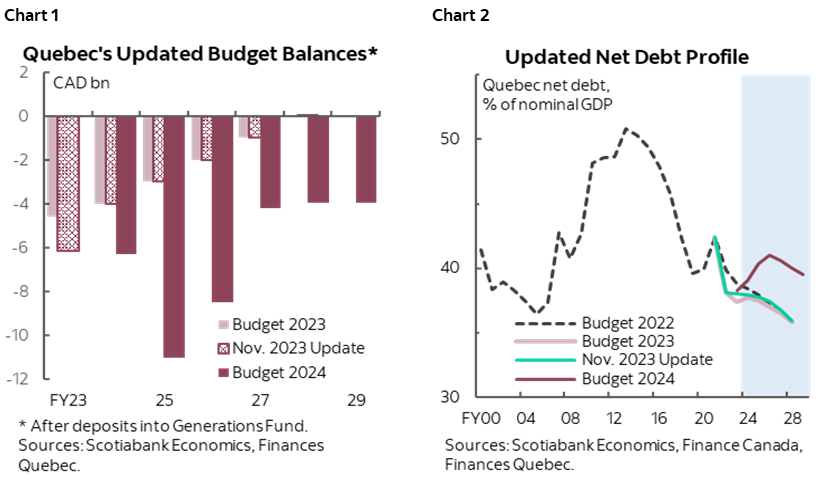

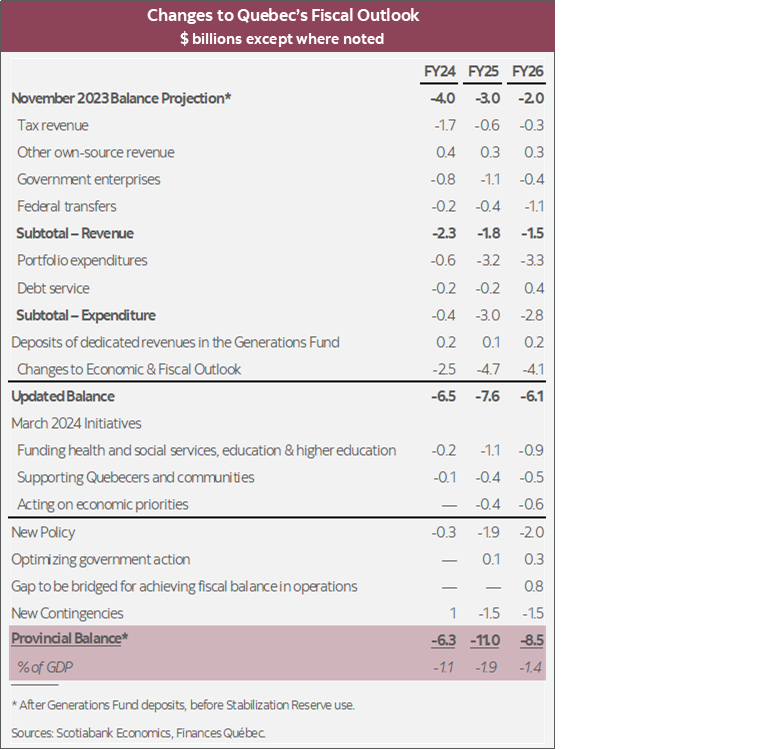

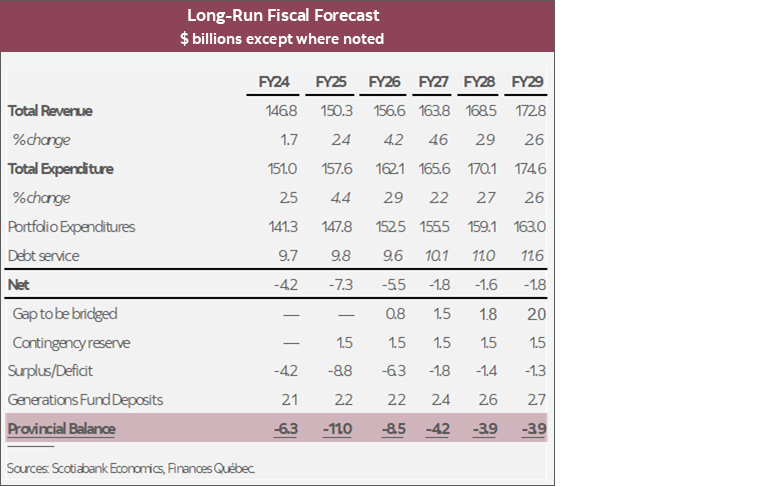

- Budget balances: -$6.3 bn (-1.1% of nominal GDP) in FY24, -$11 bn (-1.9%) in FY25, -$8.5 bn (-1.4%) in FY26 (chart 1)—a combined deterioration of $16.8 bn over three years compared to the November 2023 update (all figures after Generations Fund deposits); structural deficits projected at around -$4 bn (-0.6%) from FY27–29. Revised plan for fiscal balance to be unveiled in next year’s budget, targeting balance by FY30.

- Net debt: raised to 39% of nominal output for FY24 and is expected to peak at 41% in FY26 before declining gradually to 40% by FY28—four ppts higher than projected in the November 2023 update (chart 2). Debt reduction target of 30% net debt-to-GDP by FY38 still intact despite a change to the rate of reduction.

- GDP expectations: real growth assumptions nudged down to 0.6% this year, increasing to 1.6% next year. Nominal GDP projected to grow by 4.0% this year—above the 3.4% forecast in the previous plan—with a continued growth rate of 3.8% next year.

- New policy: $317 mn in FY24, $1.9 bn in FY25, $2.0 bn in FY26, combined $8.8 bn over FY24–29—over half of which focuses on funding of health and social services, education and higher education, with the remainder dedicated to support communities and economic priorities.

- Financing program: expected to reach $36.5 bn in FY25 and $32.7 bn in FY26, and average $27 bn during FY27–29; projected FY25–28 total is about $18.3 bn more than forecast in the November 2023 update.

- The province braces itself for ballooning deficits and greater debt as it faces a one-two punch of economic stagnation and rising spending needs. While major investments in public service and relief measures announced over the past years have eroded Quebec’s fiscal advantage, the budget sets out realistic expectations with an appropriate outlook and a $7.5 bn contingency reserve over five years. We view the investments in this budget as beneficial to long-run growth but take time to bear fruit.

OUR TAKE

Anticipating another year of tepid growth, Quebec’s fiscal position is forecast to deteriorate markedly over the planning horizon, exacerbated by heightened spending in the public service. FY24 deficit is expected to come in deeper than previously planned at -$6.3 bn (-1.1% of GDP), driven by lower tax revenue and a drop in Hydro-Québec’s dividend following last year’s droughts—before widening to -$11 bn (-1.9% of GDP) in FY25—previously forecasted at -$3 bn (-0.5%). Relative to the November 2023 mid-year update, own-source revenue projections were reduced by around $1.3 bn per year from FY24–26 due to a weaker growth profile. Portfolio spending is tracking around $3 bn higher per year in the next two years, largely the result of higher portfolio spending from increased investment in public services.

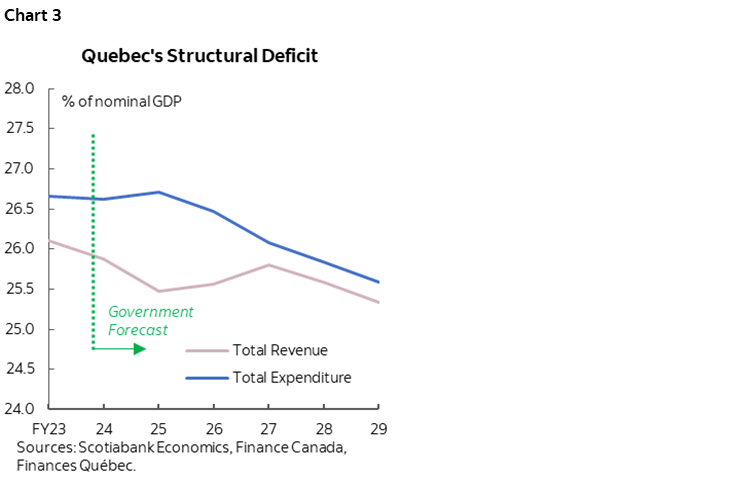

A revised plan for fiscal balance is expected to be unveiled in next year’s budget, targeting balance by FY30. The government aims to eliminate the -$4 bn structural deficit (i.e., budget balance post-deposits into the Generations Fund) over the remainder of the planning horizon by widening the gap between revenue and expenditure growth. Total expenditure is expected to increase to 26.7% of GDP in FY25 with lifted spending in public services, while total revenue is projected to drop to 25.5% of GDP, partly from recent tax cuts (chart 3). Over the medium term, revenues are set to increase faster than expenses—the average annual growth in revenue (AAGR) will reach 3.3% by FY29, while the average annual growth in expenditure will reach 2.9%. However, to eliminate the shortfall, the government will need to increase the growth gap from the current 0.4 ppts to reach 1.1 ppts over the planning horizon.

The government anticipates robust revenue growth despite strong near-term headwinds. Own-source revenue is expected to rebound by 4.7% in FY25 despite softer expected economic growth, reversing some of the FY24 revenue losses in corporate taxes and Hydro Quebec’s contribution. Federal transfers are set to decline by -6% in FY25 mainly due to a drop in equalization resulting from changes in the 2023 federal budget. In the following two years, revenue growth is supported by a rebounding economy, which is expected to average around 4.4% annually.

The economic outlook appears grim but realistic as the province experiences a rapid slowdown. Real GDP growth is estimated at 0.6% this year, before picking up to 1.6% next year—in line with our current outlook but slightly more optimistic than private-sector averages. We remain optimistic about Quebec’s growth this year, expecting it to surpass last year’s estimated 0.2% real growth as the economy gains momentum once the Bank of Canada starts to cut interest rates. However, concerns arise regarding a deeper slowdown if high interest rates persist. The update presented an alternative scenario that forecasts a recession in 2024 with Quebec’s economy contracting by –0.5%. The potential fiscal impact of the alternative scenario is estimated at -$1.8 bn in FY25, -$751 mn in FY26, and -$334 mn in FY27. To ensure preparedness for further deterioration in the economic situation, the current planning also includes a hefty contingency reserve of $1.5 bn each year over FY25–FY29.

New policy initiatives amount to $8.5 bn over five years—or about 0.3% of GDP per year, split over FY25–FY29. Big-ticket items in the Budget include the $4.9 bn over five years to fund health and social services, education, and higher education. An additional $2 bn was allocated to support Quebecers and communities through promoting access to housing and social inclusion. The $1.8 bn dedicated to economic priorities encompasses a wide array of initiatives, including bolstering key sectors of the province, fostering innovation and enhancing productivity. The government is also taking measures to optimize its action, improving tax collection efforts along with tighter targeting of certain business tax measures, resulting in additional revenue totalling $2.9 bn over the next five years.

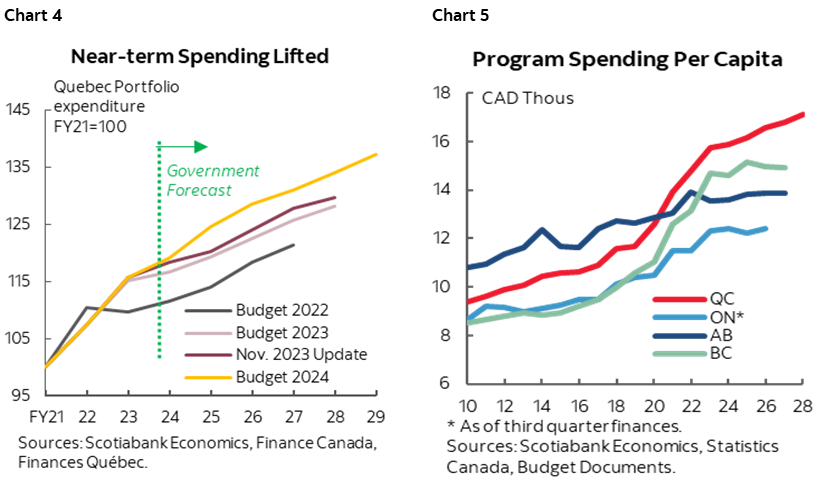

The introduction of new policy measures, along with the impact of wage increases recently negotiated with teachers and health care workers, resulted in portfolio expenditure jumping by 4.6% in FY25 (chart 4). New expenditures focus on healthcare and social services, education and higher education, which are expected to see respective growth of 4.2%, 9.3% and 3.5% in FY25. Portfolio spending growth is projected to slow to 2.9% in FY26 and remain at an average of 2.5% per year rate through FY29, generally below expected population and inflation gains beyond this year. Quebec’s program spending per capita remains well above that of Ontario, Alberta and British Columbia (chart 5). Debt servicing charges are expected to remain flat over the next two years before pushing higher after FY26 due to the province’s growing debt burden. While debt servicing cost is set to rise above 6.7% of revenue by FY29, it remains relatively low historically.

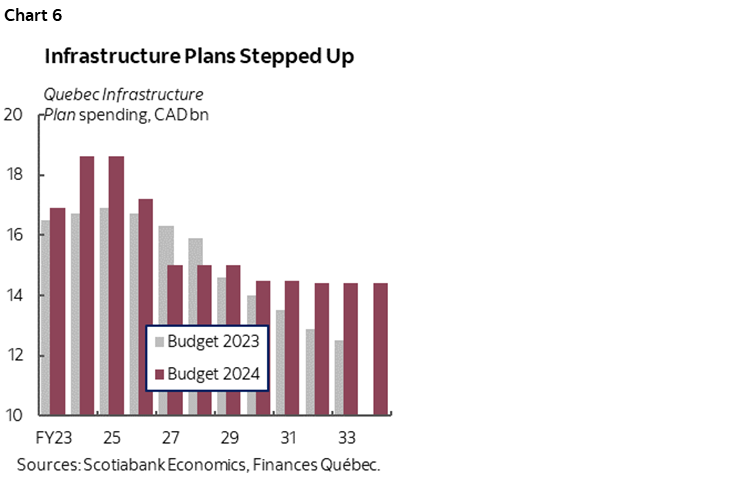

In line with the province’s significant public infrastructure needs, the Quebec Infrastructure Plan has been boosted by an additional $7.2 bn over FY24–33 versus last year’s budget, averaging $15.3 bn over the following 10 years (chart 6). Capital outlays under the Quebec Infrastructure Plan (QIP) are now expected to remain elevated at $18.6 bn in FY25 after jumping by 10% in FY24. Robust capital investment has the potential to boost near-term economic growth in the province and provide some support in the ongoing slowdown. Quebec’s per capita public capital stock has caught up with that of Canada and has surpassed that of Ontario.

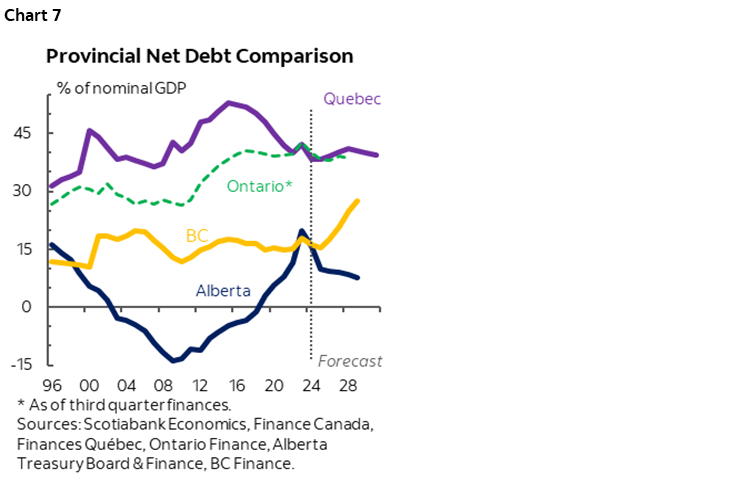

Deeper deficits and ramped up capital spending add to the province’s debt burden (chart 7). Quebec’s debt-to-GDP ratio is forecast to edge higher in the next two years and peak at 41% in FY26—the highest among all provinces other than Newfoundland and Labrador. Over the medium term, Quebec’s debt burden is projected to get back on a downward track on the back of an improving economic outlook, although on a much higher trajectory than previously planned. The debt burden is still lower than before the pandemic, and Quebec is staying the course on its objective of reducing net debt to 33% of nominal output by FY33, then to 30% by FY38. The government plans to withdraw $4.4 bn from the Generations Fund in FY25 and $2.5 bn in FY26 to pay down debt and thus reduce borrowing requirements. The balance of the Generations Fund currently sits at $18.5 bn (8% of net debt).

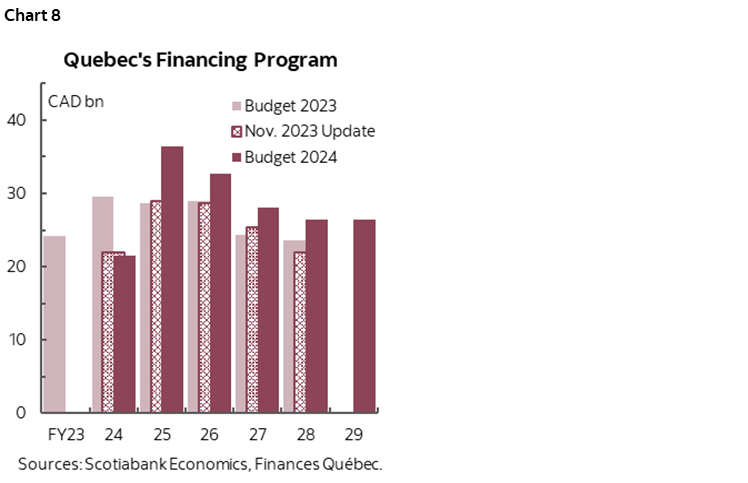

In line with the deeper deficit profile, the province anticipates a much larger borrowing program from FY25 to FY28—a combined increase of $18.8 bn versus the November 2023 projection (chart 8). The province now expects to borrow $36.5 bn in FY25, $32.7 bn in FY26, $28.1 bn in FY27, $26.5 bn in FY28 and in FY29. To date in FY24, 34% of borrowing had been conducted on foreign markets—higher than the 27% average in the last 10 years.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.