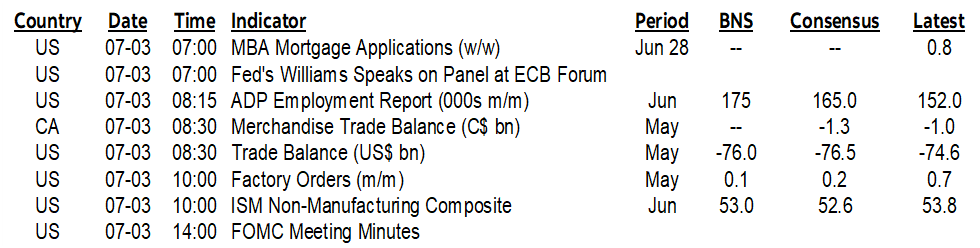

ON DECK FOR WEDNESDAY, JULY 3

KEY POINTS:

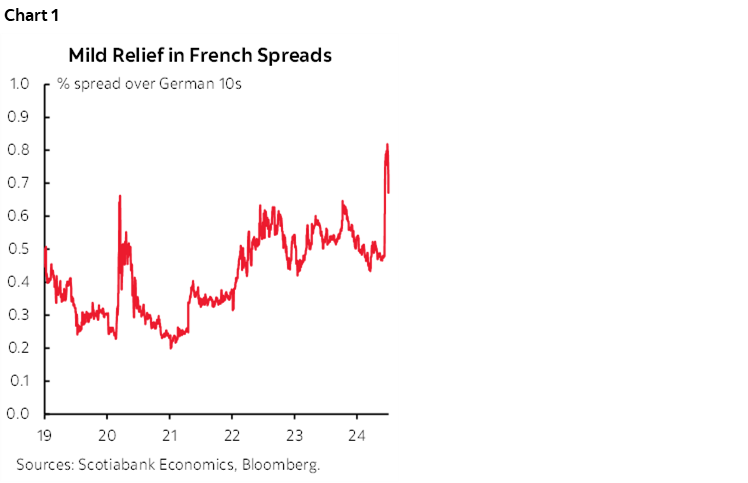

- French spreads over bunds tightest since immediate aftermath of EU elections

- European markets signal French relief; real or head fake?

- US data dump precedes early market closures…

- …including ADP, ISM-services, job cuts, claims, factory orders...

- …as FOMC minutes land at the close…

- …after Chair Powell said nothing new yesterday

- US vehicle sales look sus

There were no material overnight macro developments. The US will seek to cram in a bunch of reports before those market participants who bothered to show up today split town and liquidity suffers.

Day-to-day volatility ahead of France’s second round election on Sunday is motivating a bit more optimism as the parties circle the wagons around the Le Pen’s National Rally by rigging the candidates through strategic drop-outs. This has European stocks broadly higher and French bond spreads slightly narrower including 10s that at 67bps over 10-year bunds is the narrowest since June 12th (chart 1). I don’t buy a competing narrative that posits Powell said anything useful yesterday. The probable outcome of a hung French parliament carries its own set of risks, but markets are viewing this as more palatable than Le Pen and her 29-year-old side kick Jordan Bardella.

US bonds shut at 2pmET and stocks close at 1pmET before Wall Street hits the highway to the Hamptons. Several US macro readings are on tap including ones that can tend to spice up vol. ADP payrolls (8:15amET) are useless for forecasting nonfarm payrolls, but don’t try to convince markets that often react. US ISM-services may be more relevant (10amET). US job cuts (7:30amET), claims (8:30amET) and factory orders (10amET) are also in the mix.

FOMC minutes land just as bonds shut for the early close ahead of the July 4th holiday (2pmET) and just after US stocks have shut (1pmET). Fortunately, I don’t think that this round will offer materially different messaging to what we’ve been hearing from Powell et al. His messages at Sintra were the same as before; they are making progress but need more data and evidence to ensure that this continues.

US vehicle sales landed at 15.3 million units SAAR late yesterday for a 3.8% m/m SA decline that on its own would shave about –½% m/m off of the month’s retail sales figures. What’s unusual about this sales number is that it matched the guidance for just the first half of the month in terms of the number of selling days and hence before the CDK hack hit. Therefore, the second half of the month’s sales appear to have been unaffected by the hack relative to the first half. Maybe they would have been stronger yet, assuming no revision risk given that numerous companies were reporting handwritten sales and weaker dealer productivity. I would be careful with data quality.

It’s not just autos that are impacted either. From what I understand, CDK’s hack also affected heavy equipment sales. CDK is reporting today that operations are mostly back to normal which will mean that what was lost in June may be pushed into July with a lag as they work off the backlogs.

I think Canadian auto sales should be released today but there is no set schedule. They’re usually on a similar release schedule to the US.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.