ON DECK FOR MONDAY, APRIL 29

KEY POINTS:

- Bonds richen, USD softens to start an action-packed week

- Softer than expected start to tracking Eurozone inflation pushes yields a little lower

- The yen’s wild night was driven by intervention speculation

- Global Week Ahead reminder

As a reminder, please see the Global Week Ahead — Too Early to Cut, Too Late to Hike here in full publication format. No slide deck this time due to travel. Key topics:

- FOMC’s prior lack of a killer instinct…

- …lessens its ability to fight inflation now

- The Fed has other options to explore…

- …before courting massive risks with added hikes

- Nonfarm will be part of a suite of US job market readings

- Tracking Canada’s economic rebound

- Eurozone inflation may face upside risk ahead of key June meeting

- Eurozone GDP will also inform the path to June

- China’s PMIs are likely to signal modest growth

- BanRep likely to cut again

- Norges may have less confidence in an autumn cut

- Will Swiss CPI embolden another SNB cut?

- Is NZ wage growth still too hot for the RBNZ?

- Mexico’s soft economy poised for an update

- OECD to update forecasts

- Global macro

Bonds are richening on the back of the first glimpses at April CPI readings in the Eurozone, but it’s a pretty dull start to what is going to be an active week for macro risk.

Sovereign yields are down by 2–5bps across countries and maturities. Stocks are mixed with N.A. futures up a bit along with London’s cash market while the rest of Europe is doing very little.

The dollar is a touch softer this morning with the biggest mover being the yen that started the Asian overnight session dipping toward 160 to the USD before suddenly bouncing back toward about 155.80 now. The suddenness of the move just after midnight ET spawned intervention speculation. If so, then good luck to them, as intervention typically yields fleeting effects against more fundamental forces.

German states released CPI prints for April that point to the national reading doing no worse than consensus estimates and possibly a smidge better. Four out of six states reported 0.6% m/m for headline CPI, one landed at 0.4% and the other at 0.3%. Consensus had expected 0.6% for the national reading that arrives at 8am.

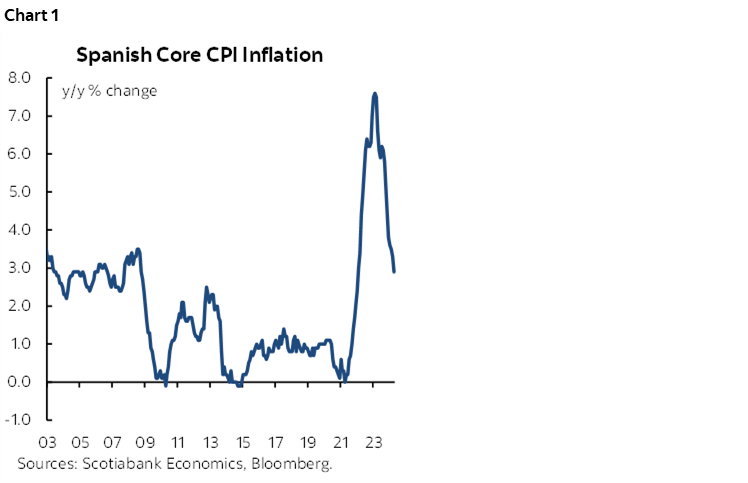

Spanish CPI rose by 0.7% m/m in April (1% consensus) with the EU-harmonized reading at 0.6% (0.7% consensus). Core CPI fell to 2.9% y/y (3.3% prior, 3.2% consensus). Chart 1.

The Eurozone add-up plus estimates from France and Italy arrive tomorrow. We get one more round of Eurozone inflation readings on May 31st before the June 6th ECB meeting.

There are no material releases on tap in either Canada or the US today.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.