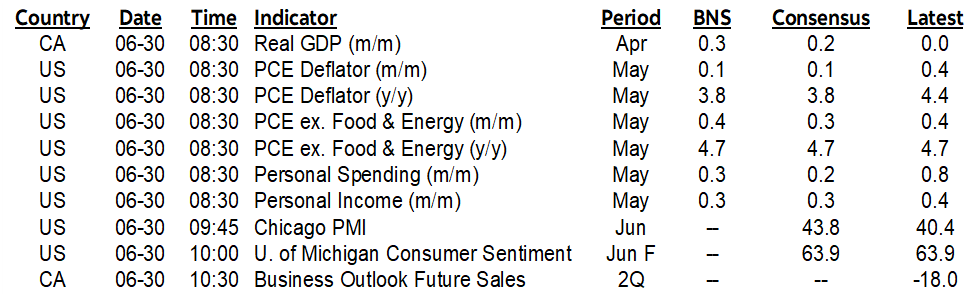

ON DECK FOR FRIDAY, JUNE 30

KEY POINTS:

- Sovereign bonds cheapen again on heavy overnight and expected releases

- Eurozone core CPI lands hotter than usual again

- China PMIs slipped again

- PBoC’s efforts to stem yuan’s slide fail again

- Yen stabilizes post-data

- European consumer spending rebounds

- Canadian GDP: April gain, May softness?

- BoC surveys to inform inflation expectations

- US core PCE expected to be hot in May and June

- BanRep expected to hold

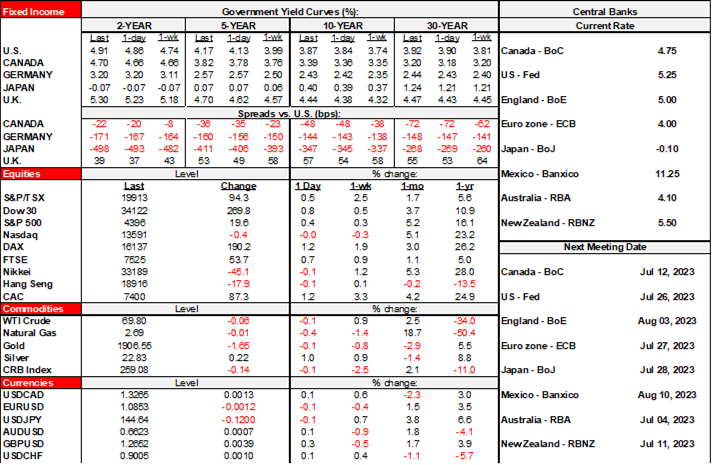

If you were hoping for a nice quiet end to the trading week, well, good luck with that. A wave of fundamentals across multiple markets is combining with month-end and an early 1pmET close for our Canadian fixed income colleagues ahead of the long weekend. Sovereign bonds are taking it on the chin again with milder losses than yesterday across US Ts and gilts and with EGBs outperforming post CPI despite another hot core. N.A. equity futures are up by about ¼% with European cash markets up by 1% at several exchanges. The USD is a touch firmer and mostly versus the euro and related crosses.

1. Eurozone core CPI put in another hotter than usual month. June’s core CPI reading was up by 0.3% m/m in the reported seasonally unadjusted terms versus the historical average of 0.1% which makes this June the second hottest gain on record (chart 1). The 0.2% m/m seasonally unadjusted lift was in line with the historical average for like months. That breaks the pattern of this measure tending to be hotter than average over the prior months. It matters little for now, since the July ECB script has been set and there will be two more CPI readings before the next decision on September 29th.

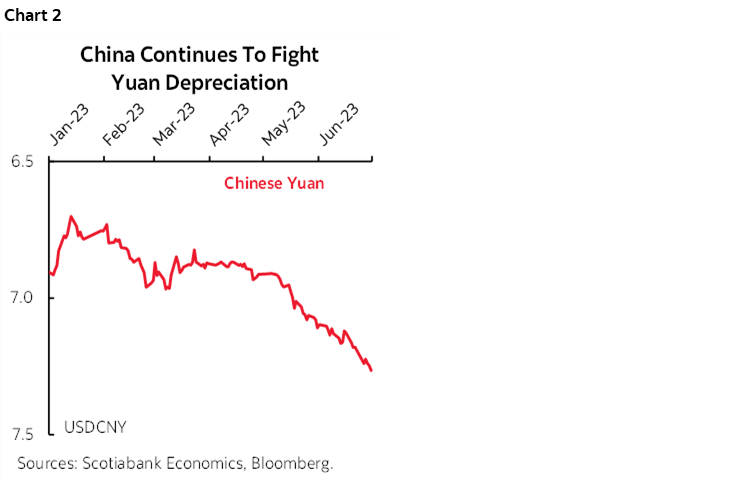

2. The PBoC continues to attempt to stem the yuan’s decline as it set the fix at 7.2258 to the USD which is the fourth time this week that the fix has exceeded expectations. Yet again, the results were disappointing as the yuan depreciated again overnight as a continuation of its fall since early May (chart 2).

3. China PMIs slipped again, adding to concerns about near-term downside risk to China’s economy (chart 3). The composite PMI fell 0.6 points to 52.3 as non-manufacturing fell 1.3 points and a slight up-tick in the manufacturing PMI to 49 from 48.8 was only mildly offsetting. Some of the pessimism is a bit carried away as the composite PMI continues to signal moderate growth near what had been trend leading up to before Covid Zero policies were embraced.

4. Japanese releases were somewhat mixed and the result stabilized the yen but at around 145 to the USD which extends its slid from about 132 in late March as it inches back toward the 150 mark that prompted concern at the Japanese MoF but mostly policy indifference at the BoJ. Tokyo CPI for June was softer than expected both in terms of headline (3.1% y/y, 3.4% consensus) and core ex-fresh food and energy (3.8% y/y, 4% consensus). Industrial output was down 1.6% m/m in May (-1% consensus). Housing starts jumped by 3.5% y/y (-2.7% consensus).

5. European consumer spending rebounded. German retail sales volumes were up by 0.4% m/m (0% consensus) and the prior month was revised down a tick to 0.7%. French nominal consumer spending was up 0.5% m/m (0.7% consensus) and the prior was revised up two-tenths to -0.8%.

On tap into the N.A. session will be the following developments:

1. Canadian GDP (8:30amET) will improve our tracking for Q2 growth and hence resilience. April’s initial ‘flash’ estimate of 0.2% m/m may face upside risk on the detailed release while the first attempt at a flash reading for May is likely to be little changed albeit based on limited tracking.

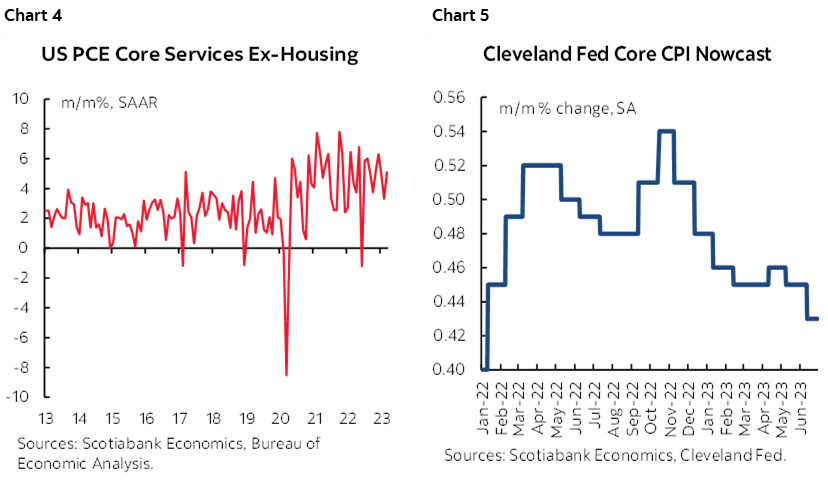

2. US core PCE inflation (8:30amET) is expected to be hot although I think it may be important to look through to core PCE ex-shelter since shelter may not rise as much in PCE as in CPI given about half the weight in PCE and core services ex-housing in particular has been trending at a hot pace (chart 4). Consensus sits at 0.3% m/m. Fwiw the Cleveland Fed’s nowcast is showing about 0.4% m/m for May and for the next reading in June (chart 5).

3. We’ll also get updated tracking of US consumers’ income and spending gains for the month of May. Incomes are expected to be up 0.3% m/m with spending up 0.2% (Scotia 0.3%) based partly upon retail sales.

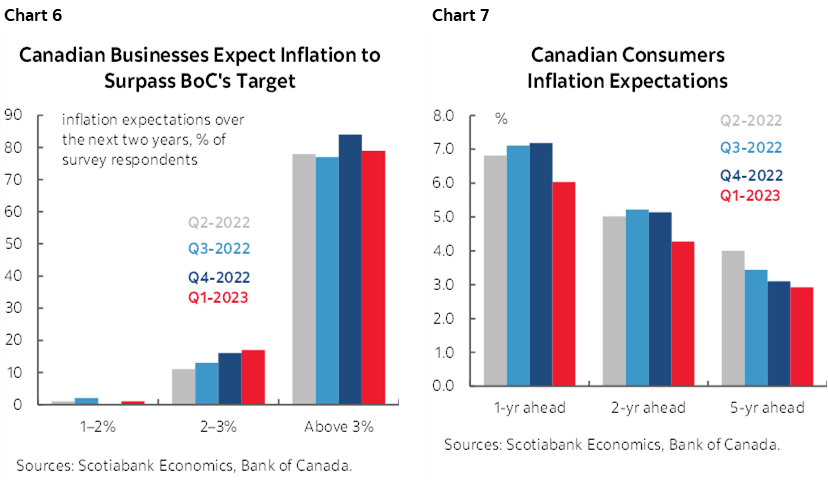

4. Watch the measures of inflation expectations in the Bank of Canada’s twin consumer and business surveys (10:30amET) in addition to the panoply of other measures for future sales growth, wage expectations, house price expectations, cap-ex and hiring intentions etc. To date, consumers and businesses have expressed disbelief toward the goal of achieving the BoC’s 2% inflation target over the years ahead (charts 6, 7).

5. Colombia’s central bank is expected to hold and it may be too early to expect signs toward a future pivot (2pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.