ON DECK FOR WEDNESDAY, JUNE 14

KEY POINTS:

- Global markets await the Fed

- The Fed is likely to pause today…

- …despite strong data…

- …while embracing the high stakes gamble that policy lags will do the trick...

- ...as it courts a more erratic, destabilizing path forward

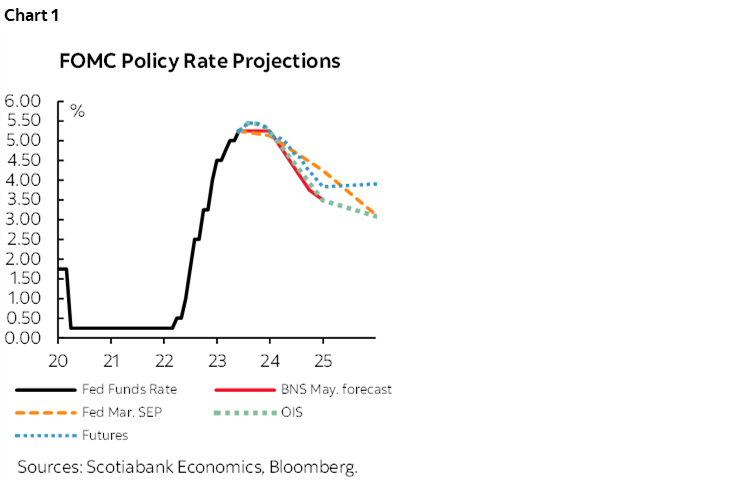

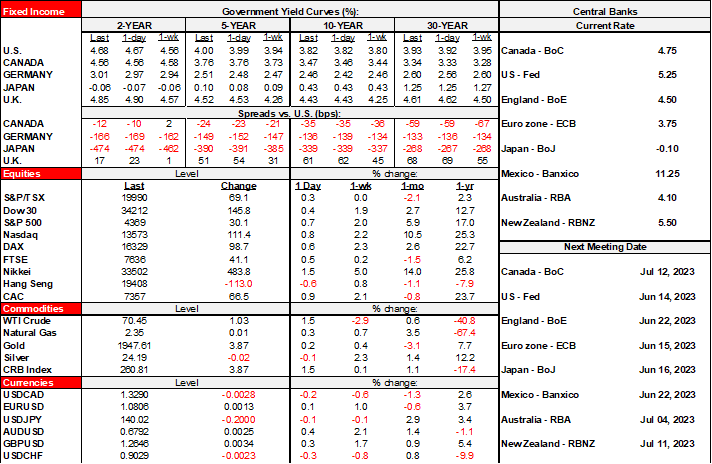

Nothing but the Fed matters today. Overnight developments were light and included April data on UK growth readings that don’t matter, or at least not as much as the other day’s jobs and wages and then next week’s pre-BoE CPI figures. Swedish inflation landed higher than expected across all readings, driving a spike in local yields and a yawn elsewhere. US producer prices will offer inflation theatre before the Fed and nearly two-dozen Canadians won a Stanley Cup for another American city. Stocks are mostly higher across N.A. futures and European cash markets. The dollar is broadly softer. US Ts and Canadas are flat with gilts outperforming and EGBs underperforming. None of it matters until after the Fed with market expectations shown in chart 1.

The FOMC will issue a full suite of communications and they may well have to get the most out of every bit of it in order not to roil or confuse markets. Powell has had occasions when he has not done well at inflection points, to say the least, which may drive elevated vol around the communications. The statement and Summary of Economic Projections with the dot plot land at 2pmET. Chair Powell’s press conference follows at 2:30pmET.

The only convincing reason for doing nothing is that nothing is expected and Powell has conditioned markets to deliver what they want while avoiding game day surprises on the administered rate adjustments. A hike would be extremely unusual with that well worn game plan.

My bias remains that there is a lot of literary licence being applied to Fed-speak that allegedly set up a pause at this meeting that just doesn’t seem accurate. Governor—soon to be Vice Chair—Jefferson intimated a pause “at a coming meeting” which is ambiguous on timing which meeting. Chair Powell’s remarks on May 19th were less about an explicit pause and more about shifting away from explicit set-ups toward heightened data sensitivity and leaving it to game day decisions. Powell said “Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments,” and that no decision had been made about the June meeting’s outcome and that they will take each decision one at a time. I read “look at the data” as meaning, well, they’ll look at the data rather than pre-committing from this point forward.

So what does the recent data say? Recent data does not merit a pause if they are still data dependent, given core CPI (recap here), nonfarm payrolls (recap here), the debt ceiling being out of the way, and regional banks having calmed down compared to when Powell last spoke and given the ambiguity around what he said (Jefferson too).

How about the argument around forward lags and whether they’ve already been given enough time to act?

- First, don’t start the lags around the first hike in March 2022. Start them in the Fall of 2021 when US Ts began to more aggressively price expected hikes. Around 20 months later, we still have precious little evidence that damage is being done.

- Second, I side with Bullard’s take that the real policy rate is toward the lower end of what would be restrictive territory. NY Fed President Williams disagrees with his research that nothing has changed to R* estimates now versus pre-pandemic. Count me skeptical. Highly so. The Fed chased neutral lower amid overly strong post-GFC opinions that it kept having to revise.

- Third, that lower end may not be restrictive enough if there are decent reasons for growth to be more resilient this time. US consumer finances are in the best shape in decades with a 22-year low in the debt-to-income ratio, a record low debt service burden, high cash balances and locked-in financing via the 30-year mortgage refinancing that occurred. This could make consumers better positioned to absorb higher prices for longer. Add to that the fact we’ve never had improving supply chains into a tightening cycle that give the ability to produce more, different labour dynamics that probably mean more resilience, weaker trend productivity and higher pressure on unit labour costs to name a few.

- Fourth, that lower end of the restrictive range may not be restrictive enough if the forces driving inflation over time are greater than in the past. This isn’t about last month’s or next month’s inflation. It’s about structural drivers. Generative AI may be a longer-run disinflationary force, but I’m skeptical toward the blue skying on this topic. I’m more of the belief that we remain at a highly nascent stage of revamping global supply chains given serial shocks to border frictions like the US election in 2016 and ensuing trade policy under both administrations, like the 2016 Brexit vote for which the British people are paying a steep price, like the pandemic, like the Ukraine War and good luck to us all if China-Taiwan frictions boil over. Lowering border frictions and financial distress while accepting higher operating expenses and passing them on could be with us for a long time given that supply chains take many years to change in slow moving fashion. Add to this misguided US immigration policy and basically no population growth that harms longer-term labour market functioning and these are among the reasons why inflation risk is still high over time along with the high risk of the Fed stopping too soon and making policy errors if they ease prematurely.

But what about the risk of systemic shocks due to Fed overtightening, the doves cry. Surely that must halt their actions, no? To me, the lesson learned from CS, First Republic, SVB etc—each of which may have blown up markets for longer if this were 2008—is that regulators will stomp on signs of systemic risk and snuff it out more effectively than in the past. Fifteen years of experience dealing with unconventional policies give public policy makers including the Fed more tools to use to lean heavily against systemic risk. That could make parallels to past Fed tightening cycles that historically have caused challenges somewhat off base if not entirely so this time.

How to condition the bias is where the tricky balancing act comes in and where the sparks could fly in Powell’s hands.

- Dots: Recall that in March they signalled that the Fed would be done now at 5.25%, with about 75bps of cuts next year and 125bps of cuts in 2025 down to 3–3.25% for the policy range. The cleanest thing would be to repeat that and then for Powell to say ignore the dots, they just drew them with a pack of crayons and don’t carry much significance while being data dependent anyway. Shrug your shoulders, say you don’t know, and use the trick of absorbing lots of time answering questions so you don’t have to answer too many. Then we’ll do the same thing we did since January for the BoC while evaluating a conditional skip or pause and the material risk that the Fed could have to come back and hike again later. The dirtier scenario would be to explicitly signal another hike(s) in which case if you have the conviction to do so then why didn’t you do it now? That just seems silly to me especially if they signal another hike as soon as the July meeting; no conviction now, but by golly we know what we’re gonna do in July! Pffft. Tweaking 2024 wouldn’t be very credible in my view because they only have 75bps in cuts and markets won’t believe that guidance anyway. Markets have no trust left for what central bankers say about the longer term.

- Forecasts: Their UR forecast for this year is materially higher than our own (4.5% versus 3.8%). Their core PCE inflation forecast at 3.6% is a little lower than our 3.8%.

- Presser: Expect tight for long, maybe not done, but definitely in no rush to cut guidance with unchanged QT plans. Hopefully the accident-prone version of Powell that we’ve seen in the past is no longer with us, but his accidents have been more likely around moments when the FOMC is not comfortable with providing explicit path guidance.

- Dissenters: I expect some no matter what they do and probably on the hawkish side. Then onto follow-up with individual views that might include dissenting explanations being issued starting shortly after the communications.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.