ON DECK FOR WEDNESDAY, DECEMBER 13

KEY POINTS:

- It’s Fed Day!

- The FOMC is unlikely to validate market pricing for rate cuts

- Expecting a pivot by March is a heroic assumption

- Gilts are outperforming again as UK macro readings disappoint

- Canada has a wartime solution for a war it started and could easily end itself

It’s only the Fed that really matters today. The dollar is gaining against all major currencies perhaps in anticipation of a hawkish feel to the communications. Treasury yields are little changed so far and there is a very mild positive bias across N.A. equity futures and European cash markets.

Other overnight developments were light. UK data was weak again across GDP, industrial output, services, construction output and a wider trade deficit. That drove gilts to outperform others again this morning.

THE FOMC IS UNLIKELY TO SUDDENLY PIVOT

The FOMC statement lands at 2pmET along with the Summary of Economic Projections and the ‘dot plot’. Chair Powell’s press conference follows 30 minutes later.

I gave a preview in the Global Week Ahead (here). It goes over possible changes to the statement, dot plot and macroeconomic projections and what to expect during the press conference. 50–75bps of projected cuts in 2024 is the most likely outcome imo and that implies starting later in the year than markets are pricing.

On balance I think it’s highly unlikely that the Fed validates market pricing for 100–125bps worth of cuts starting by about March and by the end of next year or early 2025.

In the FOMC’s favour in terms of their ability to lean against markets is that the tone of recent data that hardly screams pivot. They are not achieving their dual mandate goals more than two years into when bond markets began tightening in anticipation of Fed tightening. Achieving them with enough conviction that it will be sustainable by March is a heroic assumption.

- GDP growth was over 5% in Q3 and we’d better get slower growth in Q4!!

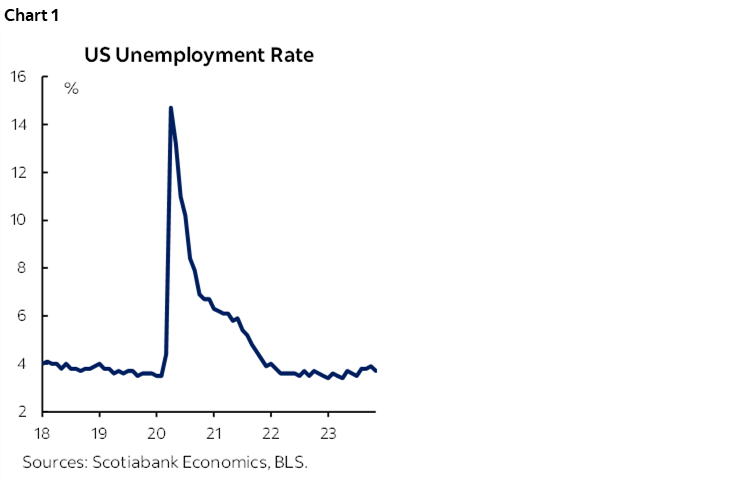

- Payrolls were up by 200k in November which remains above the equilibrium pace, and there were 750k additional household survey jobs created that drove a two-tenths decline in the UR that remains very low (chart 1) while wages accelerated to 4.3% m/m SAAR. Recap here.

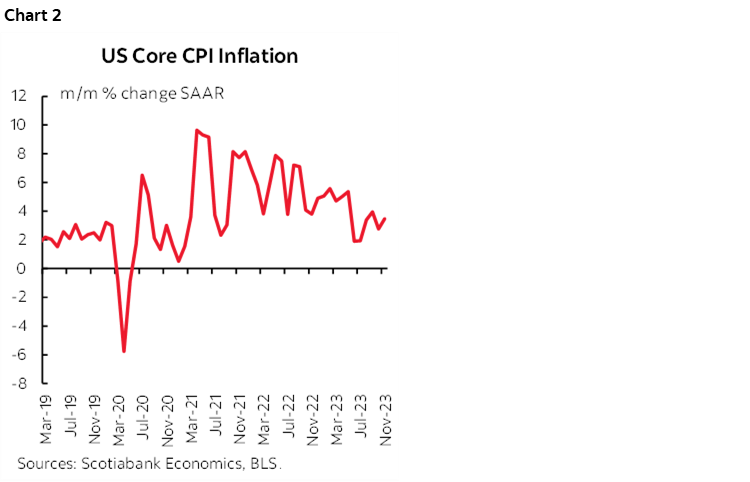

- Core CPI was up by 3½% m/m SAAR last month and it’s pretty clear that the trend remains uncomfortably high and sticky (chart 2) after the softer readings back in June and July (recap here).

- On top of all of that, financial conditions are easing which is normally a red flag for inflation through higher growth at a time when capacity constraints are already pressing.

Yeah, that all screams pivot. Good one.

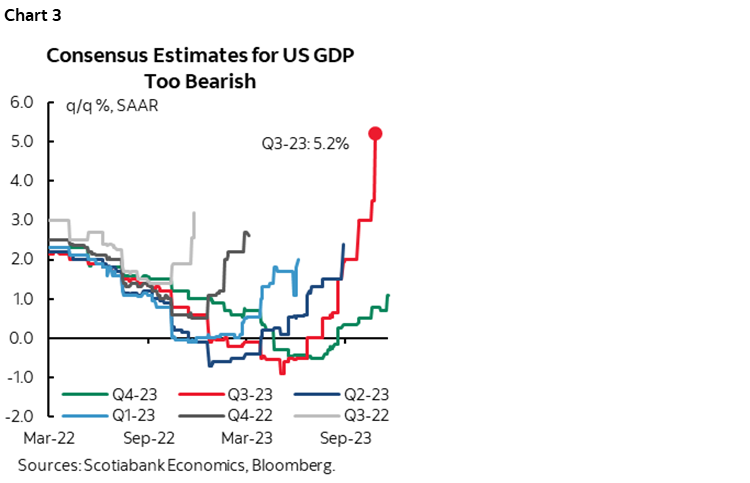

Now you’ll tell me just wait. Everything’s about to crumble and with alarming speed straight into a sewer hole. Maybe, but my counter is that you’ve been telling me that for the past six quarters in which US GDP growth expectations have been revised up and up, over and over each time and still tending to fall short of the ultimate estimates (chart 3). Doom has been postponed six times now. Maybe, just maybe, the US economy’s rate sensitivity is fundamentally different this time around. Maybe, just maybe, we should all respect the evidence.

How so? Households are in vastly better shape with multi-decade bests across multiple measures which lessens their rate sensitivity. A hiking cycle has been accompanied by improving supply chains that have given the opportunity to hire and produce more; when did we last see that happen? We once beseeched governments to help central banks in stimulating the economy and now we can’t stop them as they fight central bank efforts to cool inflation. Wage pressures are well above the Fed’s inflation target.

I think the message we’ll hear from Powell is that it’s much too soon to be talking rate cuts. The dots will say they are coming, but not as soon or by as much as markets wish. He’ll emphasize the same points on progress with respect to the labour market coming back into better but not complete balance and with inflation making progress. He’ll also say we’re some distance from their goals and use the same lines about how history counsels against prematurely declaring victory against inflation. It’s hard to see all of that changing as soon as the March FOMC in keeping with market pricing.

How comfortable am I with this view? I’ll put it this way: markets have been wishing for rate cuts on and off many times during the pandemic.

CANADA’S OWN GOAL ON HOUSING

The Feds’ latest housing solution is prime material for late night comedy. Get this. The Feds started a war on housing. They are now desperately seeking solutions to the war they started themselves. And right before them lies their very own ability to declare peace that they are not declaring. It does not get better than that.

- The Feds started the war with excessive immigration combined with serial overstimulation on the demand side over many years.

- Their latest solution that was floated yesterday is to go back to WWII with the solution being to build a tonne of cookie cutter homes modelled after post-WWII era so-called ‘strawberry boxes’ with a few hundred square feet of living space on tiny lots.

- They could just call it all off by curtailing immigration, maybe even taking a full one-year holiday from any new arrivals before then reducing the flows in order to let the market catch up.

But they won’t. They keep digging deeper and deeper. Scrambling to build a lot of homes very quickly is the solution being touted in order to address Ottawa’s own goal. Brilliant. Here are some challenges.

- For one, the economy post-WWII was struggling with replacing defence spending with private activity and with housing all the people who moved to the cities from rural areas in order to feed wartime production needs. That’s not today’s issue in an economy basically at full capacity and beyond full employment. Heaping housing stimulus onto the picture of an economy dealing with ongoing inflationary pressures could only add to them.

- who is going to build all of these ‘strawberry boxes’? There is already an acute shortage of skilled workers in the housing sector. Immigration has tilted sharply away from the skilled trades during the surge of 2022–23.

- Have they done focus group testing to see if people actually want the type of wartime 'strawberry box houses' the government is thinking about? Or will they build a lot that will turn out like China’s ghost cities? This sounds like Government mandating production of too many homes of a type nobody wants. Tastes have changed since WWII and the housing market is vastly different. Many immigrants being targeted today are skilled and educated with better income prospects who may not want that type of housing.

- If these homes become a concentration of low income neighbourhoods thoroughly lacking planning diversity then they may bring other socioeconomic challenges. It sounds like an urban planner’s nightmare.

- then there is former BoC Governor Dodge's criticism that I’ve also held to. He was by far the most on-the-mark former Governor on the airwaves yesterday! Canada keeps shovelling money into housing and consumption so this diverts capital away from investment and productivity. A richer economy is one that improves the latter, not one that takes on too many new arrivals and diverts capital toward building strawberry boxes in housing ghettos amid a declining standard of living.

- I smell arbitrage opportunity! Build cheap houses like these. Knock 'em down and build bigger ones on the same lots and sell for more later. My long-deceased aunt and uncle had one of these homes when they returned from the War. Their whole neighbourhood has since been knocked down and rebuilt to reflect changed preferences.

- and still, the estimates are millions of homes that need to be built. If they can pull it off then every bit helps, but good luck.

The simpler solution? Cut back on immigration. I’ve long supported higher immigration targets including a piece I wrote two decades ago, but gradually and with proper planning. The sudden shock approach that is being imposed now is clearly excessive. The government is seeking wartime solutions for a war it declared upon itself and the solution for peace lies at its own grasp. Maybe some of that immigration surge should be allocated toward bringing in better comedians.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.