ON DECK FOR TUESDAY, DECEMBER 12

KEY POINTS:

- Markets position for a soft US CPI print

- US CPI is expected to be soft, but it’s core that will matter

- FOMC participants have until tonight to firm up forecasts

- US to auction 30s post-CPI

- Markets bring forward first BoE cut to June 2024…

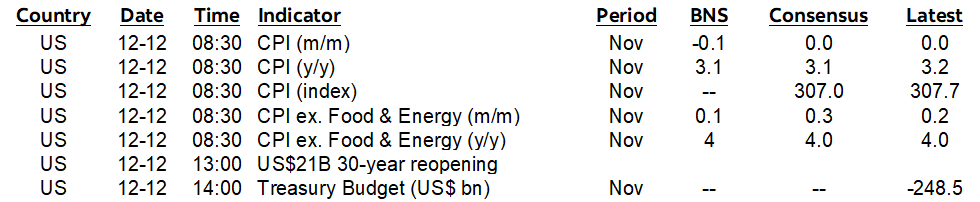

- …after UK wages post the first outright decline since the start of the pandemic…

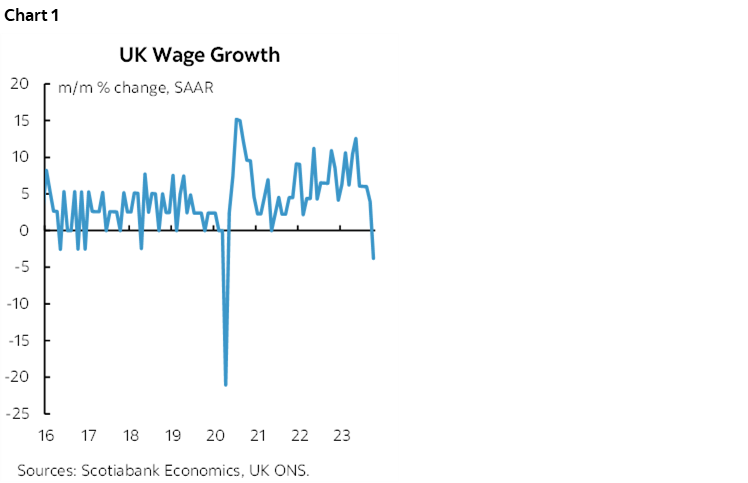

- …and UK payroll employment dips by the most since 2020

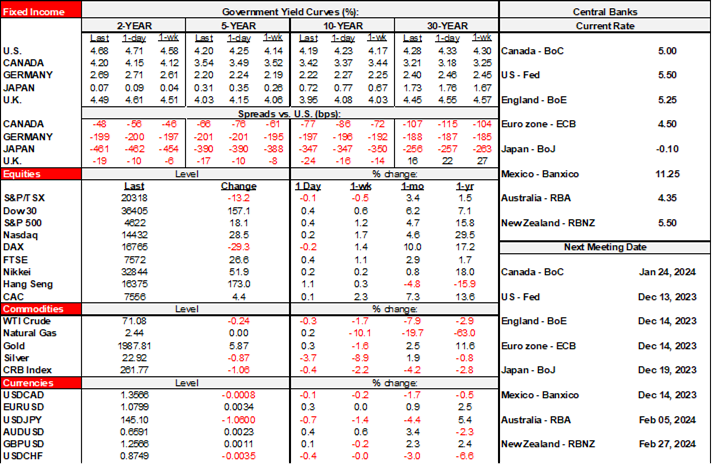

Sovereign bonds are rallying in anticipation of a weak US CPI print this morning while they fade the post-nonfarm reaction. Gilts are outperforming with yields down by about 10bps across most of the curve following soft job market readings. Equities are little changed across NA futures and European cash markets except for about a mild rally in London on brought-forward BoE cut bets. The dollar is broadly softer ahead of CPI, with CAD, sterling and MXN underperforming.

I don’t see the latest readings on UK jobs and wages being impactful to the BoE on Thursday when they hold and counsel patience. They did, however, bring forward market pricing for the first rate cut to the June 2024 meeting that went from about -18bps priced pre-data to just over –¼%. Why?

Wages fell outright for the first time since April 2020 at the very start of the pandemic (chart 1). They were down by 3.8% m/m SAAR in October. It’s only one month, but it sticks out like a sore thumb along what was previously a decelerating but still firm trend.

Payroll positions fell by 12,807 positions in November. That’s the first dip since August after about 70k jobs were created over the months of September and October, and it’s the biggest drop since November 2020. Chart 2.

US CPI PREVIEW

The US updates CPI for November at (8:30amET). Some expectations are offered below and also see my week ahead as part of your readings to prepare.

The CPI update lands right toward the beginning of the FOMC’s two day meeting. Committee participants submitted their forecast inputs to the SEP on Friday evening but have until tonight to submit any revisions to their macro projections and dots. It's therefore plausible that the print could influence some of their dots and the median dots if enough of them are waffling to the point to which one data point matters even in the wake of Friday's jobs and wages.

m/m % change headline / core CPI, November:

- Scotia: -0.1 / +0.1

- Consensus mean: 0.0 / 0.3

- Consensus median: 0.0 / 0.3

- Headline range: Most are calling for 0% or 0.1%

- Core range: 0.3 and 0.2 are the most popular estimates

Rationale:

- The Cleveland Fed’s ‘nowcast for headline CPI is 0% m/m SA. It has tended to overestimate inflation this year.

- The Cleveland Fed’s ‘nowcast’ for core CPI is 0.3% m/m SA. It has also tended to overestimate core inflation this year.

- There are quite a few calls for a weak headline.

- Gasoline will be a significant weighted drag on headline CPI.

- used vehicle prices also slipped according to industry guidance, but new vehicle prices were little changed

- Shelter including OER and rent of primary residence are tracking firmly again

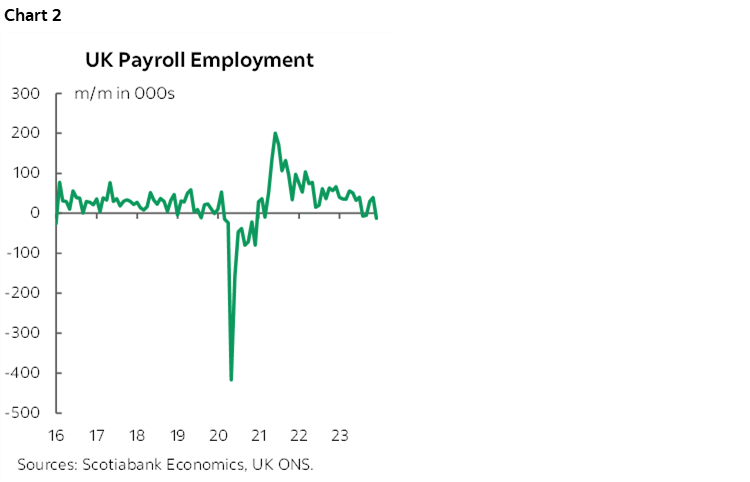

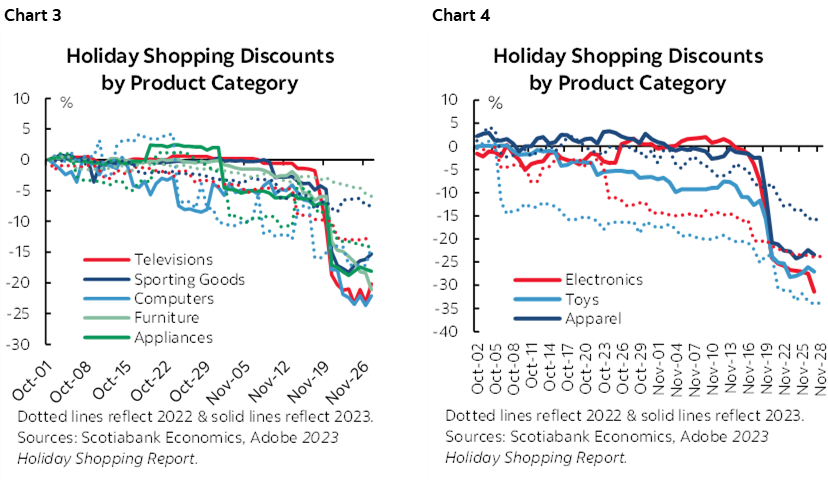

- November saw greater than usual seasonal discounting in a diverse array of consumer items compared to last year and may weigh on several categories (charts 3, 4).

- A wildcard is whether core services light up again. At 0.2% m/m in October, CPI services ex-housing and ex-energy services returned to about the average rate of increase over the April to July period and came off 0.6% the prior month. This could be an upside risk.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.