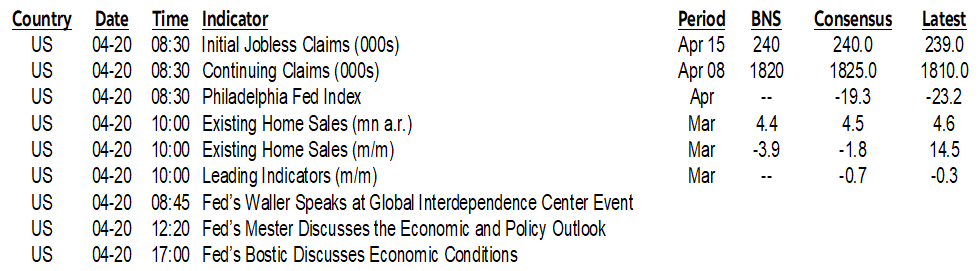

ON DECK FOR THURSDAY, APRIL 20

KEY POINTS:

- Earnings drive risk-off sentiment

- US regional banks mostly disappoint

- NZ inflation surprises lower, rates rally

- Chinese banks leave loan rates unchanged as expected

- Heavy Fed-speak before blackout

- Light N.A. data

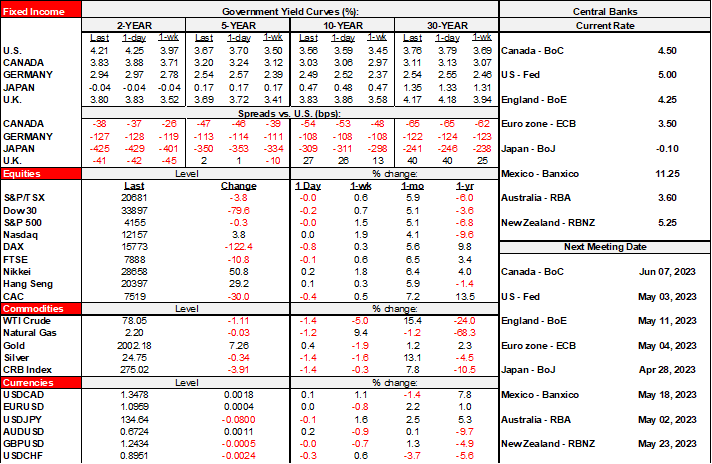

Mild risk-off sentiment is following some soft global earnings reports with light regional macro developments operating in the background. Sovereign curves are generally rallying across major markets this morning as they continue their erratic behaviour. The dollar is little changed on a DXY basis as gainers (euro, A$, yen) offset losers (sterling, CAD, especially the NZ$). N.A. equity futures are down by between 0.3% (TSX) and up to -1% (Nasdaq) with European cash markets down by ¼% to nearly -1% in Italy. Oil is slipping again and WTI is now almost right back to where it closed on the Friday before OPEC’s surprise production cut into the following week despite predictions of $100 oil. Markets never learn when it comes to the fleeting effects of OPEC+ changes.

If anything incrementally influences the market tone then it would be several earnings reports from US regional banks and a heavy line-up of Fed-speak. Regionals mostly disappointed expectations including Keycorp, Fifth Third, and Comerica with the latter beating on earnings and revenues but missing on deposit flows.

BoC Governor Macklem’s reappearance should be a dud in the sense that nothing new is expected after the deluge of communications over the past week (11:30amET).

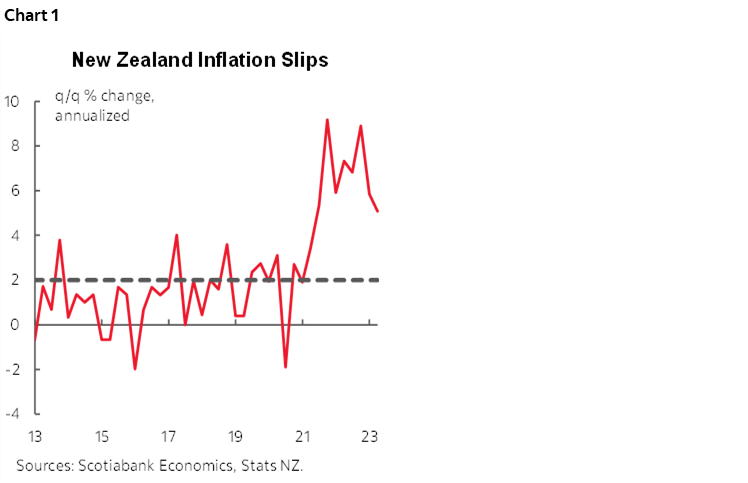

Kiwi inflation surprised by landing a bit lower than expected and that sparked a rally across the rates curve in 2s10s bull steepener fashion and pushed the NZ$ to be the weakest cross to the dollar into this morning. Q1 CPI registered a 1.2% q/q non-annualized gain (1.5% consensus) that contributed toward a cooler year-over-year rate of 6.7% (7.2% prior, 6.9% consensus). This was the softest—but not soft—reading in some time but the figures are volatile and so more evidence is needed (chart 1). The breadth of price increases was also on the softer side outside of food prices that were up by 3.7% q/q. Clothing/footwear (-0.1%) and transportation (-1.3%) both fell and other major categories saw increases of 1% or less.

Chinese banks left their key lending rates unchanged as expected including the 5-year borrowing rate that serves as the benchmark for property markets. This is because the PBoC left its 1-year Medium-Term Lending Facility Rate unchanged.

Fed-speak will try to cram in whatever is left to say before Saturday’s blackout ahead of the May 2nd–3rd meeting and there will be quite a few speakers on tap. I would expect them to reaffirm that a quarter-point hike is likely at the May meeting and stay tuned for when the next pack of crayons draws fresh dots in June. Governors Waller (12pmET) and Bowman (3pmET) will speak and so will regional Presidents Mester (12:20pmET), Bostic (5pmET) and Harker (7:45pmET).

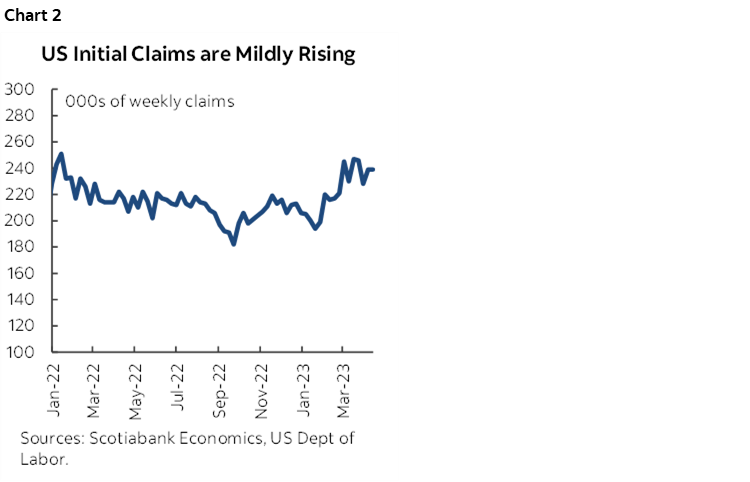

Watch weekly US initial claims (8:30amET). Including the effects of revisions they have indeed been trending mildly higher since late January, but at 240k recently they are still not alarming (chart 2). This tally will start to push through the nonfarm reference week that is the pay period including the 12th of each month. The Philly Fed’s gauge for April (8:30amET) and an expected pullback in existing home sales after February’s 15% m/m surge (10amET) are also on tap.

Mexican retail sales for February unexpectedly fell by 0.3% m/m (consensus +0.5%).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.