ON DECK FOR MONDAY, FEBRUARY 28

KEY POINTS:

- So far, global market stress is manageable…

- …after the allies found their spines over the weekend…

- …but it’s a different matter altogether for Russia

- The ends justify the means in crushing Russia’s economy

- Lehman event or manageable consequences?

- The US oil shock is paying the price for turning down Keystone XL

- The US posts another record monthly trade deficit as retailers re-stock depleted inventories

- Canada temporarily swings back into current account deficit

- Omicron continues to fade

- Please see Friday’s Global Week Ahead here

The ends justify the means. The debate over whether and in what form Machiavelli actually said this isn’t what matters for present purposes. With the end goal defined as destroying the brutal killer Vladimir Putin through internal collapse and dissension by creating a critical mass of internal opposition, the targeted means to achieve this end kicked into higher gear over the weekend. We’re seeing the limited effects upon global markets and the deepening effects on Russian markets to kick off the week. Overall, the response across the allies became considerably more impressive in nature than the timid measures that were initially pursued last week when the words were far stronger than the measures. It’s welcome to see individual companies joining with their own measures. It’s welcome to see more foreign provision of arms to Ukraine, but Harvard’s Niall Ferguson is bang on saying that the amounts remain trivial in his thoroughly enjoyable weekend column about parallels between Biden and Jimmy Carter.

The intensification of measures included banning some undisclosed Russian banks from accessing the global SWIFTS payments system, as well as G7 central banks taking steps to cease transacting with Russian banks, Russia’s central bank, Russia’s ministry of Finance and Russia’s sovereign wealth funds (the National Wealth Fund of the Russian Federation and the Russian Direct Investment Fund). The EC plus G7 minus Japan issued this communique on Saturday (Japan joined the next day), Canada had offered some further details yesterday and the US announced them this morning (here). Russian assets are being frozen in their respective G7 markets right down to the yachts, real estate and investments of Russia’s corrupt oligarchs.

The effects include blocking Russia’s access to its US$643B of reserves that were almost doubled since the last invasion. The allies are catching on to the fact that Putin had taken steps to insulate Russia from sanctions since the last war in 2014 by ramping up reserves, paying down external debt, trying to create an alternative payments system and diversifying FX exposures away from the dollar. Putin gambled that the US would be isolated in whatever sanctions it sought to impose upon Russia and that those sanctions wouldn’t effectively hit at the capital account or would do so in limited fashion by focusing upon the USD. I’m delighted to now see that Putin seriously miscalculated as the allies adapted over the weekend. They can still do more but the biggest remaining options are likely ones—like thwarting the supply of Russian energy—that could take years.

So with that we are in monitoring mode in terms of watching measures of stress across global markets and need to be careful in prematurely drawing conclusions on the impacts and the potential policy responses.

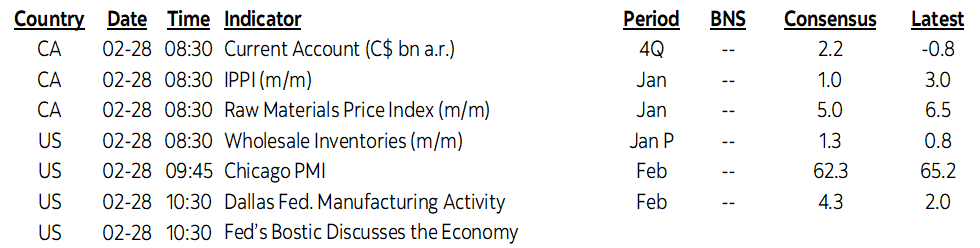

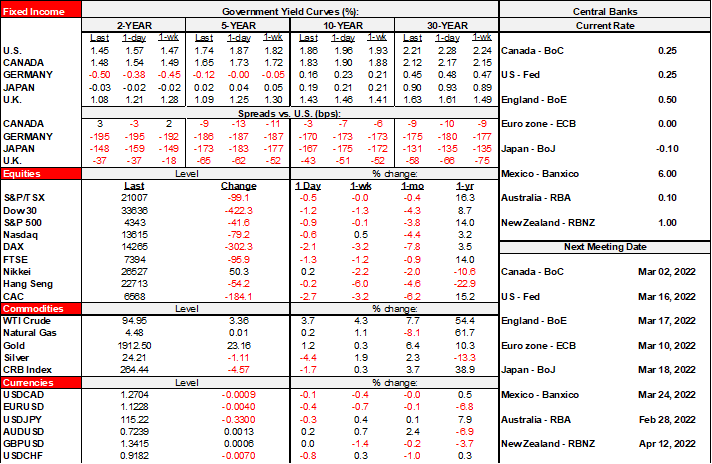

Headlines are somewhat alarmingly drawing parallels to March 2020, but in reality, the magnitudes of the deteriorations across key measures are a fraction of what they were back then—so far. For one, the widely monitored FRA-OIS spread that is a rough measure of systemic risk across the global banking system has climbed to 18ps this morning, up from 13 on Friday and about four times what it was about three weeks ago (chart 1). Still, it was about four times today’s level in March 2020 and about 165bps higher when the GFC was breaking out. The cross currency EURUSD 90-day basis sank to -48bps this morning but was 100bps below that when liquidity initially froze at the start of the pandemic. The VIX has increased to about 33 but had soared to about 50 points above that at the start of the pandemic and a similarly height when the GFC broke out.

Across asset classes, sovereign bonds are catching a limited bid so far. US 2s are about 12bps richer in a bull steepening move that has the long end down by 6bps. Similar moves are occurring in gilts and EGBs. Canada’s curve is richer but underperforming ahead of the BoC on Wednesday. Equities are under pressure with European cash markets down by between 1–3% and N.A. futures off by ~1% across benchmarks. The USD is little changed this morning in part because other safe havens like the yen and CHF are gaining, but also because broader moves are fairly limited despite talk of the risk of flooding the world with dollars to avert a liquidity crisis that at least so far is not in existence. Oil is up by about 3–4% and expectations ahead of Wednesday’s OPEC meeting to raise output by the long planned 400kpbd may be set too low.

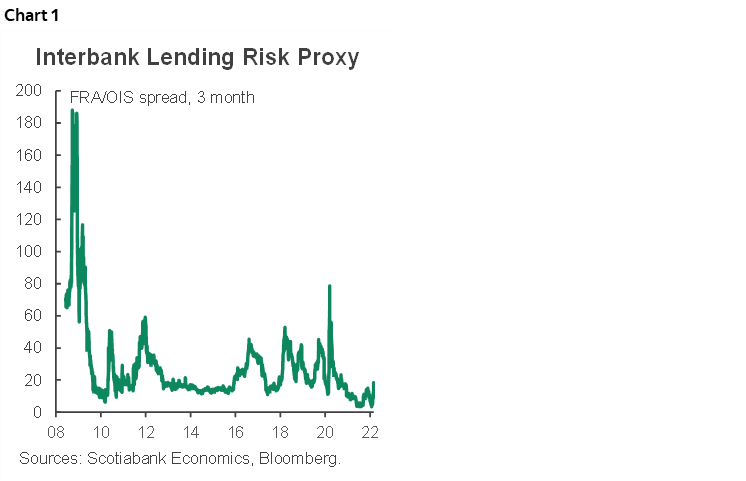

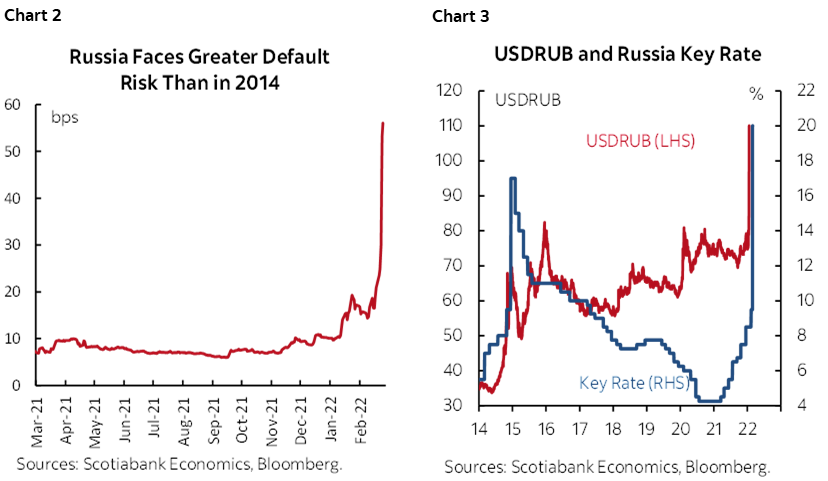

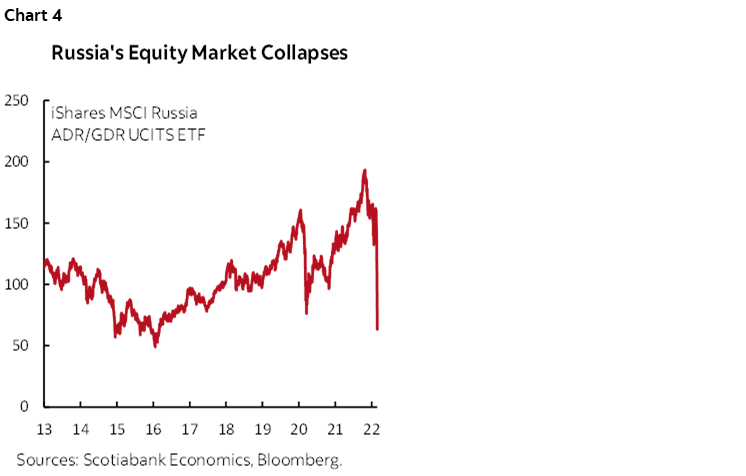

It’s a rather different picture for Russia’s financial markets. A currency and banking run appears to be underway in Russia as savers express diminished confidence in the currency and banks. Cueing costs are piling up. At the same time, Russia’s implied default probability has soared to about a one-in-two chance as of this morning (chart 2). The ruble started off by plunging by about one-third versus the USD but a 10.5 ppt hike by Russia’s central bank cut that in half, albeit with the strong caution that liquidity is severely hampered so treat pricing accordingly (chart 3). The long-term collapse of the ruble is a back door pay cut for Russians that basically import everything they consume other than oil, some minerals and vodka. It destroys their purchasing power on the world stage. Russia isn’t willing to test what this means for stocks and so it shut the stock market, but one can well imagine the direction when it eventually reopens and we can already see that in ADR proxies in London that have plunged toward the lows of the prior invasion (chart 4).

Do I feel for everyday Russians? Absolutely. Many of them didn’t ask for this and don’t support it, though many do. Their life savings and jobs are seriously at stake which is always tragic. But I have far more sympathy toward Ukrainians and fans of democracy the world over. Short of unwisely engaging Russia in direct open conflict, economic war on its population is designed to crush its economy, foment domestic instability and perhaps enact change from within and hopefully one day become vividly illustrated by the toppling of dictator’s statues as seen elsewhere (think Romania, Iraq etc). Putin has gone much too far and at whatever cost now needs to be removed in order to mitigate a potentially far bigger longer run cost if this is another September 1st 1939 moment in the context of a grand master plan.

Is it premature to seek too much comfort in the financial market responses thus far? Perhaps. Some are drawing parallels to a brewing Lehman event. We’ll see, as so far, we haven’t seen skipped payments, mass defaults and failures or real blow-outs in measures of stress. That may yet test the financial infrastructure and the likely policy response over coming days and beyond. But there are important differences to Lehman to consider. Lehman was an idiosyncratic firm event that should have arguably never been allowed to happen. One difference now takes the form of the leakage effects from sanctions like a pivot toward Russia’s alternative payments system, but that only partially insulates the country. Another is that not all of the world’s powerful central banks are refusing transactions with the Russians (think PBOC etc). Another is that while Russia’s capital account is (mostly) shut now, emergency capital control measures are being invoked without having to answer to the inconveniences inherent to a democracy. The longer that persists within the context of the currency’s collapse and imported inflation, the greater the risks to Russia’s economic and financial stability and its spillover effects abroad.

How we got to this point is the distressing part. My belief is that Trump’s bromance toward Putin lost valuable time and his gutting of the State Department resulted in not enough voices flagging what Putin was up to as he was taking those steps to insulate his country from the effects of sanctions. A more effective and more American leader than Trump—who recall through inaction and forms of encouragement sought to bring down his own country’s legitimately elected government after he flat out lost—would’ve stood a better chance at spotting the signs. At least, however, he saw fit to pursued N.A. energy security including support for Keystone XL whereas if the Biden administration really wished to lessen its vulnerability to swings in global oil markets then it has a nearly complete massive pipeline from Canada to reconsider among its options. Killing it was among Biden’s biggest mistakes on par with Germany’s earlier pursuit of the Nord Stream pipeline. Biden traded environmental considerations on his doorstep for heightened environmental and geopolitical risk attached to enemies of the United States abroad. He turned his back on energy supply from a safe and sound neighbour in favour of making the world more reliant upon energy supplied by despotic regimes.

As for other more mundane considerations, there is otherwise very little else on the economics calendar to consider at the start of the week unless another Eurozone inflation beat from Spain that follows Friday’s upside surprise from France, some stale Japanese readings or Australian retail sales do it for you. The US saw its advance merchandise trade balance swing toward a new record monthly deficit of $107.6 billion this morning as inventory restocking via imports drove retail inventories up by another 1.9% m/m in January (4.7% the prior month). Canada updated Q4 balance of payments figures but a markets crowd that saw the international investment transactions move across its desks months ago probably couldn’t care less. Fwiw, the current account swung back into a small deficit position although surging oil prices may swing it back into surplus in Q1.

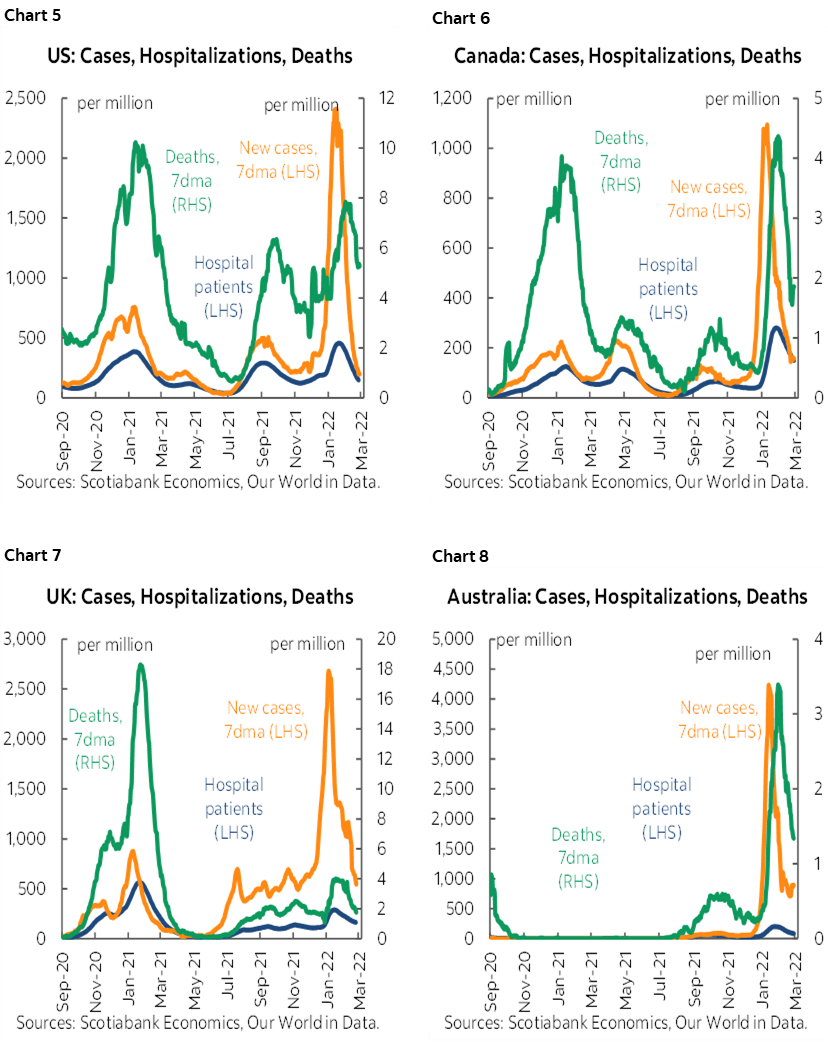

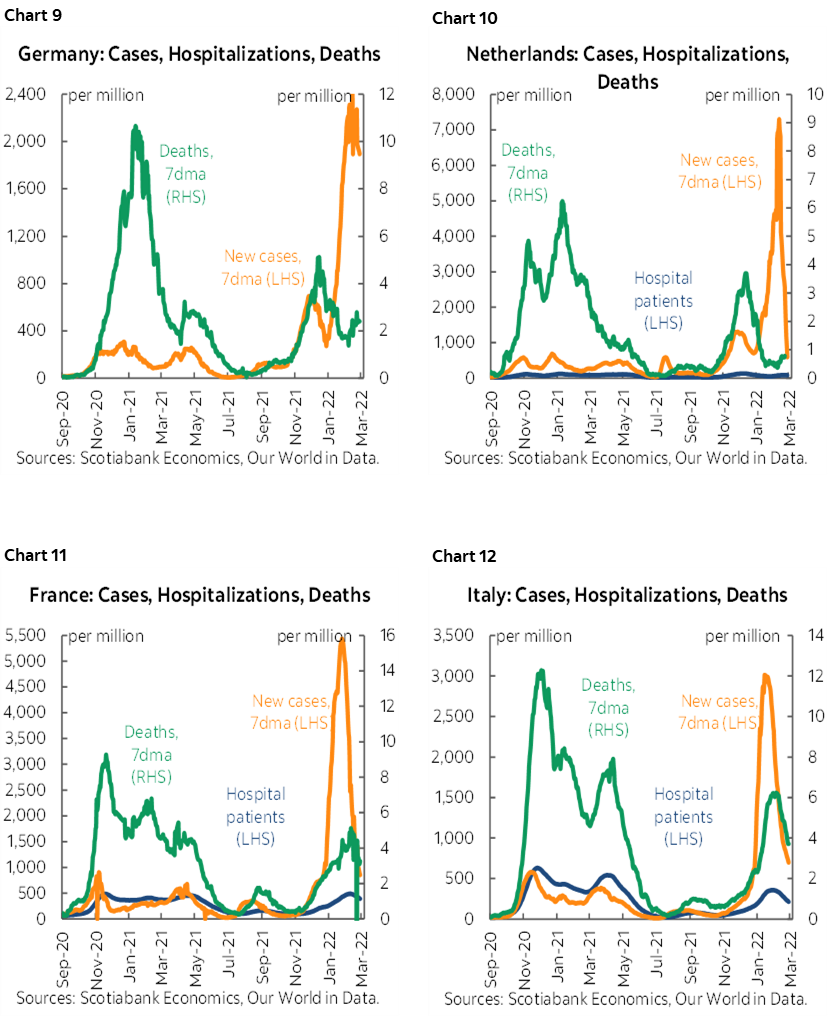

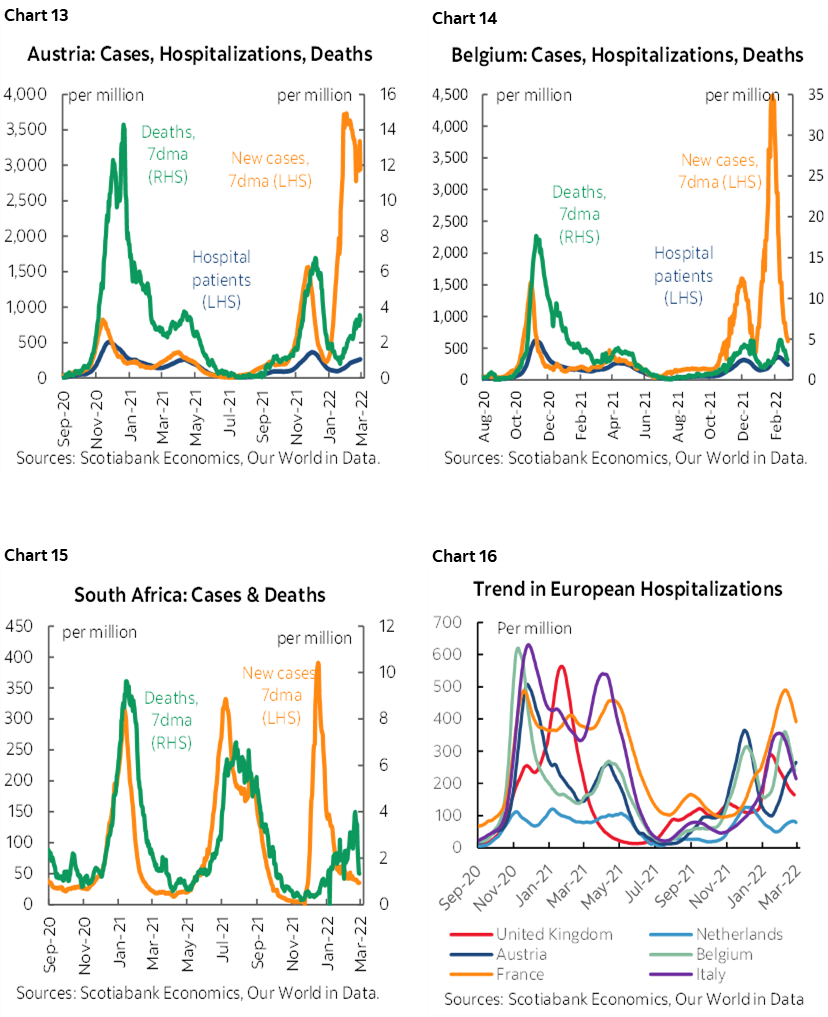

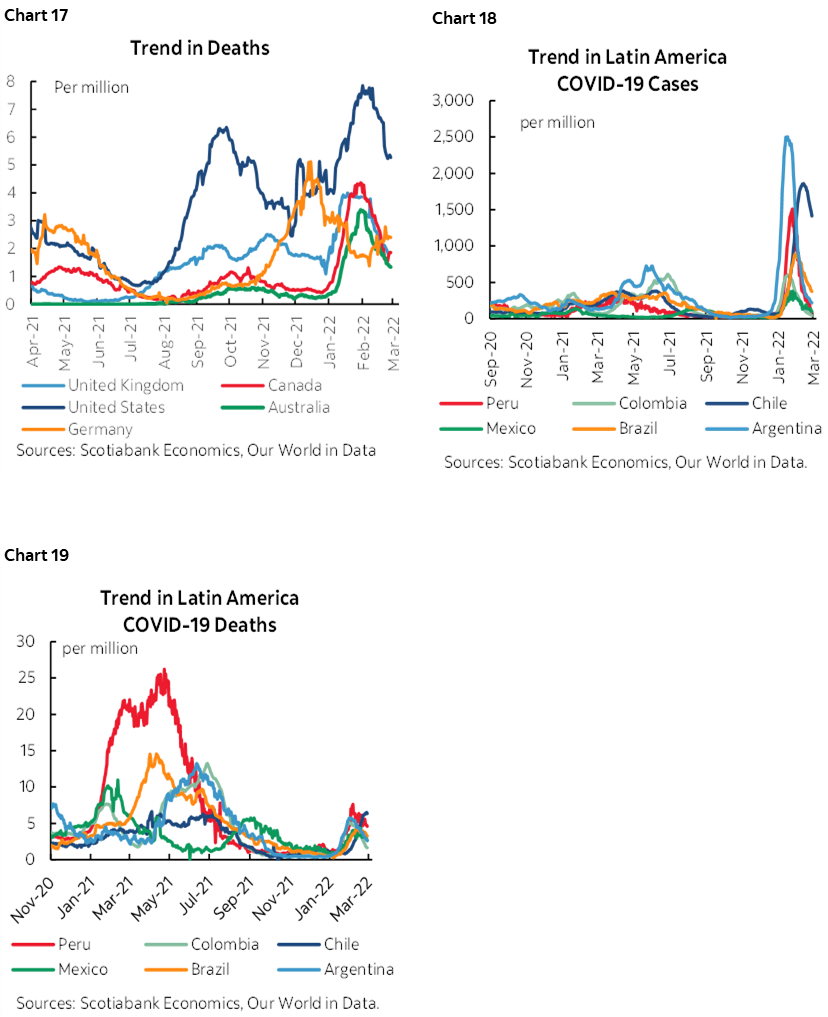

Lastly, the usual collection of charts covering global COVID-19 trends in hospitalizations and deaths is offered at the end of the note. In general, there continues to be growing evidence that the omicron wave is subsiding across multiple jurisdictions. As one risk has gone down, another is flaring.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.