ON DECK FOR TUESDAY, FEBRUARY 22

KEY POINTS:

- Markets take Russian provocations in stride

- Sanctions awaited, amid signs of mixed appetite for severity

- German business confidence builds upon global PMI signals

- US consumer confidence highlights US releases on tap

- Global COVID-19 charts

- Global Week Ahead

Developments to start a holiday-shortened week in most of N.A. are squarely focused upon Russia and Ukraine following Putin’s recognition of separatist regions in Ukraine and the dictator’s decision to send troops to those regions as an act of provocation that furthers his prior false flag maneuvers. The west is preparing sanctions, but with plenty of evidence of divisions and uncertainty toward how severe they may be. Russia’s foreign secretary was dismissive saying that “well, we’re used to it.” Germany has halted approval of the Nord Stream 2 pipeline which they arguably should have never allowed in the first place. Italy’s Draghi says sanctions need to be limited, targeted and should exempt gas given Italy’s dependence upon Russian gas. The EU, US and UK are preparing sanctions that may be revealed today, and the EU requires all member states to approve them.

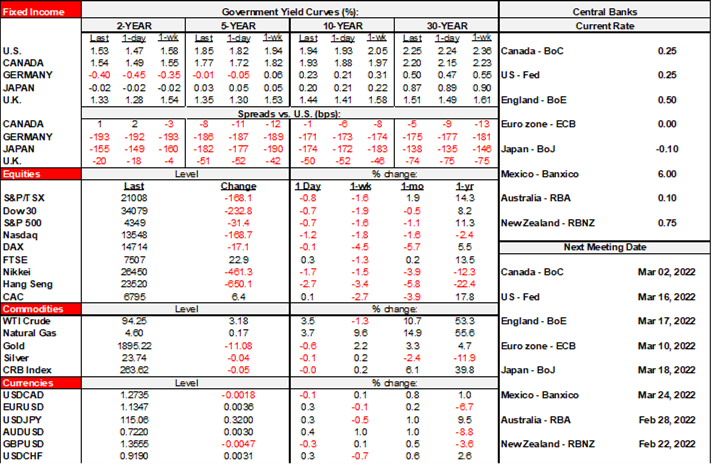

So far, the effects upon markets are relatively mild outside of oil’s inflationary impulses. Oil prices are up by about US$2–3 per barrel. US equity futures are down by up to ½% (Nasdaq) but the moves across the S&P500 and TSX are minor so far after yesterday’s -¾% declines by the S&P500 and the TSX. European cash markets range from down ¼% in Germany to up ¼% in London. US Treasuries are bear flattening with 2s about 6–7bps cheaper and the longer end is only slightly cheaper. Flattening moves are also driving gilts and bunds. The USD is slightly weaker this morning but generally little changed since Friday’s close despite the developments in Ukraine.

For Canadians and Americans returning from the long weekend the only other updates included a round of global PMIs that arrived yesterday morning and on Sunday evening. They showed encouraging signs in support of an omicron rebound with improvements in the Eurozone, UK and Australia, while Japan fell. They are nevertheless being treated as stale given the geopolitical developments.

The only overnight release was Germany’s IFO business confidence for February that posted significant improvements to current and expectations components.

On tap today will be a few US releases with the main emphasis upon the Conference Board’s measure of consumer confidence (10amET). US Markit gauges are due shortly before that, but are not widely followed partly because Fed prefers the ISM measures that are geared toward the domestic US economy and hence the Fed’s mandate.

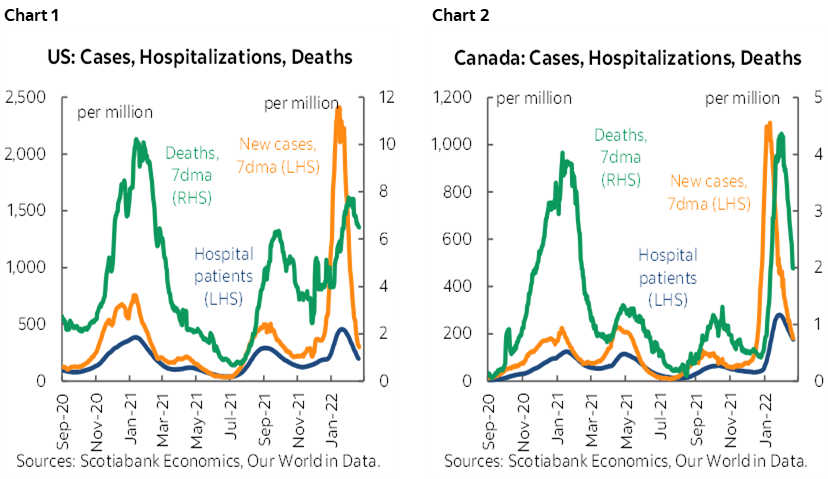

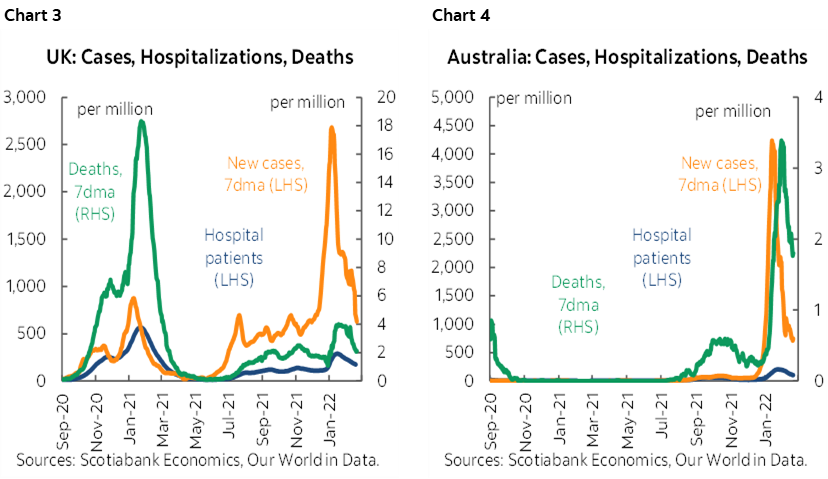

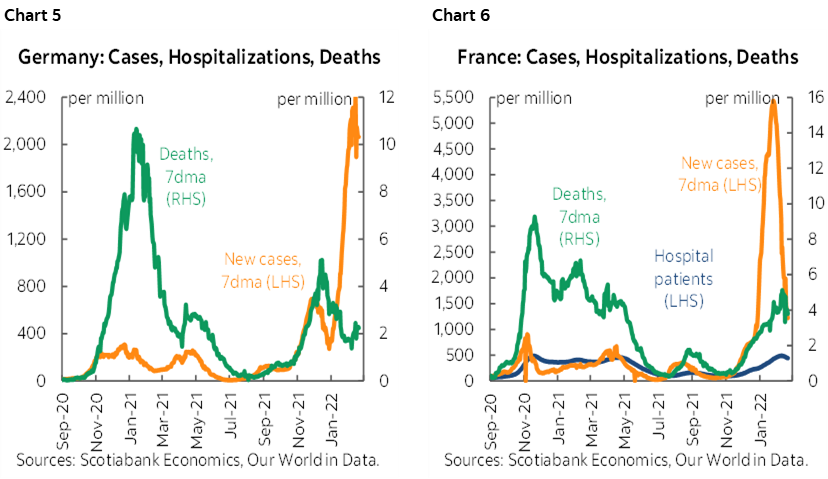

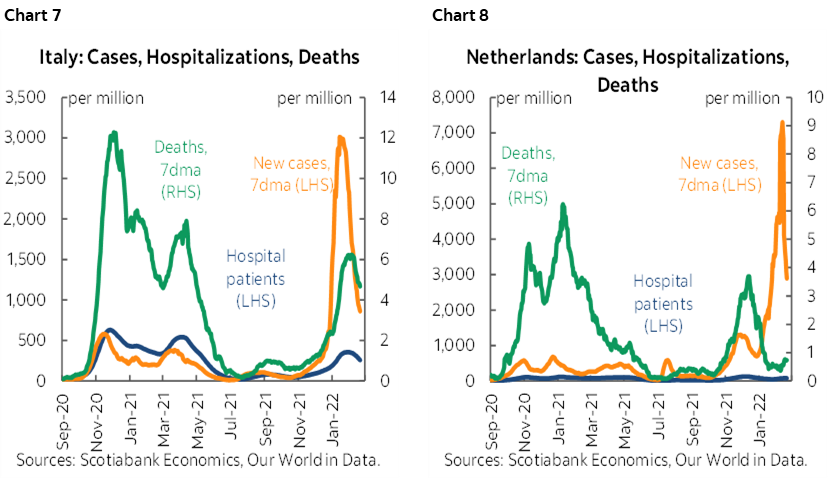

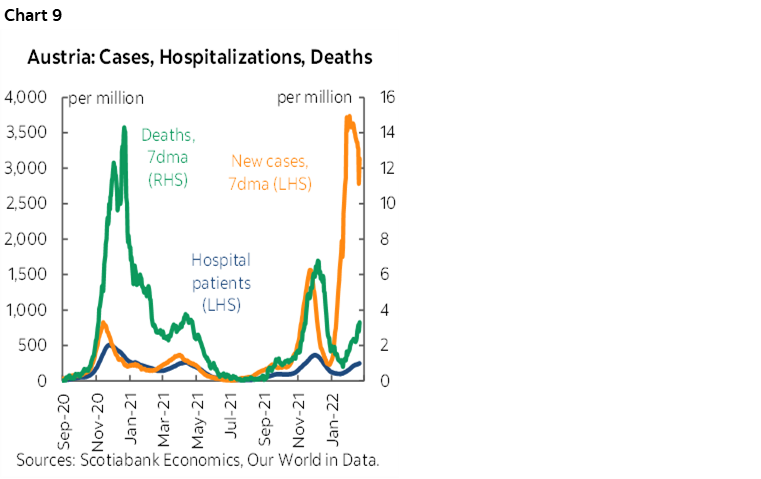

Please see the weekly update of global COVID-19 trends in hospitalizations and deaths that continue to decline in several major regions.

Please also see the Global Week Ahead here and your inbox for the related chart deck. The deck was updated to account for developments into Monday evening.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.