ON DECK FOR WEDNESDAY, MARCH 17

KEY POINTS:

- Global markets have their colours mixed up today

- Fed: Forecast upgrades…

- …could push at least some dots higher, earlier…

- …offset by emphasis upon the long dual mandate road ahead

- The Fed’s insulting inflation narrative

- Powell’s presser & the Supplementary Leverage Ratio

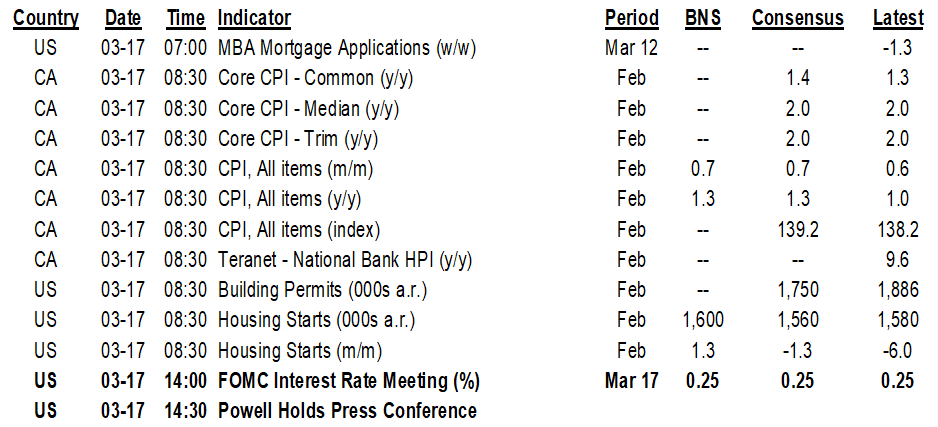

- CDN CPI: higher headline, core uncertain

Happy St. Paddy’s Day!

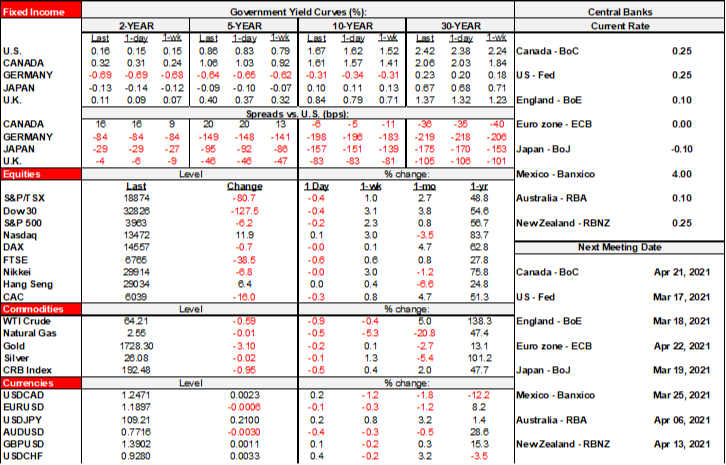

But my, you are all being verrrry bad Irish(wo)men. Tisk tisk. I would have expected you to be driving a sea of brilliant emerald green across my screens this morning. There had better be some green tea on those desks (or maybe green beer in the case of our friends in Asia)! Alas, ahead of the Fed, stocks are playing a bit of defense, sovereign yields are higher with curves bear steepening across most major markets, the dollar is little changed on balance, but CAD, the Mexican peso and other commodity crosses are losing a bit of ground with oil off by under 1%. We’ll see about conditions after the Fed.

The Fed will clearly be the focal point today and before that we’ll get an update on Canadian CPI to pass the time in the background. Overnight developments were otherwise thin. The German government revised growth guidance to be slightly lower at a still rather respectable 3.1–3.7% this year and 4% next year which despite the doom scrolling is still in the ballpark of most expectations. Japan’s PM Suga indicated that Tokyo’s lockdown would lift on Sunday; rather hard to prepare for the Olympics otherwise…

UNITED STATES

The Fed statement, Summary of Economic Projections and dot plot arrive at 2pmET followed by Chair Powell’s press conference at 2:30pmET. The last forecasts were issued in mid-December and developed even before that. Today’s will raise GDP projections at least for 2021 on the back of two huge fiscal packages and major vaccine progress in the US. The dots could see a few more join the 2023 hike camp but probably not enough to swing the median toward a hike. The statement and presser are likely to acknowledge the upside developments while still flagging 9.5 million unemployed and being shy of inflation goals.

They’ll repeat that we should all simply ignore inflation’s rise as just a year-over-year base effect phenomenon with nothing to see, nothing to fret about here, inflation is going to charge right back down so #stimulusforever. Hogwash. Most of us should instead be looking at higher frequency gauges, like seasonally adjusted month-ago core measures and with greater uncertainty in mind toward inflation drivers not just into Spring but within the 1–2 year monetary policy horizon. US real GDP is forecast to fully recover the pandemic shock by next quarter. Spare capacity is shutting faster than Trump’s net worth is falling. The Phillips curve is flatter, not dead. Full employment is attainable within the monetary policy horizon. Powell’s low inflation arguments are rooted in views drawn from the past that may well be changing and in the context of ginormous stimulus. The FOMC’s don’t worry be happy line is merely about buying time in my view and I’m sure they know full well that adjustments are ahead. The stimulus put in place about a year ago now was for a depression scenario which this is not. The FOMC has already accommodated a whisper taper that makes an actual taper easier to deliver. The EM asset effects of a whisper taper are starting to be felt as guided. The path toward tapering purchases as soon as later this year, more likely early next year remains intact and it will be a lot easier to deliver with markets adjusting toward that path.

Also watch for possible discussion in the presser on the Board of Governors’ stance on what to do with the supplementary leverage ratio’s month-end expiration of the exclusion of Treasuries and deposits held at the Fed which could be the considerably more important nearer term Fed consideration along with guidance toward other possible tools into a likely further liquidity overshoot (IOER hike, raise overnight reverse repo counter-party limits, etc). See the Global Week Ahead for more (here).

CANADA

Before that we’ll get Canadian CPI. Spare a couple of minutes to think about the BoC today before the Fed takes over. Don’t look for a repeat of the CPI revision fiasco, at least for a while. Gas prices and seasonality should pop headline NSA CPI higher by about 0.7% m/m. When combined with base effects, that should be enough to raise headline from about 1.0% to 1.3% y/y. Two out of the three core measures are likely to hang in around the unchanged 2.0% y/y mark so the key will be whether common component remains as much of a downside outlier at 1.3%. The average is already running at 1.8% y/y and there is some debate at the margin about which measures of core are truly best. Like the Fed, the BoC put in place ginormous stimulus for a world before vaccines were expected and when it was common to assume that fiscal policy would fail as it has in the past. Neither assumption remains valid. So why all the long faces talking about long rate holds and buying bonds until the proverbial cows come home? Helllllo April.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.