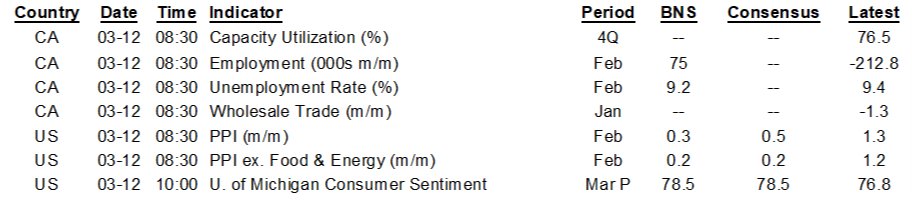

ON DECK FOR FRIDAY, MARCH 21

KEY POINTS:

- Markets have already forgotten about the ECB

- Will CDN jobs rebound?

- The UK lockdown hit wasn’t quite as bad as feared

- US core producer price inflation is already accelerating

- US UMich consumer sentiment on tap

INTERNATIONAL

What’s the good news? Well, the clocks go forward Sunday in this part of the 'hood (two weeks later in Europe), so you’ll get an extra hour of daylight in the evening. The bad news? The clocks go forward Sunday, so you’ll ‘lose’ an hour of sleep and the markets are not looking so hot to end the week. Let’s hope Canada’s jobs tally can provide a lift to sentiment this morning! In the US watch for further inflation signals.

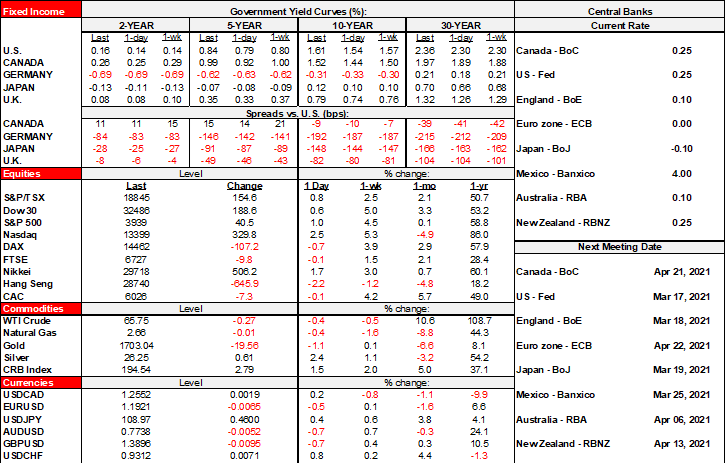

- The USD is broadly stronger and the DXY has reversed yesterday’s weakening with CAD outperforming most other crosses.

- Sovereign curves are steepening again and led by US Ts, gilts and Canadian yields that are all 5–8bps cheaper toward the longer end. Yesterday’s modest reaction to the ECB has been either entirely or largely unwound across most EGBs. See yesterday’s note for why the ECB underwhelmed.

- Stocks are a little softer on balance with Nasdaq futures leading the sharpest decline.

UK macro data reflected lockdowns in January but on balance was not as bad as feared. Overnight releases posted a 1.5% m/m drop in industrial output led by manufacturing, a 3.5% decline in services, an unexpected 0.9% rise in construction output and a wider trade deficit. Monthly GDP shrank by 2.9% which was better than the consensus estimate of -4.9% as all but three out of 31 economists thought the number would be worse.

CANADA

Well what a fine way to end the week with the Canadian jobs lottery!

I take zero comfort in the fact that my early guesstimate for +75k in today’s jobs report for February (8:30amET) is exactly where consensus landed. I think there is more upside than downside based upon what little we can track into it, but the much stronger numbers are likely later. The point is about the direction after Canada lost 213k jobs in January due to COVID-19 restrictions particularly in Ontario and Quebec. The slightly trimmed range of estimates for today is about +25k to +200k. The 95% confidence interval on the Labour Force Survey’s jobs estimate is +/- 57,600, so statistically speaking our guesses won’t face a statistically significant hit/miss unless we’re getting down toward no change or a drop or above around 130k.

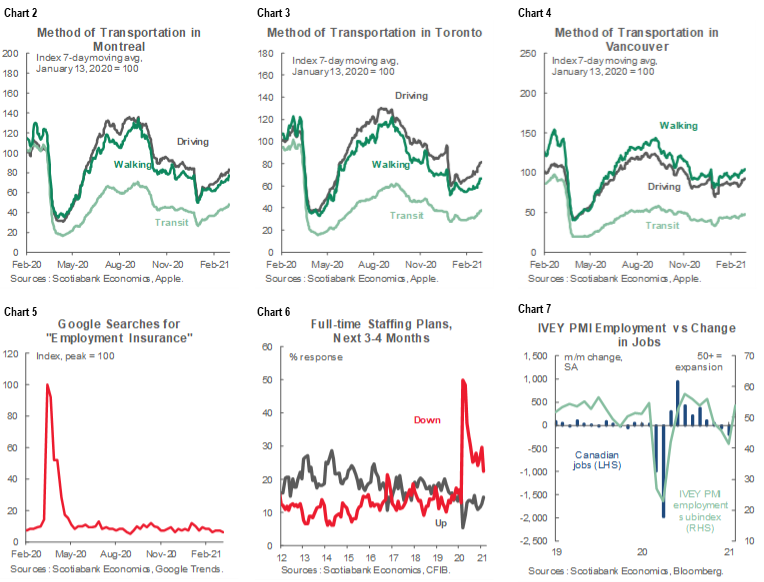

Canada has far fewer advance signals on jobs than the US, but here’s what we can point toward, as previously written in the week ahead article:

- Ontario/Quebec relaxed some restrictions between LFS reference periods which in this case is the difference between the week of February 15th–19th and January 11th–15th.

- The BoC’s new high frequency provincial stringency indices that measure restrictions confirm this easing into the February reference week (chart 1).

- Mobility readings picked up by more than the improvement in the stringency indices in the biggest cities of Toronto, Montreal and Vancouver (charts 2–4). The measures had generally gotten back toward last Fall’s levels before second wave clampdowns.

- Google searches for employment insurance program info were flat to slightly lower (ie: no increase in cuts). See chart 5.

- Small business hiring plans over the next 3–4 months improved a bit (chart 6).

- The Ivey employment subindex sharply rebounded in February from below-50 readings that signalled employment losses to +54 for the hiring index in February (ie: renewed growth in hiring, but unweighted). See chart 7.

UNITED STATES

US releases will be light and focused on producer prices during February (8:30amET) and the University of Michigan’s consumer sentiment reading for March (10amET).

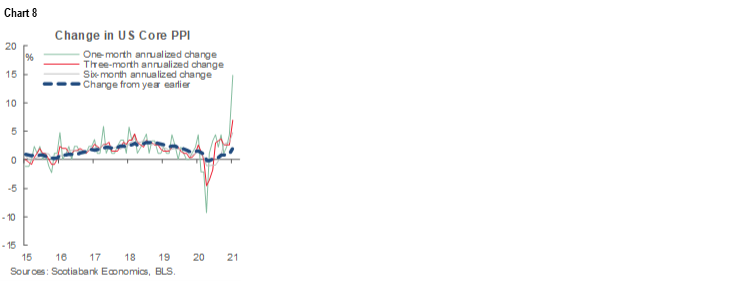

Core producer prices are expected to accelerate by the fastest pace since early 2019 and not just due to base effects as the prior month had registered a 1.2% m/m jump for the fastest rise in many years. Chart 8 shows the sharp recent acceleration in producer prices excluding food and energy which generally confirms guidance in surveys like the ISM reports that indicate rising price pressures across supply chains.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law