ON DECK FOR FRIDAY, JANUARY 8

KEY POINTS:

- Dollar, Treasuries guarded, stocks up

- US nonfarm payrolls likely stalled out in December

- Fed’s Clarida to weigh in with updated outlook

- Canadian jobs: downside risk in both December & January reports

There are three main things to watch this morning after largely inconsequential overnight European releases. They are flagged below.

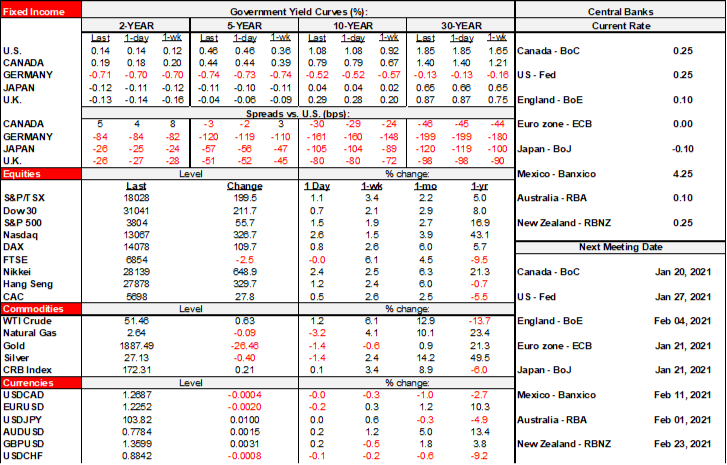

- US equity futures are in the black again with a rise of ¼% to ½% across exchanges. Toronto is mildly higher. European exchanges range from flat in London to up by as much as ¾% in Frankfurt.

- Sovereign bond yields are little changed with mild exceptions including slightly richer Canadian 10s and Italian spread narrowing over bunds.

- The USD is little changed and so is CAD ahead of dual jobs reports.

- Oil is up again by about 1½%.

Overnight European releases were largely inconsequential to markets as they speak to lagging November readings in the face of forward-looking risks. Still, German data was strong, French not so much. German exports were up 2.2% m/m (1% consensus) for the seventh consecutive solid gain. German industrial output was up by 0.9% m/m in line with consensus but with a mild upward revision and this also marks the seventh straight monthly gain.

French consumer spending plummeted by about 19% m/m in November on the nationwide lockdown effect. Industrial production also fell by 0.9% m/m that month.

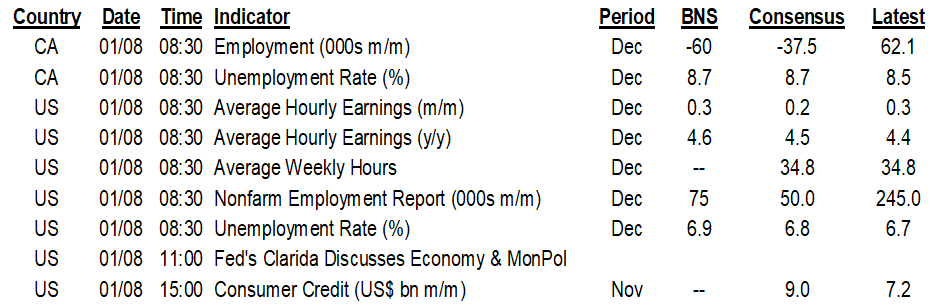

Here are the three main things on tap. The main focus is on US & Canadian jobs reports as restrictions tighten (chart 1).

1. Nonfarm payrolls (8:30amET)

Consensus 50k, Scotia 75k, trimmed range is about -100k to +150k, whisper number is 45k. The 90% confidence interval for nonfarm estimates is +/- 110k so noise always figures prominently. That job market momentum stalled out is clear. Chart 2 shows that jobs became harder to get according to the jobs plentiful gauge in consumer confidence. Chart 3 shows that initial jobless claims backed up between November and December reference periods (but have since fallen back). Chart 4 shows that ISM-services indicated weaker hiring activity. Chart 5 illustrates that job openings have stalled out. Chart 6 is a reminder that it would be statistically improbable for nonfarm to be positive after the magnitude of the ADP decline of 123k last month; the left side of the chart shows the low frequency of observations attached to a spread like -123k for ADP and the nonfarm consensus of +50k since ADP revised its methodology in October 2010. There is a single digit percentage chance that nonfarm comes in as high or higher than consensus thinks; the problem is that all of the data points behind that low probability are concentrated in this year as ADP has generally undershot nonfarm payrolls.

2. Fed’s Clarida (11amET)

The Fed’s #2 speaks on the US economy and monetary policy in a conversation at the Council on Foreign Relations. Key may be whether he reinforces recent taper talk from some FOMC speakers (e.g. Kaplan, Bostic) but I suspect he’ll lean more toward Bullard’s answer that indicated it’s too early to address this. A lot has happened since Powell spoke in mid-December and so his remarks on the outlook and risks may be meaningful. Several positive developments have included passing the Brexit deal, getting the US stimulus deal passed, the ‘blue wave’ and market moves like a further rise in inflation expectations. Confidence in vaccines, however, has been dented until we get the results of trials against the London and South African mutations into a February/March timeline.

3. Canadian jobs (8:30amET)

Consensus -38k, Scotia -60k, highly scattered range from around -125k to +31k. Notwithstanding a 95% confidence interval of +/-58k (90% at +/- 46k), I lean pretty strongly toward a negative. Key is the timing of restrictions that hit just after the prior month’s reference week that includes the 15th of each month. January’s job report is also likely to face downside risk on further restrictions and because Ontario’s extended school closures will go right through the Labour Force Reference week and probably have a particularly negative impact upon working moms as evidenced the first time around.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.