ON DECK FOR WEDNESDAY, JANUARY 13

KEY POINTS:

- Bonds richen in cautious markets

- US core CPI holds steady for a 6th straight month…

- ...as emergency deflation risk is well behind markets…

- ...while a vaccine and stimulus fed recovery are forecast to challenge the Fed’s revised goals statement in 2022

- Fed’s Clarida likely to repeat a more positive bias…

- …while continuing to lean against early taper…

- …in a speech on consequences to the Fed’s new framework

- US impeachment in the House is likely to fizzle in the Senate

INTERNATIONAL

Global risk appetite is muted this morning following nothing by way of overnight developments and ahead of soft calendars into the North American session. There were no meaningful developments overnight.

- Equities are mixed with the S&P500 flat so far while the TSX is marginally lower. London is flat while small gains of ¼% or slightly firmer are being booked across the rest of Europe.

- Sovereign bond curves are a bit flatter especially in Europe. 10 year yields are down by up to 4–6bps in gilts, bunds and French bonds, and 2–4bps lower across the US, Canada and elsewhere in Europe.

- The USD is a touch stronger against most major currencies.

- Oil is flat and so is gold.

UNITED STATES

US developments start to heat up today and will continue to do so over the duration of the week. Today brings out slightly softer core CPI than anticipated for December and Q4, ongoing Fed-speak with the focus today primarily upon Vice Chair Clarida’s remarks later in the day, and impeachment proceedings that are likely to be mostly symbolic in nature.

US CPI headline, m/m % / y/y %, Dec:

Actual: 0.4 / 1.4

Scotia: 0.3 / 1.3

Consensus: 0.4 / 1.3

Prior: 0.2 / 1.2

US core CPI headline, m/m % / y/y %, Dec:

Actual: 0.1 / 1.6

Scotia: 0.2 / 1.7

Consensus: 0.1 / 1.6

Prior: 0.2 / 1.6

US core CPI inflation held unchanged at 1.6% y/y and 0.1% m/m during December. Core CPI has been stuck at 1.6–1.7% for about six months with inflation risk remaining a future story. Core CPI averaged 1.3% y/y in 2020Q4, a tenth lower than our revised forecast issued yesterday. Still, however, that’s a lot more resilient than some had feared when the pandemic first struck and given the tendency to dredge up deflation talk every time an ant sneezes. 1.6% core inflation is not deflationary, but it also doesn’t put any pressure on the Fed’s dual mandate either—yet.

Inflation is going to be more of a story over the next couple of years with various drivers. That’s likely why market-derived inflation expectations have moved as much as they have. Among the drivers may well be when explosive growth in money supply combines with a recovery in velocity as GDP recovers. Chart 1 shows broad money is growing at the fastest pace in at least six decades and likely a lot longer than that given present data limits. Explosive growth in broad money is occurring as the Fed’s balance sheet aggressively expands absent the countervailing forces of broad money destruction in the depths of the GFC. Limiting the pass through of aggressive money supply growth into prices is that velocity has fallen naturally because GDP plunged so much in Q2, but given it is GDP over money supply, velocity could well rebound alongside GDP while growth in money supply wanes but the level remains exceptionally high. Now if the pandemic is a transitory shock (mind you, a really bad one) that vaccines snuff out, then unprecedented monetary and fiscal policy stimulus with more of the latter ahead in the Biden administration could well combine to achieve higher inflation.

In yesterday’s revised forecasts, we anticipate core PCE inflation to rise to over 2% y/y next year and thus to begin challenging the Fed’s revised goals statement that signal a willingness to tolerate marginally above-2% inflation for a modest time period. That’s one reason we have short market rates materially rising over our forecast horizon even if the Fed doesn’t hike until their scout’s honour pledge says so. We anticipate a gradual move away from emergency conditions with greater distance from deflationary risk that should drive cheaper Treasuries over time notwithstanding near-term tactical risks.

Chart 3 shows core CPI likely means core PCE remains stuck at about 1.4% y/y when we get PCE at month-end. That remains well below the Fed’s revised long run goals statement that aims for inflation “moderately above 2 percent for some time” before tightening policy. For now.

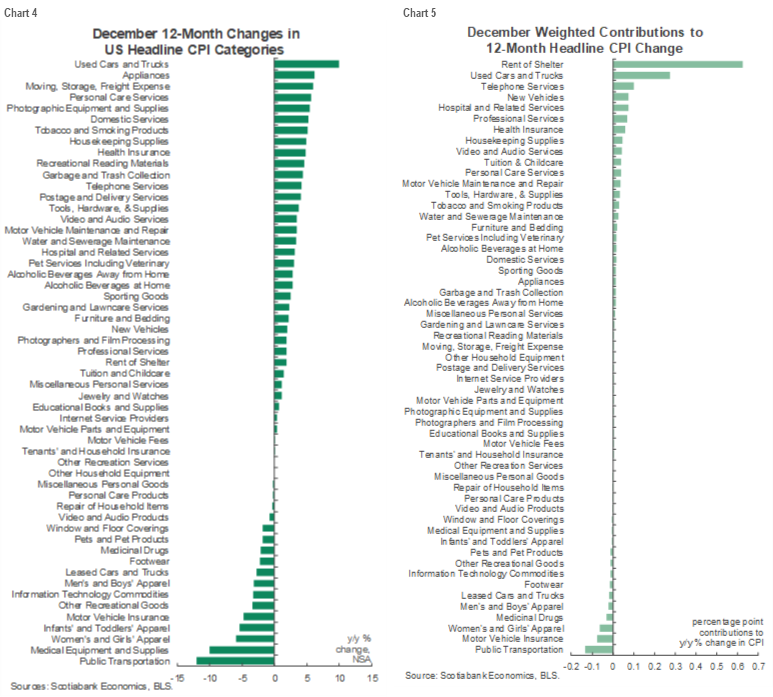

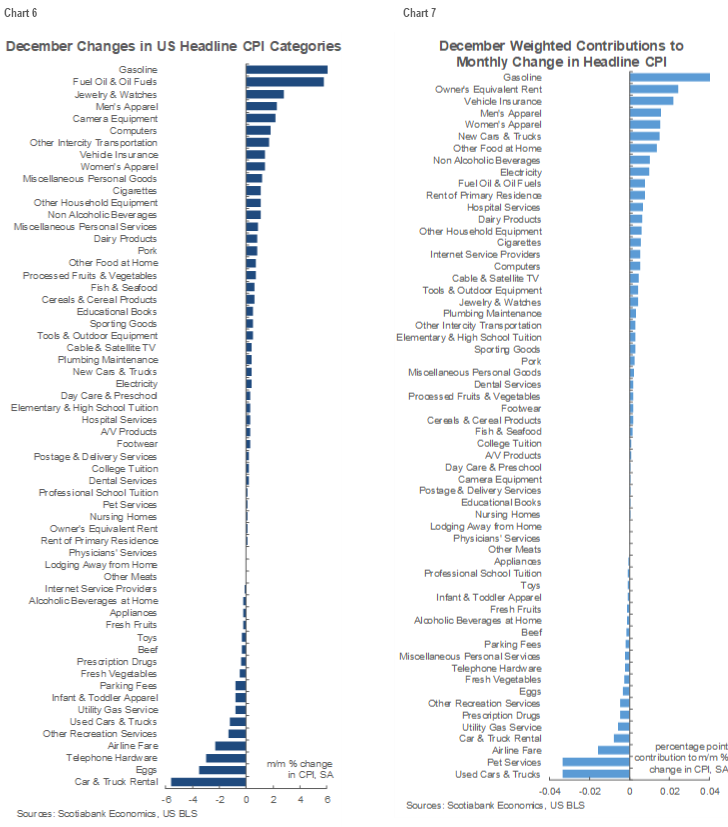

Chart 4 provides a break down of the year-over-year changes across individual components within the CPI basket. Chart 5 does the same thing on a weighted contribution basis and it shows that housing and vehicles are the top drivers of inflation. Chart 6 shows the CPI changes in month-over-month seasonally adjusted terms while chart 7 does the same thing on a weighted contribution basis.

While the Fed’s Beige Book (2pmET) will be largely ignored by markets as a set of regional anecdotes, greater attention may be placed upon Federal Reserve Vice Chair Clarida who speaks at 3pmET on the Federal Reserve’s new framework and its consequences. I suspect he’s likely to repeat that “the downside risk to the outlook has diminished” as he stated on January 8th, but to also repeat that “My economic outlook is consistent with us keeping the current pace of purchases throughout the remainder of the year” notwithstanding the fact that some regional Presidents (e.g. Bostic, Evans) have indicated openness toward tapering by year-end.

The US House of Representatives’ impeachment vote is likely to occur toward the market close this afternoon and is expected to pass. Then it’s a matter of whether the articles of impeachment go straight to the Senate or are delayed until the Democrats take control with the pending changeover in Congress. Either way, two-thirds support is required in the Senate trial which means it’s unlikely to occur.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.