ON DECK FOR FRIDAY, FEBRUARY 26

KEY POINTS:

- Global central bankers diverge into G20 meetings

- BoE’s Haldane warns on inflation, gilts frown

- ECB’s Schnabel follows Lane on bond warning

- RBA exerts control over 3s target in broader steepening

- US House starts the horse trading on path to stimulus bill

INTERNATIONAL

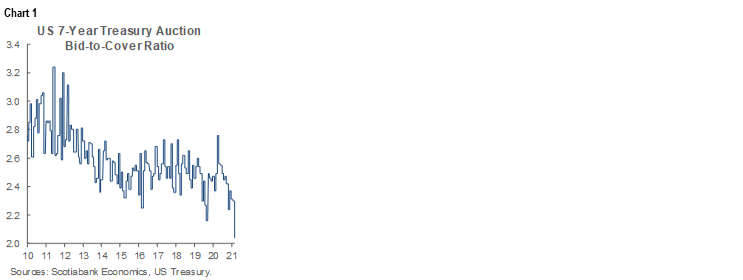

There is a bit more variety across central bank perspectives toward the bond market this morning and it’s driving some divergence across markets. This follows yesterday’s yield spike that was in place prior to but aggravated by the weak 7s auction (chart 1). The narrative on the bond market changed markedly post-US election, as momentum built toward two US fiscal relief bills within three months of one another that add around a dozen points of nominal GDP to the picture and as vaccine take-up has become much more positive in the US. A booming US consumer lies ahead. This remains, in my view, a fundamentals-led cheapening with technical factors following.

On what we are hearing from central banks into this morning it’s either that they are uncoordinated as a group into the G20 finance ministers and central bankers meeting today into tomorrow, or merely speaking toward local conditions. I think it’s a bit of both and one shouldn’t expect a unified stance toward the bond market out of the G20.

For one thing, no other central bank faces as material a pick-up in fiscal policy combined with as much progress on vaccines as the Federal Reserve and so that perhaps explains its complacency toward the bond selloff. The BoC has adopted a similar line. What about the others? Markets are being influenced by remarks and action by three other central banks this morning.

The Bank of England’s Chief Economist Andy Haldane drove yields higher across the curve this morning when he warned:

“There is a tangible risk inflation proves more difficult to tame, requiring monetary policymakers to act more assertively than is currently priced into financial markets. People are right to caution about the risks of central banks acting too conservatively by tightening policy prematurely. But, for me, the greater risk at present is of central bank complacency allowing the inflation (big) cat out of the bag.”

I’m with him, at least across the Anglo-American markets.

Over at the ECB, Executive Board member Schnabel followed up yesterday’s remarks by the ECB’s Chief Economist Lane about being flexible with the PEPP with her own warning that there is a limit to what the ECB will tolerate via higher yields. She argued that higher real long-term rates “even if reflecting improved growth prospects” could be premature and “Policy will then have to step up its level of support.” The Eurozone is behind on vaccinations, not facing the same fiscal impulse as the US and frankly more growth-challenged at the best of times. Still, even a powerful central bank faces its own limits on the upside of the global recovery slope if it seeks to interfere with where bond markets wish to go. My personal belief is that the ECB shouldn’t be worried about the moves in 10 year bunds or French 10s or Italian 10s that collectively are approaching pre-pandemic yields in the context of reasonable expectations for a stronger global outlook. That can hardly be labelled a clear overshoot.

The RBA again stepped up purchases at the 3-year section of the curve in a further attempt at enforcing its 0.1% target. This time it generally worked—sort of—by bringing the yield to about 0.1% whereas it had strayed above that target since February 17th and was stubbornly refusing to edge lower following prior efforts over recent days. Still, the curve massively bear steepened as Australia’s 10 year yield soared another 17bps and is up by about 110bps since November with accelerated selling since mid-February.

Overnight releases on the macro calendar were of little consequence.

UNITED STATES

US releases will be the main focal point on the macro calendar to close out the week as the US House of Representatives takes up the Biden stimulus package as a first step toward passing both chambers and reconciling differences before a bill lands on President Biden’s desk for signing before unemployment benefit extensions expire around a mid-March timeline. Personal income, consumption, the saving rate and the Fed’s preferred inflation rates will be updated with readings for January at 8:30amET.

Personal income growth will be very strong and despite spending some of that, most of it will be hoarded which is the typical pattern when stimulus is thrown out. Hoarded amounts sitting around in cash and near-cash holdings will be the stimulus gift that keeps on giving and their redeployment could well drive a very strong consumer.

I’ve estimated nominal personal income growth at +11% m/m SA in January. That’s based on the US$166B cost of US$600/pp stimulus cheques plus the extra US$300/week for just under 10 million unemployed Americans, as well as reasonable assumptions on other PI components.

We already know that US retail sales were very strong at 5.3% m/m which should pop nominal total consumer spending up by +/-3% given the way the retail control group translates into consumption and the assumption that more dominant services spending growth will be weak.

Given those two points, I figure the personal saving rate will spike to about 24% which would be the highest since May.

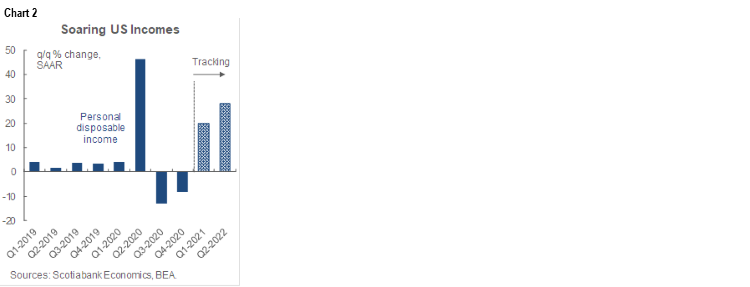

Factoring in assumed passage of the Biden bill in March and disbursements by April translates into forecast quarterly annualized consumption growth of 20% in Q1 and about 28% in Q2 (chart 2). April incomes could rise by toward 30% m/m. These would be the two strongest back-to-back quarterly gains in total personal income on record.

As for PCE and core PCE inflation measures, I went with a tick higher on PCE to 1.4% y/y (1.3% prior) but a tick lower on core PCE to 1.4% (1.5% prior) based on what we learned about CPI on the 10th, the composition of CPI relative to how it translates into PCE and slightly different base effects for PCE. I can’t see that mattering a whole lot as a backward looking inflation gauge in a forward-looking market.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.