ON DECK FOR WEDNESDAY, FEBRUARY 24

KEY POINTS:

- US, UK and Canadian long-ends explode

- FDA paves the way for J&J’s vaccine

- Macklem’s takeaways are consistent with the exit narrative

- The BoC puts far too much stock in house price expectations

- More Fed-speak to focus on Clarida’s US outlook

- US new home sales offer light data risk

INTERNATIONAL

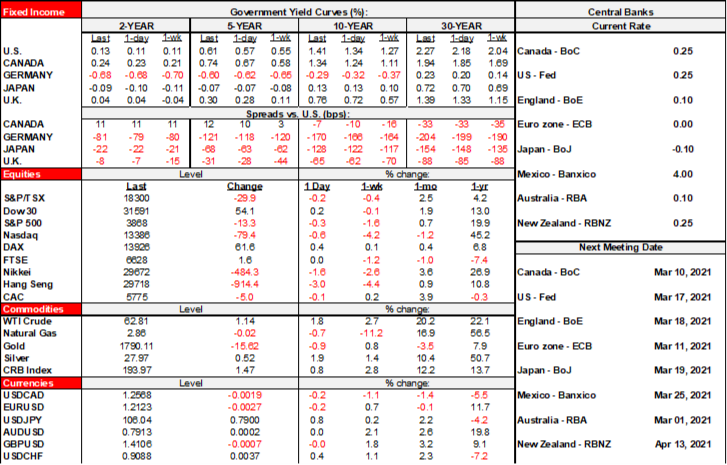

A combination of factors is driving sky high demand for buckets near the desks of rather pale-looking bond investors. The long end of the US Treasury curve is retching with central bankers cruelly hoarding stockpiles of breath mints. The 30 year yield is up another 7–9bps in the US, UK and Canada.

While the price action was already in motion beforehand, the FDA’s positive staff assessment of J&J’s vaccine (here) contributed to the spike in yields. The staff report was expected, but it paves the way for the FDA’s committee to give its blessing when it meets on Friday and to announce its approval shortly thereafter. This means 100 million US vaccinations at a one dose per person requirement by June. Delivery channels are also swinging into higher gear by the day; witness the announcement this morning that US drug chain CVS would expand delivery to six more states. Markets aren’t sitting around listening to fretting health authorities and slow footed central bankers and are instead pricing in the end of the pandemic starting this summer and through the second half of the year.

Central banks are complicit to the steepening in two ways. One is that they are sounding rather sanguine toward the price action further up the curve, as they arguably should given underlying drivers and the likelihood that trying to lean against powerful bond markets could prove rather embarrassing to central banks through the risk it backfires on them. Bond markets are in control here.

Second, central banks may be dragged by bond markets toward policy exits faster than their slow narratives may like if this kind of steepening continues. At some point the pendulum swings toward controlling upward pressure on the 30 year US mortgage rate and 5 year Canada rate by sounding less committed to prolonged holds. In the meantime, promising to sit on the front-end forever with narratives that are clinging to justification of emergency stimulus that was set in motion before vaccines and heavy fiscal stimulus is stoking inflation expectations. The argument that they can’t talk exits because that would risk market tightening too soon is contributing to the very market tightening that is underway further up the curve. Witness the spike in the US 10 year break-even around the FDA announcement to the contest 2018 levels that were the highest since 2014. It’s still bad to see so many unemployed, but the true emergency conditions marked by depression and deflation fears in the early stages of this pandemic are likely well behind us; emergency stimulus is not and that’s what has markets fussed.

UNITED STATES

Fed Vice Chair Clarida speaks twice on the US economic outlook and monetary policy, once at 1pmET before the US Chamber of Commerce and the second time into the Australian overnight at 4pmET. This might get a bit meatier on the outlook than Powell had to offer us today and in his repeat before the House tomorrow, but the broad narrative is likely to be the same on the key touchpoints. Ditto for Governor Brainard on maximum unemployment. Fed Chair Powell’s 10amET testimony before the House financial services committee is so far just the expected rewind of what he said yesterday that offered little by way of any fresh perspectives.

US new home sales beat expectations by rising 4.3% m/m in January (consensus 1.7%). The prior month’s gain of 1.6% was revised up to a 5.5% rise. The rise over the past two months is reaching toward the highs over the second half of last year which in turn had been the strongest readings since 2006. New home months’ supply stands at 4.0 which is about double what it is in the resale market (1.9). That, in turn, is a motivator to expand the housing stock in the face of tight resale offerings.

CANADA

Governor Macklem’s speech (here) and presser yesterday afternoon did not move the market dial, but that’s not to say we didn’t learn more about how the central bank is viewing things. Before offering a recap of what I thought were the salient takeaways, I’d say his comments were broadly consistent with the exit narrative. His remarks were consistent with assuming that BoC purchase programs are on their way out with a further gradual backing away into Q2 including ending the PBPP and/or going down to $3B/week for GoCs. My interpretation of his remarks is also consistent with forecasting a first hike in 2022Q4 that I'd still shave to face a higher risk of earlier rather than later. The broad narrative is intact but, like central banks, now we’re all watching vaccine roll-outs, data, endless fiscal stimulus and how behaviour responds. As this is happening, however, we're moving way past emergency conditions and on the gradual exit slope. Central banks and their risk management focus always lag markets on the way out.

Here are the offered takeaways from Macklem’s communications.

1. Macklem sounds increasingly confident in sustained growth over H2 into 22.

2. They assume full immunity by the end of the year under more conservative assumptions than the Federal government. Macklem tiptoed around why they are more conservative as a combination of being prudent through a risk management central banker’s perspective.

3. The BoC is significantly more concerned about housing risks but not in an overly alarmist way. Still, the BoC has transitioned from dismissing housing strength as just a release of pent-up demand from the early lockdowns and little to worry about to after seeing records across multiple housing metrics from sales to very tight inventories now saying we are starting to see some early signs of excess exuberance” in housing and “there are risks housing could get carried away.” Onto Spring...

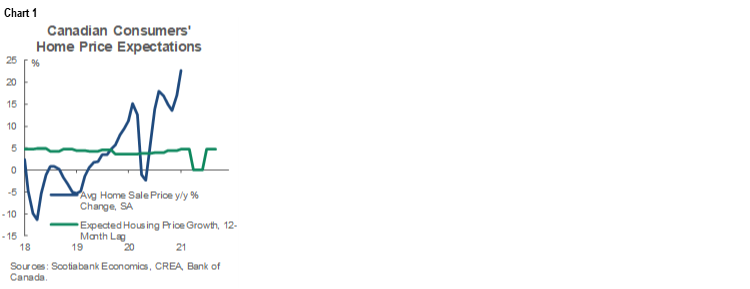

4. Still, Macklem hung his hat on the lack of evidence that consumers are getting carried away extrapolating expected house price gains in a sign of froth. There is a strong caution around their guidance on this count. Macklem is likely thinking about what the BoC’s consumer expectations survey indicates on this count (here). Their survey shows that consumers expect about 5% growth in house prices over the coming year. Apart from the issue that 5% exceeds inflation and population growth, the first caution is that the survey is rather stale as it was conducted from November 10th to December 1st and we’ve gotten a lot more information on the outlook since then. More important, however, is that consumers have a really bad track record at forecasting house prices as shown in chart 1 that compares one-year ahead house price expectations from this survey lagged a year to line up with what was delivered by way of actual house price growth. The BoC should take zero comfort in its survey after consumers said they thought house prices would rise by only about 4 ½% last year and instead they climbed by about four times that!

5. Macklem also reinforced that Canada is a long way off from a full recovery. In linking what this means to the policy rate, note the difference between when hikes start versus end. The point of a full recovery with zero slack, full employment and inflation on target should be where your policy rate is at neutral. The BoC’s estimate of neutral is a range from 1.75–2.75%.

6. Macklem repeated that the output gap doesn't shut until 2023. We have it shutting as soon as the end of this year. Note that the BoC almost always repeats what they said in the last MPR until the next one’s refreshed forecasts in that regard and the last one is arguably stale. We'll see in the April MPR.

7. Like Powell, Macklem says he's not fussed by curve steepening.

8. Macklem reinforced the messaging in January that they will gradually taper if the forecast evolves as expected. Yesterday’s cuts to the PBPP and (more symbolically) the CBPP are further steps in this direction toward reducing flows into bonds. I still think they should let the PBPP end on schedule in May as the underlying rationale for its existence has largely disappeared.

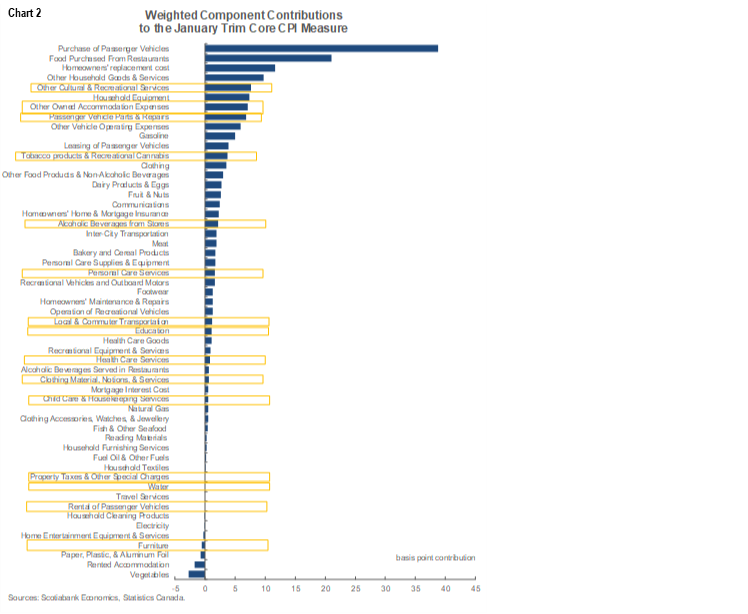

9. Macklem said that the flap over core CPI revisions by Statistics Canada doesn’t fuss the BoC. He noted that they target headline CPI which at 1.0% y/y wasn’t affected, they have high confidence in Statistics Canada while looking forward to working closely with StatsCan after admitting the BoC protested the changes. Chart 2 breaks down the components of the trimmed mean CPI measure of inflation and highlights the categories that were affected by the revisions. The revisions were caused by StatsCan’s decisions to stop seasonally adjusting 16 out of the 55 CPI components that go into calculating the core measures. In some cases there may be good reason for doing so, like for some administered prices that adjust in stepwise fashion. In other cases the rationale is less clear for ending seasonal adjustment of categories like furniture, clothing materials, car rentals, vehicle parts and repairs, etc. I think Macklem overstated the BoC’s sanguine approach to the issue in keeping with standing tradition for Ottawa’s various branches to avoid publicly criticizing one another. Again, stay tuned….

10. It was somewhat interesting that Macklem didn’t mention the currency once and not a single journalist in the presser thought to ask. Maybe that reflects an unwillingness to revisit the confusion that his earlier remarks on CAD sparked. In my view, the currency has done exactly what it should have done with the shift in the outlook and is a long way from having appreciated enough for any undesirable reasons to merit concern.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.