ON DECK FOR THURSDAY, SEPTEMBER 17

KEY POINTS:

- Fed drives risk-off sentiment…

- …with help from Washington’s stimulus divisions

- Sterling falls and gilts rally…

- …as the BoE inched closer to a negative policy rate

- · The whole gilts curve could shift lower yet…

- …if the BoE adopts ECB-style guidance

- BoJ, BI and SARB stand pat

- US claims and Philly maintain recovery evidence…

- …as housing cools a touch

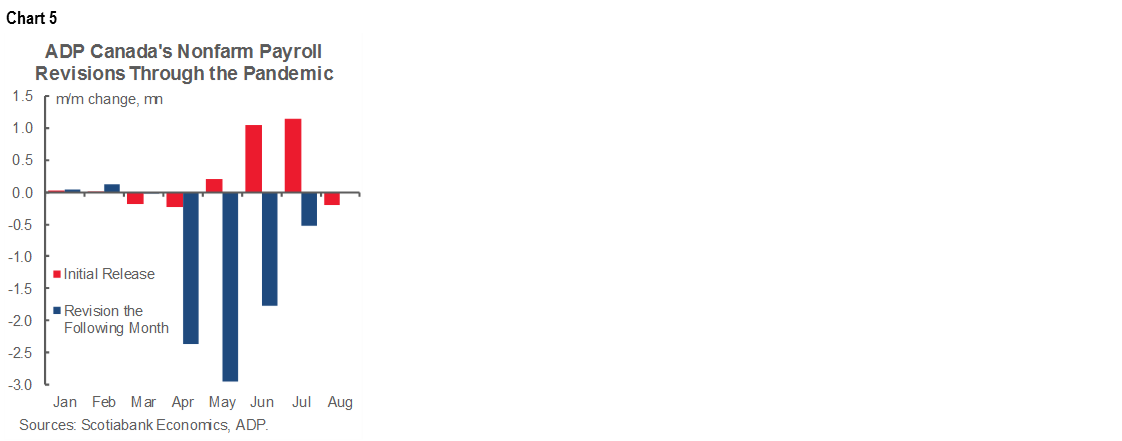

- ADP’s Canadian job stats messed up again

INTERNATIONAL

Well the Fed didn’t have any magic for markets yesterday and we’re seeing the more concentrated reaction this morning. As a reminder, please see yesterday’s take on why I think the Fed’s communications disappointed markets (here). What also doesn’t help risk appetite it the bickering within the GOP and between the GOP, White House and Dems over a further stimulus package that is looking less and less likely to be delivered.

Across the pond, the Bank of England did a better job at conveying its easing bias while ably tip toeing through the Brexit minefield. As noted below, if they were to actually implement a negative policy rate that is significantly priced at the front-end, there may be further potential to flatten the gilts curve if they copy ECB forward rate guidance to go with a negative policy rate. Other central banks figured they’d keep to the sidelines for varying reasons from can’t do much more (BoJ) to currency instability (Indonesia). US macro data wasn’t enough to swing the materially needle in any direction and Canada’s data was a downright joke.

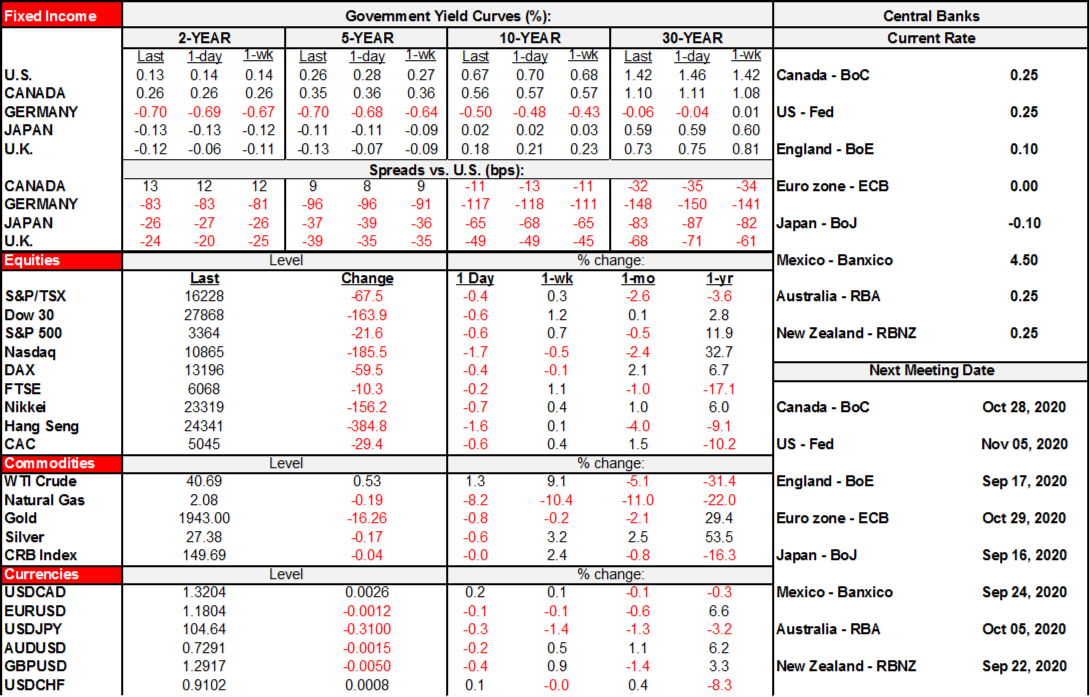

- Equities are pushing lower. US equities are down by ½% to 1¾% across the exchanges. The TSX is opening around 0.4% lower. European cash markets are lower by about ½% with London faring a little better on sterling weakness and Italy faring a little worse. Asian equities broadly sold off by between ¾% and 1 ½% within mainland China’s exchanges faring a little better.

- The USD is mildly firmer but past its peak rate of appreciation that was set in the overnight Asian session. The dollar is particularly strong against sterling post-BoE but CAD and the Mexican peso are also lower.

- Sovereign curves are rallying pretty much everywhere this morning. Gilts are outperforming mainly at the front end as the yields on 2s through 5s are down 6bps. 10s are down 3-4bps in the US and UK with Canada’s curve rallying by a little less than US Ts. 10 year EGB yields are marginally lower in core Europe.

- Oil prices are up by almost 2%. Gold is off by under 1%.

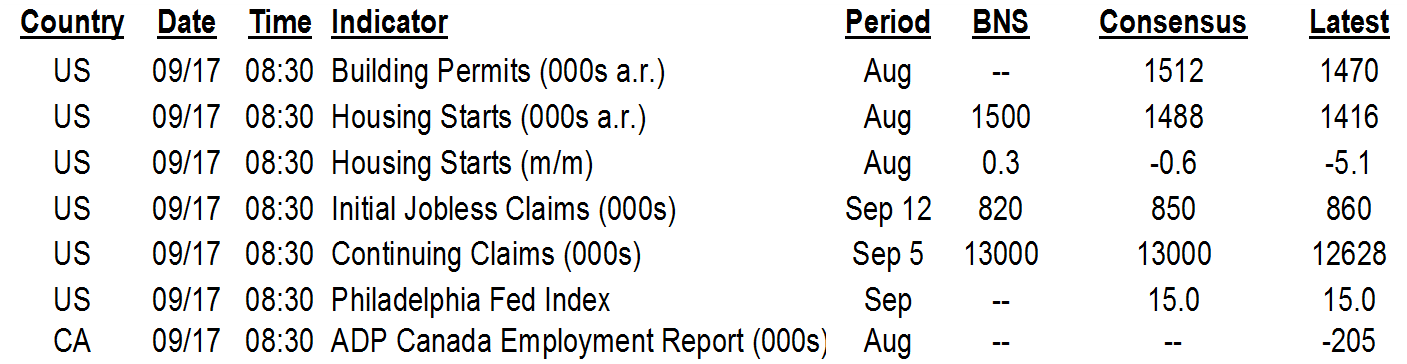

The Bank of England drove sterling to depreciate, gilts to rally and the Sonia OIS curve to further price prospects for a negative policy rate (chart 1). Not bad for a day’s work I’d say. What did the trick was the following line in the accompanying minutes (here) to the statement itself (here):

“The Committee had discussed its policy toolkit, and the effectiveness of negative policy rates in particular, in the August Monetary Policy Report, in light of the decline in global equilibrium interest rates over a number of years. Subsequently, the MPC had been briefed on the Bank of England’s plans to explore how a negative Bank Rate could be implemented effectively, should the outlook for inflation and output warrant it at some point during this period of low equilibrium rates. The Bank of England and the Prudential Regulation Authority will begin structured engagement on the operational considerations in 2020 Q4.”

Taking steps since the August MPR to explore details on implementation is a requisite tactical step toward having the flexibility to implement a negative Bank rate without necessarily doing so. OIS markets are now priced for a decline in the 0.1% Bank rate to slightly negative territory as soon as November and are priced for a -20bps rate about a year from now.

What may not be fully priced, however, is a further evolution toward negative rates across more of the gilts curve. The curve is negative out toward the belly of the curve but still positive 17bps in 10s and about 40bps in 15s by contrast to negative yields across the bunds and French curves. How could more of the curve rally toward more deeply negative rates into the belly and into negative rates beyond? Key here is the guidance and its credibility. Recall that the ECB emphasizes that curve control stemming from negative rates depends critically upon the commitment to keep rates “at their present or lower levels.” The ECB has emphasized the importance of removing the market’s inclination to view a negative policy rate as only facing the risk of increases which would drive a positive yielding curve slope. Introducing more ambiguity about future directions drove the whole EGB curve lower along with the effects of QE purchases and liquidity programs.

Australia unexpectedly gained 111,000 jobs (consensus -35k) and the prior month’s rise was revised up by just under 5k to 119k. Australia has regained about 52% of the 875k lost jobs due to the pandemic. The A$ barely budged overnight and the Australian rates curve shed about 1-2bp of yield across maturities.

The Bank of Japan left all policy variables unchanged with one dissenter but mildly upgraded its forecasts.

Bank Indonesia met expectations and kept its policy 7 day reverse repo rate unchanged at 4%.

The South African Reserve Bank somewhat unexpectedly held its policy rate at 3.5% this morning, but 8 economists had expected a hold and 9 marginally tilted expectations toward a cut so it wasn’t a huge surprise overall.

UNITED STATES

Today’s US macro reports didn’t move the needle following yesterday’s Fed’s communications.

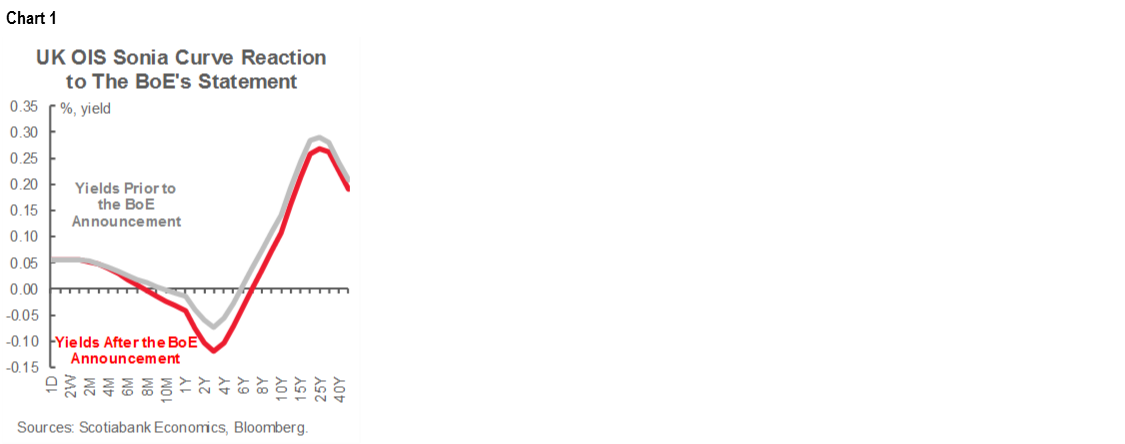

Initial jobless claims fell by less than guessed to 860k (850k consensus, 800k Scotia) and the prior week was revised up a bit to 893k from 884k. Nevertheless, the downward trend continues, just at a somewhat uninspiring pace (chart 2). Continuing claims indicate longevity of unemployment and so their decline to 12.63 million from and upwardly revised 13.54 million (from 13.39) was a bit more encouraging. Continuing claims are at their lowest since the first week of April.

US housing starts fell by 5.1% m/m and the prior month was revised lower to a 17.9% m/m rise instead of 22.6%. Permits also lost some steam as they slipped by 0.9% m/m and the prior month was revised a little softer to 17.9% m/m, or down by about 1%. The ‘V’ in home construction is coming back to earth (chart 3).

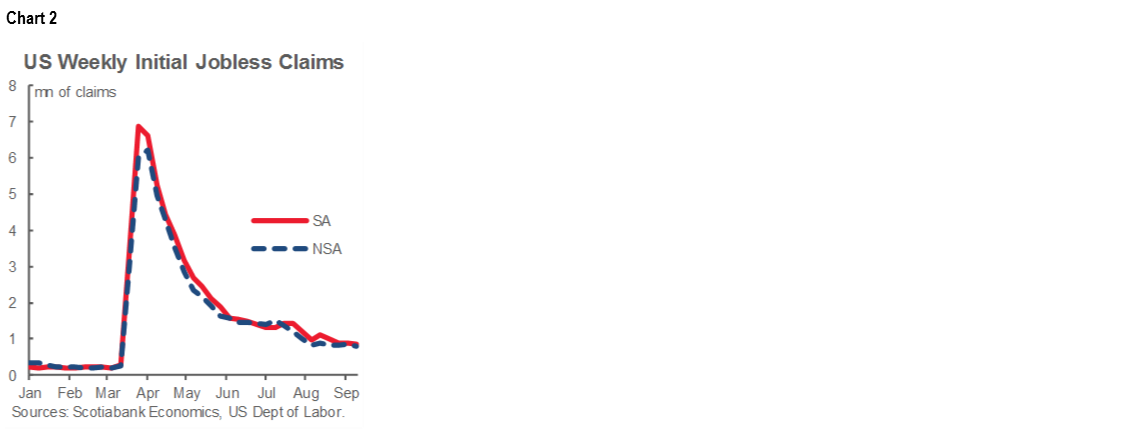

The US Philly Fed gauge of regional business conditions slipped by a statistically negligible amount, given its volatility. At 15.0 (17.2 prior), the gauge still signals a solid pace of expansion and it comes after the Empire regional gauge surprised strongly to the upside. Philly’s details were encouraging as new orders accelerated (25.5 from 19) and so did hiring (15.7 from 9.0) while shipments flew out the door (36.6 from 9.4). Like housing, Philly is also stabilizing (chart 4). Next Tuesday’s Richmond gauge will further inform expectations on the path to the next ISM-manufacturing print on October 1st.

CANADA

It’s an understatement to say that ADP’s jobs report has some issues to work out if it really wants to rival StatsCan’s household and (lagging) payroll surveys. Witness chart 5. For the fourth straight month, ADP revised its jobs numbers by seven figures. The difference between the sum of their initial estimates for monthly job changes from April to July and the revised estimates is a net cumulative revision of about 10 million jobs. StatsCan’s Labour Force Survey says there are about 18 million employed Canadians in total. I realize that’s mixing samples, but hey, that’s quibbling when revisions amount to somewhere around half or more of the total number of employed Canadians in just four months!

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.